Are you buying oil explorers, integrated or service companies?

Probably all of the above. Whatever has to be done…

Has been a long time that I did go that high on a sector, last time it was housing I think. I don’t do sector diversification in the momentum strategy.

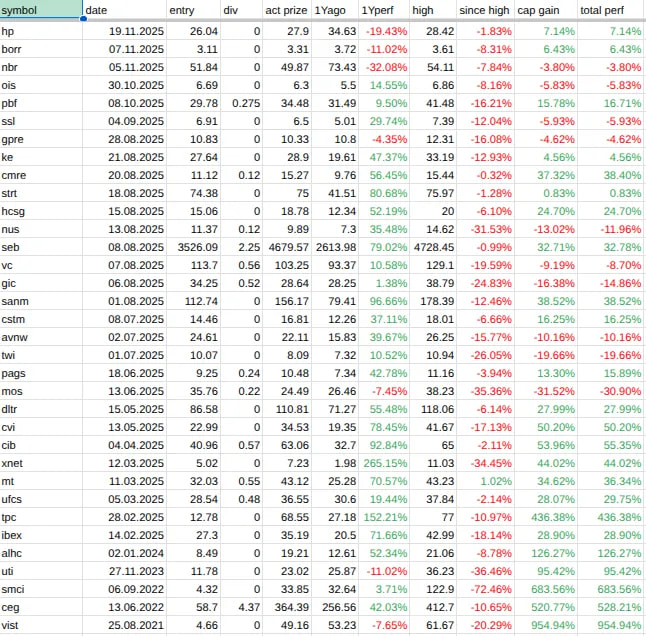

At the moment I hold CVI (+57%), OIS (-8%), PBF (+19%), NBR(new) and VIST(+942%) in the momentum strategy. Two refiners, two explorers and one service company. From experience I think there will be more. No risk, no fun.

1 Like

And on it goes with my momentum strategy. Are Oil stocks the next railways?

Had to sell Seneca foods way too early for my taste. A little gain of almost 20% in 8 months helps a little for the departing pain.

And all that just to buy yet another oil stock: Borr Drilling. I know Captain, you like those, but are those not really just doomed? OK, I do what you tell me like always.

(even in Brazil)

This is the first time in my life I experience a live testimony of someone having sold their soul for wealth.

4 Likes

To myself, as I made the rules when my brain was a little younger than now. I am the sole and only owner of my soul and I am sorry for making that much money without the f..n devil.

But then I think I lost my iron shirt…

[HD Video Clip]")

1 Like

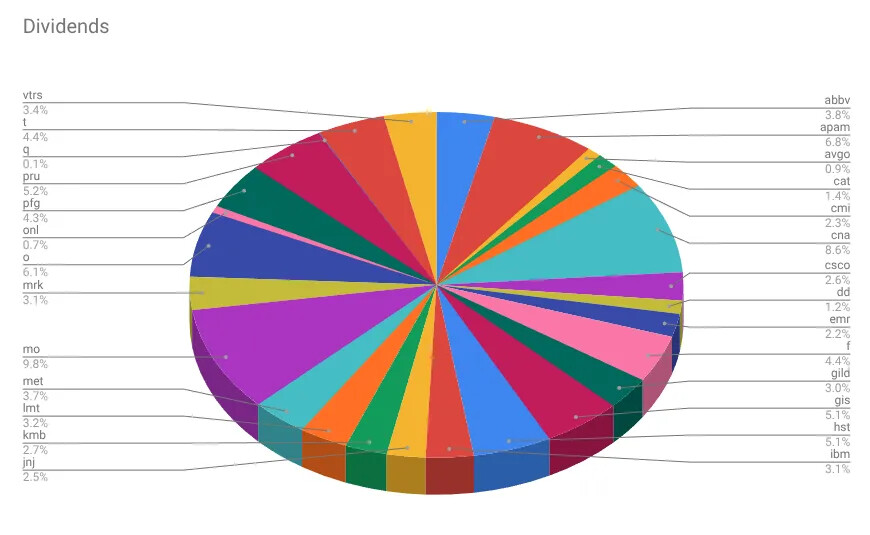

And yet another market dividend in my dividend strategy from Cummins.

With the cash and a bit more I bought more of APAM, CNA, JNJ, LMT, MRK, O, T and VTRS.

The carry premium rises to a new record this year: 11.95%. That is cash flow!

Thanks Cummins.

Dividend strategy: KVUE did not fulfill my cash flow requirements, so I had to sell it even before the merger. With part of the money I bought more Dupont.

1 Like

I’m curious how Du Pont will fare in your mechanical strategy. Looking at FASTgraphs Du Pont’s current valuation was almost always the top valuation for the company (except for a short stretch in mid 2009 to mid 2010).

So my FASTgraphs lens would tell me not to buy right now. But your mechanical strategy tells you to buy. Hence my curiosity how this will turn out. ![]()

Mostly unrelated: I once spent a year in a high school in the US (in the late 80s) and also took French as a class. The French teacher one day came into class explaining that one of her friends had incorporated a company named Du Pont, but was sued by the real Du Pont company for using its name. So the French teacher’s friend just renamed his company to De La Pont …

1 Like

How will the company where Bob Marley worked and that inspired

ever fail?

My probably not so strict cash flow rules were adhered in the last quarter and last year. The position was smaller than 4%. So yes, it was a buy!

2 Likes

ChatGPT: “that’s an urban legend”

Gemini: “Yes, the famous reggae musician Bob Marley did briefly work at DuPont in Delaware.”

