I’m 30 years old, living in Switzerland, and currently have CHF 200,000 available for long-term investment. I work night shifts and can save about CHF 1,000 per month.

My goal is to build wealth steadily and with minimal stress, generating regular cash flow in CHF and maintaining high security. My investment horizon is 20 to 30 years. I plan to rebalance the portfolio manually every six months.

Just a remark to the bi-annually rebalancing: this may be a bad idea, depending on the correlation of your investments. According to “Shannon’s demon” theory, rebalancing gives you additional return for non correlated investments. But if the correlation is high it may be a waste of resources or even bring worse performance. If the correlation is high rebalancing is like a coin flip. If the correlation is low rebalancing may bring you positive returns even if all the investments have negative returns, that is the demon.

I feel that portfolio is very heavy on Switzerland and very low on US, is this deliberate?

A very high dividend strategy will reduce your returns because of taxes, why do you need so much dividends during accumulation phase?

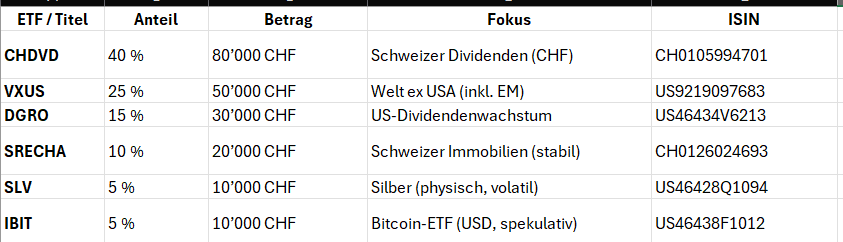

In summary , your portfolio comes down to

CH + ex-US + US + RE + crypto + precious metals

Crypto & Precious metals are speculative investments with no cash flow. So it’s up to you how much you allocate there. I am not much into non-cash flow assets

Talking about following. Your strategy looks fine but the choice of instruments and proportions are something to reconsider .

CH + ex- US + US + RE

That VXUS will do worse than the US when the US does well, and even worse than the US when the US does badly, unless there’s a rogue orange-utan at the helm. If I was splitting the world I’d get developed ex-US, and see that it doesn’t miss countries like India, Korea, Taiwan.

Thanks already for your quick replies – you’re a really strong community!

My Strategy:

I’m risk-tolerant (8/10) and want to use Bitcoin and silver as a counterweight to my heavy CHF exposure.

My goal: 50% CHF exposure, the rest globally diversified (growth-oriented).

On the broker topic:

A friend pointed out the following – is this accurate?

If I hold CHDVD or SRECHA (CH-ISIN, Swiss domicile) via IBKR:

No E-tax statement (E-Steuerausweis)

35% withholding tax not automatically reclaimable

Manual declaration of each dividend in my Swiss tax return required

Alternative: Hold CH ETFs with Yuh, Swissquote, or Saxo CH

→ E-tax statement available

→ Automated reclaim process for Swiss withholding tax

Dividends – Worth it in Switzerland?

I’m currently more focused on growth. Dividend strategies are tax-inefficient in Switzerland, because:

Dividends are fully taxed

Capital gains are tax-free (if held as private assets)

So in the long run, it’s likely more efficient to use accumulating ETFs (domiciled in Ireland or Luxembourg).

My current thinking:

If I stick with IBKR, I should probably focus on tax-efficient, accumulating ETFs (e.g. iShares, Vanguard, Ireland/Lux).

A 50% CHF allocation still feels right – to manage FX risk and keep things stable.

What do you think?

Hold CH ETFs like CHDVD or SRECHA via Swiss brokers instead?

Keep everything at IBKR, but optimize via Ireland-domiciled ETFs?

Or consciously accept the admin hassle of holding CH ETFs at IBKR?

Accumulating are taxed the same in CH (the internal dividends are taxed)

No sure what this means, it’s mostly equity not CHF exposure (and what’s the thesis for silver? I get gold because it’s used as an hedge/central banks)

Thanks for your explanation on accumulating ETFs – I didn’t know that. A friend of mine told me otherwise. So, from a tax perspective, it’s probably best to avoid dividends where possible, right?

Silver is more of a speculation for me. I think it might catch up to gold and possibly offer some inflation protection. Do you think 5% of the portfolio is too much?

By “CHF exposure” I just meant that I prefer holding something like UBS ETF (CH) SLI (CHF) A-dis, which is denominated in CHF, instead of SLV, which is in USD – just to keep some CHF exposure.

I wouldn’t say avoid, but at least not actively seek it.

For that kind of unusual investment you probably need a better thesis than “I think”

Currency used by a fund doesn’t matter, silver bought with USD or CHF is still silver, what matters is what you buy not with which currency you buy it.

When I said “CHF exposure”, I actually meant that I’m trying to allocate around 50% of my portfolio to CHF-denominated assets – to hedge against a potential USD depreciation and preserve the Swiss franc as my base currency.

But you’re absolutely right: the fund currency doesn’t matter. Whether I buy silver in USD or CHF – it’s still silver. What really matters is what I’m buying, not in which currency it’s traded. Honestly, I didn’t even think of that…

Hello! The advice that it is what you buy rather than the listed currency is very good advice.

The CHDVD fund is 20 Swiss-listed companies. They are almost all large multinationals, with their income in foreign currency. The Swiss franc is therefore going to be largely irrelevant to their value. Currency exposure is so complicated once you go down that rabbit hole!

If I were you I would first decide what my objective and time frame is. Income? Long term growth?

If, say, I were saving long term and wanted growth, I would keep it simple, put it in a cheap, passive ETF (like VWRL) and maybe a bond fund. If you want some Swiss exposure (since I suppose it could be argued that the success of large Swiss-based companies could be correlated with the Swiss economy and therefore currency), there’s always CHSPI with 0.1% charges. Your strategy of using mainly low cost funds looks good to me.

Now that it’s clear that what you buy is main factor and not which currency you buy it in, you have following things to decide

If you want exposure to Swiss companies (SLICHA or SPICHA) could be good options.

If you want US exposure -: then UBU9, SPY5, VOO would work. The last one is US ETF and other two are domiciled in Ireland.

If you specifically want higher dividend strategy (after you have understood pros & cons), then you can pick high div versions. But remember they might reduce your returns due to taxes during accumulation phase

If you are worried about foreign currency exposure, there are also hedged version of S&P 500 ETFs available. But remember hedged ETFs work both ways. If USD depreciates more than expected then you will benefit, if it doesn’t, then you will have a lower return. So just make sure you understand what hedging actually does. This video would be helpful

VXUS is already well known. So nothing to add

SRECHA is good ETF for Swiss real estate. So you got it right.

If you feel overwhelmed , watch this about Home bias.

SLICHA should be preferable to CHDVD but either is very concentrated to a handful of companies. CHDVD has outperformed in a way one can’t easily ignore though. Wasn’t aware of SRECHA…what does one think when buying real estate funds? Is it that RE prices will continue to rise? 0.97% TER too, very high.

Well because SLICHA limits how much % each stock can be and doesn’t select for dividends, so it captures large cap CH stocks and should be a tad more tax efficient (though it does have high dividends by design, as most European large caps do). In my opinion anyway! But as I said, CHDVD has outperformed SLICHA and SPI so there’s that. I don’t own either but knowing myself that’s probably what would happen if I was about to get either:

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.