Wow, that’s clever - all so you can do a recurring transfer from your bank account without further hassle?

Correct, I do automatic monthly bank transfers to Avadis.There is zero trading cost (neither explicit nor implicit). That saves me from monthly investments. I then generally once a year call off the amount from Avadis, and invest it into individual funds.

The only important things:

i) Avadis does manual withdrawals- so I consciously don’t give them more than 1, max 2 withdrawals per year that they don’t face a cost challenge on me as a client. Pluse I keep some assets (20k or so) just so that they have a stable revenue stream from the TER I pay

ii) I respect dividend pay-out dates aka ensure that I receive dividends that I tax. If I kept calling funds right before dividend dates, that may trigger an issue as it could be considered both unfair to other avadis investors and might even constitute tax evasion

1 Like

Here is how I figure out my own strategy.

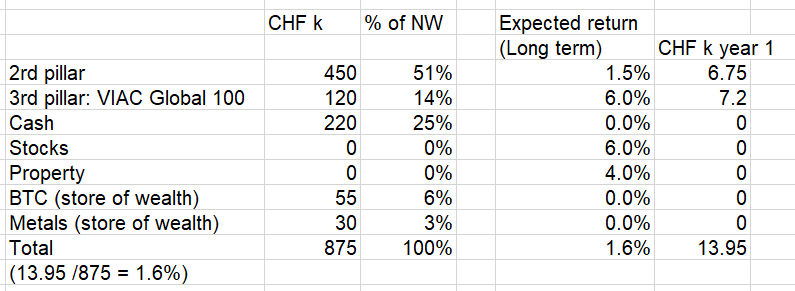

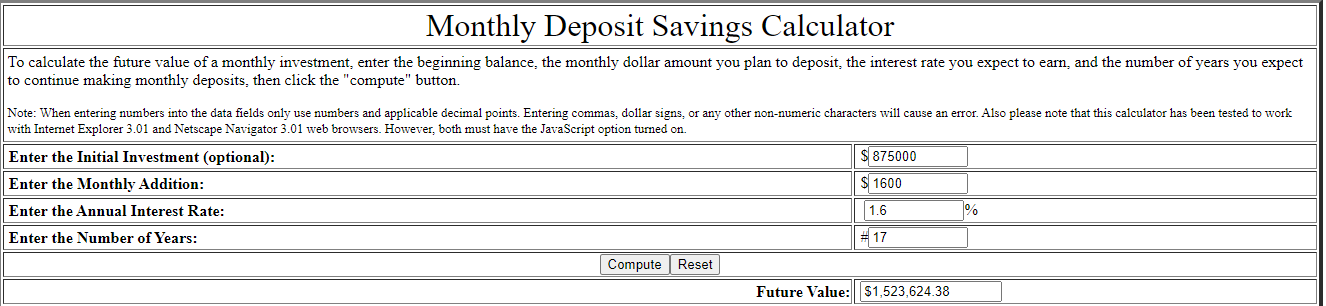

Based on your current asset allocation your expected return on wealth is probably ~1.6% due to having a lot of 2P and cash. In 17 years aged 65 you could reasonably expect to have ~1.5M wealth:

Applying 4% SWR rule you could count on ~60k income age 65 (in addition to Pillar 1 AVS).

If you move current 85k BTC and metals and 200k of cash to stocks you could have ~80k income instead of 60k. The trade off is you need to be able to tolerate more volatilty and risk before then.

If this is not enough you could try to save more. For example saving 2k per month instead of 1.5k increases your income to 86k

Once I do these back of the envelope calculations I fine tune asset allocation , risk tolerance etc.

Your second pillar has an expected return of 2.5% (long-term) and about 3.5% over the next 5 years. Compared to 4.5% with shares, this is fairly decent. This of course unless you don’t have a pension fund as such. If your employer selected an Insurance Solution - then you are screwed and you indeed struggle to make the 1%. But that is a very rare case…

Too low - with 450k of Second Pillar at age 48; he will probably have a final P2 balance of about 1M. Therefore, I would forecast about 50k from the second Pillar only. Then you take the remaining 3rd Pillar and Portfolio and on these, you apply the 4% rule…

Indeed employer and employee contributions to 2 Pillar should be counted in addition to the 1,600 /m savings rate

I’m not very learned regarding pillar 2. The 3 funds I’ve been a part of all had roughly 1%, max 1.25% yield during the last 9 years, though it was a period of negative interest rate and I am expecting a better yield on a longer period of time.

What is the difference between the pension funds as such and the insurance solutions that you mention and how do you know if your employer’s pillar 2 plan is one of the former or of the later?

3 Likes

I would actually want to keep all BTC and metals for diversification. I believe in BTC, after following the developments for some years now. There is never total certainty, but neither is the stock market certain.

1 Like

Save more and invest that into ETFs/stocks is what I would do.

1 Like

Rich Dad Poor Dad rant

In my opinion Robert Kiyosaki is a grifter. I think he’s just peddling what gets him clicks on his videos/podcasts or what gets him booked to give speeches. I saw some of his podcasts a few years ago and I don’t think he’s particularly good at timing the market. At least not with the advice he gives out to his audience.