Grok: “In 1965, at age 20, after marrying Rita Anderson and moving to the United States to live with his mother Cedella Booker in Delaware, Bob Marley took a series of factory jobs to support himself. One of those jobs was as a forklift operator and general laborer at a DuPont chemical plant in Wilmington, Delaware.”

Now waiting for the OpenAI IPO so I can short the stock.

I hope your other investment thesis based on cash flows will hold up just as well … ![]()

3 Likes

And on I go to be an oil sheik with yet another one. When will it stop? Bought myself some Helmerich & Payne today for my momentum strategy.

Momentum strategy: sold some of the world’s biggest mechanics school, UTI, after 24 months. Welcome to the 3rd year with me, UnTrained Idiots. Momentum fades away, probably they won’t make it to the 4th year. Actually at plus 95%.

And here comes the November report:

Momentum strategy runs very nice.

Portfolio:

Margin multiplicator: 134.6%

Performance: YTD 21.62%, XIRR since 2020 27.25%

Wheel of fortune:

And the dividend strategy:

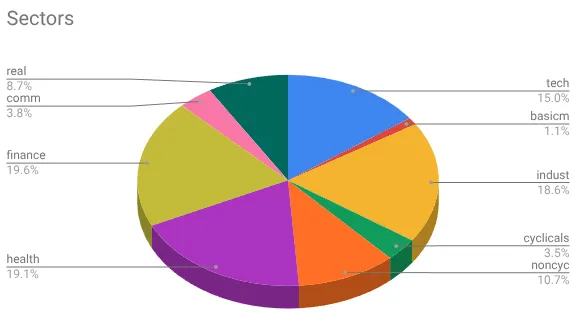

Portfolio: finviz

Dividends: T,GIS,ABBV,O,CAT,APAM

Sold: KVUE

Partially sold (market dividend): CMI

Bought additional positions: APAM,CNA,JNJ,LMT,MRK,O,T,VTRS,DD

Carry premium: 11.56% (yeah, that is cash flow baby…)

Margin multiplier: 100.29% (almost no debt).

Performance: YTD 18.77%, XIRR since 2014 11.05%, since 2020 13.99%

And the wheels of fortune:

3 Likes

Congrats.

Love that big fat MO dividend pizza slice! Almost wished I was not as strict with my (dividend) position sizing when I see such a juicy slice … and it’s still not really expensive!

OTOH my strict (dividend) position sizing has saved me from losing a significant part of my cash flow produced by some other companies when they decided to cut their dividend.

Still … seems like it’s currently unfathomable that Altria will ever cut theirs. Their earnings growth is even more steady than Johnson & Johnson.

If I was really rich I’d probably back up my truck to load up on some more Altria. If the bet goes south, so what (since I’m really rich). As I have to manage risk, my pile of Altria is already (almost) full. It’s mostly always full, but as the overall pie starts growing little slices of adding more MO occasionally open up.

![]()

1 Like

the thing that makes me be careful with tobacco is that the current generation seems to be getting healthier. drinking less. etc. so i do wonder if revenues/profits will rapidly decline at some point.

1 Like

I see children with those plastic sucks and they are probably even legal in Switzerland. Gateway drug.

No, thanks for smoking…

This year my cash flow from market dividends is almost 3 times the regular dividends. And market dividends are free of tax…

MO is on buy, but is too big to buy more at the moment. I only add to positions that are less than 4% of my portfolio.

Trigger warning:

Are you quoting from a 1980 aerobic commercial shot on a California beach starring Olivia Newton John? Once a secret idol of mine even as I probably didn’t even know her name or so, but maybe heard a song and saw a picture in (physical, i.e. printed) Bravo magazine at one of my friends who were allowed to read/own the publication.

When I was a teenager in mid 1980’s we would be forced in (public) school to see in 8th or 9th grade anti smoking campaign videos featuring one of the Marlboro men giving interviews with a throat microphone (as obviously he got sick with larygeal cancer).

Hat tip to the school authorities at the time as it definitely worked with me never wanting to smoke (because of those videos). Not that I expect to live any longer because I don’t smoke, but I’m still kind of glad.

Yeah, and about that current generation … I wonder if you’ll change your mind once your kids enter teenage territory. I was kind of surprised how many of my son’s friends smoke, vape, etc.

Perhaps the revenue from LVMH has been declining, but from what I personally observe these kids absolutely want to consume their shit. Maybe it’s not Hennessy, but they’ll have their vape.

See MO’s earnings curve above.

Q.E.D. ![]()

![]() I liked the 70’s or 80’s feeling of the trailer I clicked into.

I liked the 70’s or 80’s feeling of the trailer I clicked into.

But to be clear: I would actually prefer people to not consume products that advance their likelihood of death (not just for selfish reasons like them being able to contribute to my pension and AHV for longer. Or, wait, should I be interested in them perishing earlier so they won’t be beneficiaries of AHV …? Anyway …)

I more strongly believe these people should have the choice to do whatever they like including deciding what they consume.

I have my opinion on how smart that is, but who am I to pass any judgement.

Yep, same boat.

1 Like

I wonder how much of the younger generation smoking less is also different per countries. While I have no clue about generational development, my impression is that people in Switzerland smoke a lot, compared to e.g. Anglo-Saxon countries.

1 Like

no worry… my friends and I are compensating them by large…

1 Like

I may be wrong, but MO went down a lot when they said to go out of the cigarettes market. Don’t know by when, but seems that all the youngsters now suck on MO’s overpriced plastic sucks. Children first without and later with all the addicting drugs…