Whoo…I didnt get this being a newbie ![]()

Why mix with cash ?

Why is the bond fund you suggested earlier not suggested now ?

Could you please rephrase ?

Whoo…I didnt get this being a newbie ![]()

Why mix with cash ?

Why is the bond fund you suggested earlier not suggested now ?

Could you please rephrase ?

Even though I started this thread by referring to crash prophets like Robert Kiyosaki, I neither follow main stream nor act according to that. My mind is set to do the opposite of what is shouted at the masses.

On a rough level, bonds react to interest rate changes as a function of their duration: for each 1% of interest rate hike, they should loose 1% per year of duration of value (so 10% for 10y bonds, for example). They’ll recover that loss due to increased interest over their duration (so 10 years for a 10y bond). The reverse happens when rates fall.

This is the best thread I’ve seen on the topic: Short- and longer-term effects of rising interest rates on a bond fund - Bogleheads.org

In essence, a 50/50 mix of 10y and 5y duration bonds should behave roughly like a 7.5y duration bond (for each 1% of interest rate rise, the 10y bond would loose 10%, the 5y 5% for a mean of 7.5%, the same as the 7.5% bond, then they’ll regain the lost value at different rates which approximate a breakeven at 7.5 years for the 2 solutions).

So, in theory, we can finely tune the duration of our bond funds by mixing and matching durations. Cash is essentially a 0 duration bond so by mixing a 2y duration bond with cash at a 50/50 ratio, one would have a mix of assets behaving roughly as a 1y duration bond, so by adding the right amount of cash, you can theoretically lower the duration of your global fixed income assets to the term you are targetting.

This is what would happen in lab conditions, in reality, there are other aspects that make things happen not exactly as the theory would have it but since I lack a better while still simple model, I consider it good enough for me.

Let me know if you want me to develop more. The Bogleheads forums have very knowledgeable people and are usually a good source of information. Their Wiki provides good information on bonds:

https://www.bogleheads.org/wiki/Bond_basics

https://www.bogleheads.org/wiki/Bonds:_advanced_topics

https://www.bogleheads.org/wiki/Individual_bonds_vs_a_bond_fund

.

I don’t think there are a lot of short term bond or money market funds with either assets denominated in CHF or hedged in CHF available to retail investors, I’ll have to dig a bit and come back to you on that one.

Edit: @Fallguy our own Wiki is a great resource on the existing fixed income options for Swiss investors with links to the active topics regarding the best rates/products available currently. Thanks to all the contributors and to @nabalzbhf for having started and compiled it: Short guide to CHF fixed income options

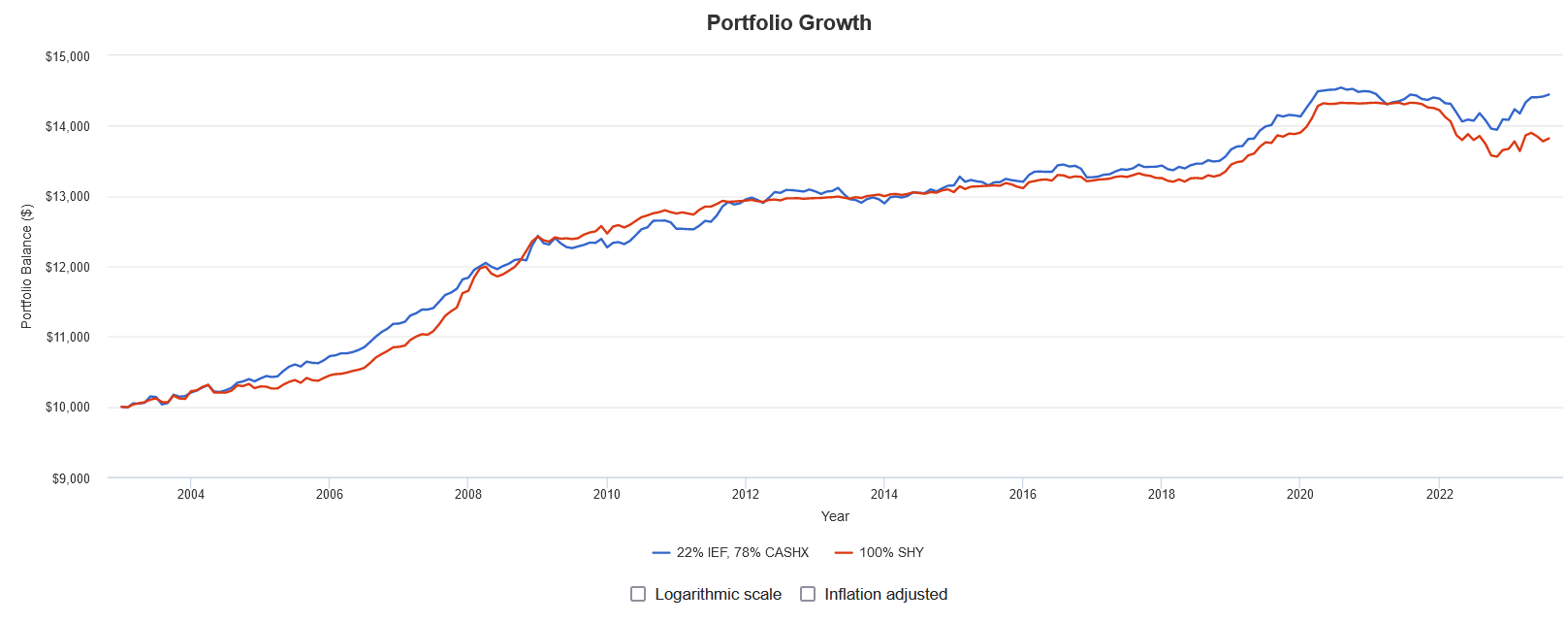

As an illustration:

IEF is an intermediate term US treasuries fund with a current effective duration of 7.42 years.

SHY is a short term US treasuries fund with a current effective duration of 1.84 years.

CASHX represents cash in Portfolio Visualizer, it is actually 3 months treasury bills if I understand correctly, so effective duration of 0.25y.

This is a comparison of the returns, in USD, one would have obtained:

by holding 22% IEF and 78% CASHX (effective theoretical duration of 1.83y) in blue.

by holding 100% SHY (effective theoretical duration of 1.84y) in red.

To note that the effective duration of the funds may have varied during their lifetime and the rebalancing is done monthly so small divergences can occur. The temporary outperformance of the mix IEF/CASHX seems to occur during periods of raising rates (2004-2008; 2016-2018; 2022-2023).

If you calculated that it will deliver your target retirement income then all good

If you need to grow wealth more aggressively then your allocation to stocks is quite low. I estimate it at 33% of NW (I find it a bit difficult to follow your notes but understood your general idea is to deploy 75% of your cash as stocks and leave the 58% of your NW currently in 2P, metals BTC alone )

A 6% weight in volatile BTC looks a bit odd in an otherwise conservative portfolio

Still going.

What have you finally done?

Sounds like the top was in when Jensen Huang signed a woman’s chest back in June ![]()

/s

I wonder how they depict that on Bloomberg’s terminals.

w …?

More than one person called the top based on that! ![]()

Maybe Jensen ought to get out there signing some butts to keep it going a bit longer…