Oh, I read some of the first replies now after writing the above and I think enough has been said about the guy already.

You’re effectively saying that you think you’re smarter than the average market participant. It’s hard to evaluate from here if that’s true or not.

You can also go play roulette and put 25k on red, but you shouldn’t consider that an investment.

This protects you from inflation in the longer run. But it doesn’t do anything on it’s own, so it’s kind of like “insurance” and you’re paying a premium in the form of opportunity costs. If you think there will be a crash in the short-term, cash is king as even gold tends to drop with the market, because some players need to sell gold to cover their losses (or margin requirements) from other contents of their portfolio. Given the current inflationary environment I think it’s a good idea though.

Given your opening post it may not be wise for you to go all-in ETFs as you’re already doubting the merit of the strategy before you started. I don’t suggest the following because I’m not a financial advisor:

- Lump-sum 30k into VT or VWRL

- Set up a recurring investment of 2k/month into VT, or a quarterly investment of 6k/month into VWRL (assuming higher fees) that you try to keep going even beyond the 50 month run rate from the initial 150kCHF

- Lump-sum 20k into gold

-

- Keep the rest in CHF and ready to be put into use to lump-sum into VT or VWRL if there was a significant correction

-

- or

-

- Keep a portion of the rest in some “paper-gold” like IAU if you’re worried about inflation

The trade off is you sacrifice the growth that can be expected from stocks over the long term. You can estimate the opportunity cost: 85k in stocks is likely to grow to approx ~228k in 17 years’ time, in turn supporting ~9k/ yr expenses in retirement (4% rule).

Metals may give some diversification and stability in the short term but you sacrifice the growth from shares. The price is not underpinned by growing cash flows

BTC has correlated to stocks so far with a multiplier effect so I would not agree it gives diversification. If you believe in BTC and your financial planning gives you enough leeway to have a punt on it, then go for it

1 Like

Pension funds generally have liabilities with a longer duration than their assets. Meaning that they heavily lose if interest rates drop, and they heavily win if interest rates go up. This will give pension funds a big boost for the next few years. The contrary was the case the past ~ 10 years.

According to the statistics, pension fund assets have since 2006 delivered about 3% of annual return (nominal). This in an environment with very low inflation. Their real return was probably in the range of 2%. In the meantime, share quota has gone up so we can expect even a higher real return.

In summary - more than 2% real return (based ok the historic performance dating from before the great financial crisis)… plus the effect from increasing interest rates that allow pension funds to credit more interest than asset return generated; that gives a very rosy picture.

Insurance solutions are different as they don‘t work with coverage capital but it is a hard obligation for the insurance company to always be ready to pay 100% of the funds. Meaning that they have an Investment horizon that is very short and zero risk capacity. As a consequence, they invest mainly in bonds and your expected return is terrible. The 10 year benchmark rate is probably the max you can realistically expect. But there are only about 500k employees or so with such a solution and this mainly minor enterprises and low income jobs.

1 Like

– Final strategy ( I hope ): –

To all, thanks very much for all the inputs and discussions. I have gone through all of your inputs until date, broken my head now ![]() to arrive at the following strategy which should balance out the pros and cons of all relevant aspects:

to arrive at the following strategy which should balance out the pros and cons of all relevant aspects:

Summary: I will combine a quarterly sell-bonds-to-buy-shares DIY/broker evenly distributed DCA strategy across 36 months (not too long) adding monthly savings from income, speculating that market corrections would happen over this time period. This would allow me to do one or more lump sum investments during the 3yr period in case market corrections of say at least 10-15% happen. Once all funds are in the markets latest by Sept 2026, I have ~13 years until retirement, so the portfolio can work over this time, maybe longer, if retirement age gets prolonged ![]()

Target Fixed Ratio Portfolio:

- 75% VWRL (probably won’t go VT due to unavoidable US estate tax admin overhead for my heirs with ambiguity how the Swiss-US tax situation will be in the future, also relating to the current exemption amount of USD 60k)

- 25% Cash or bonds

- Check for rebalancing need every 6 to 12 months

Cash Flow Sources:

- Investment cash from accumulated savings: 173k

- Investment cash from monthly savings: 192k (1k/month x 16 yrs x 12 months)

Sum: 365k

Target allotment:

- VWRL:

(173k x 75% = ~130k) + (192k x 75% = 144k) = ~274k - Bonds:

(173 x 25% = ~43k) + (192k x 25% = 48k) = ~91k

Sum: 365k

Cash flow next 36 months:

Monthly:

-

VWRL:

– From accumulated investment cash: 130k / 36 months = 3611 / month

– From monthly savings: 750 / month

Sum: 4361 / month -

Bonds:

– From accumulated investment cash: 43k / 36 months = 1195 / month

– From monthly savings: 250 / month

Sum: 1445 / month

Quarterly:

- VWRL: 4361 x 3 = 13083

- Bonds: 1445 x 3 = 4335

Sum: 17418 / quarter

Yearly:

- VWRL: 13083 x 4 = 52332

- Bonds: 4335 x 4 = 17340

Sum: 69672 / year

Cash flow post next 36 months until retirement (13 years): 156k

Quarterly:

- VWRL:

– From monthly savings: 2250 / quarter - Bonds:

– From monthly savings: 750 / quarter

Sum: 3000 / quarter

Further points: -

a) I understand that the majority of people here suggest to reduce my BTC holdings (and partially metal holdings) to invest into the stock market. I will re-assess my crypto strategy after calculating my income projections post retirement from 1st pillar, 2nd pillar and 3rd pillar.

b) I will maintain a 50k emergency cash cushion apart from a tax cushion

Questions:

- What do you think about the overall asset allocation, DCA strategy and lump sum strategy when the market corrects?

- Sell high-quality CHF bonds bonds to buy shares strategy vs. cash to bonds and shares: Is this a good move to transact bonds to shares to yield interest for the part of bonds waiting to be sold for shares ? If yes, which products suggested ? Or rather invest cash directly into bonds and shares ?

- Any inputs on how to go about rebalancing ? Manually ? Free tools ?

- Is it advisable to add CHSPI or SMIM as CH-shares ? It makes the portfolio complex though and adds trx costs and overhead.

- Has anybody having US assets already gone through the US estate tax hassle ? If yes, kindly report back, how to simplify this process to the max.

I would appreciate short answers ![]() now that I have summarized my strategy into a hand full of words

now that I have summarized my strategy into a hand full of words ![]()

2 Likes

I think the market has crashed already. When you factor in inflation and current prices, it’s down by 20%. Will there be another crash? Nobody really knows.

DCA might be better for your peace of mind, but personally, given the current conditions, I’d go with a lump sum. Just my two cents.

1 Like

I do not mean this in a harsh way, but maybe just as a valuable thought experiment to test emotions (for all of us). Why do you mention market correction? If you really expect it, wouldn’t you go short then? If you imagine for a second that you went short, would you be comfortable with it, or would you be scared that you are missing out on potential growth?

My overall investment strategy is buy-and-hold / going long only. Hence, buy when the market drops.

Not intending to do short-trades with retirement capital.

Good enough. It will get you invested and that’s what really matters. I’d note that, from a risk perspective, there is no fundamental difference between doing a lump sum and having all your assets invested at your target allocation at the end of a DCA: in both cases, all your assets are invested and subject to market changes. DCA can allow someone to target an allocation riskier than their effective risk tolerance would actually allow. I’d keep an open mind about that and reassess my risk tolerance after some time.

If the bonds you’ll select for that have a duration that matches the time at which you plan to sell them and buy stocks, it is fine in my opinion. If your plan was to buy an intermediate term bond fund, then it’s a bet on intermediate term bonds overperforming cash on the short term.

One way to handle the duration risk would be to use a short duration Swiss bonds fund (for example iShares Swiss Domestic Governent Bond 0-3 ETF: https://www.blackrock.com/ch/individual/en/products/261156/ishares-swiss-domestic-government-bond-13-ch-fund, with an effective duration of 1.88 years) and to mix it with cash to bring the duration down to the actual term of your liabilities when necessary. Note that the above iShares’ fund has only 3 assets, so using a bond fund for that may not be fully justified. It may be more hassle than it’s worth.

I go manually, others may have better tips.

If you are asking yourself the question, it is probably not worth it to you. I would consider it if I were trying to dilute my exposure to the US or the part some heavy stocks like AAPL have in my portfolio, or if I wanted to hold a fund domicilied in Switzerland and/or managed by a Swiss bank for regulatory reasons. In those cases, I would avoid funds tracking the SMI or the SPI because of the very top heavy concentration of Swiss stocks. SPI Extra or SMIM would be fine in my opinion.

As a side note:

It is very rare for the markets to give an “all green” signal that no expected drawdown is on the horizon and, even when it happens, other participants have access to the same or more information than you and it’s likely for stocks to have lower returns during that period (because they present less expected risk). In order to profit, you have to be invested before other investors consider the situation is safe enough, that is, when the doom prophets are on the streets claiming that staying invested is foolish.

Stocks do climb a wall of worries, and often fall due to unexpected events (9/11 in 2001, Lehmann Brothers’ bankruptcy in 2008, etc.). Our psychology plays a lot of tricks on us that are not conclusive to success in investing in the stock market (CNBC article on loss aversion, for example: https://www.cnbc.com/2016/04/26/investors-fail-because-of-this-impulse.html). The best way to beat other market participants is to choose an allocation we can stick with come hell or high waters, keep investing regularly and stay the course.

2 Likes

Thanks. To my understanding, this can be incorporated into the 1-2 annual rebalancing reviews, adjusting the fixed ratios.

1 Like

IMO, with interest rates on the hike and unclarity on how this is going to evolve, short duration bonds are the only option right now to lower the volatility of the bond price.

Yes, this product fullfills the parameters: Short-Term, CHF, Government bond.

Any other specific product suggestion ? JustEFT.com doesnt have other products with those criteria…