Ciao everyone!

I have a question related to my move to the UK. I’ve been reading in the forum but couldn’t find an answer yet.

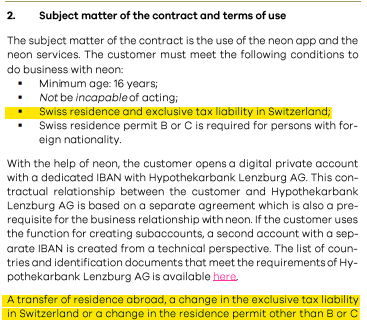

I am moving next week to the UK, which means that I need to close my Bank account at the BAS + receive the payment for my fellowship for 12 months on a Swiss account (using my name) in december.

My idea was:

1- move the money from the BAS to Revolut, and leave it there in CHF (approx. 50k). When I have time to better inform myself, invest part of it with IB or Selma.

2- give my Revolut account number to get the fellowship amount in CHF (around 60k), then sell the whole yearly salary to pounds without needing to open a bank account in the UK.

Questions:

is it a good strategy?

is it safe to have all my money on Revolut (50+60k, half in francs half in pounds as explained above)?

I wouldn’t recommend leaving all your money in Revolut long-term, both because of its questionable depositor protection and because you will likely find a higher interest rate or better investment opportunity elsewhere.

But as an interim solution for changing the money, it’s an affordable option. However, it’s only possible/beneficial if BAS is willing to transfer to Revolut’s Swiss account instead of a Swiss bank account in your name.

couldn’t I move all my money to Revolut first, and then close the account, for instance?

I understand, then I should open a bank account in the UK, but I’ll be there only for two years (then who knows), so I am unsure where to put my money in general. I am still even hesitating where to put my 2nd pillar. In my work I will need to move quite a lot. My partner for now stays in CH. an alternative was to transfer my money to his account. (but it seems a bit shady in my opinion).

I quiclky checked on google and it seems like it works!

as an alternative I’ve heard that I could open an account Swisspost because I could keep it open from abroad, with e.g. 25CHF cost per month, something that the BAS wouldn’t allow me to do. I could then transfer my fellowship monthly to Revolut or something similar in the UK.

would that be more convenient?

I do have an account with a reference number, in francs, on Revolut (at crédit suisse though).

Yes I had found the same issue…

After several discussions tonight we were thinking of opening a joint account at Postfinance before I leave, we will try to call tomorrow - since my partner stays here. I’d then transfer on Revolut a share to cover my living costs in the UK, converting them in pounds (unless there is a better way to exchange francs in pounds).

For larger amounts, I can recommend Wise. It is much cheaper than the rest and costs are transparent. I used it for transfers to India (which is one of those countries where it can get complicated), and in my family we used it for my brother who was studying in Canada. There is also a possibility to open an account there with a debit card. This would be cheaper than changing through postfinance.

Do I understand you correctly that your stay in UK is limited to 12 months and you will come back afterwards ? Then I would say your solution is not too bad, just open another UK account and use Wise to get the amount you need for living from Switzerland to UK (or use the Wise debit card, to be checked if this is the right way.

Just a note, postfinance is pretty expensive when you do not live in CH. I do not know how it works when one partner is in CH and the other one in UK. When I went abroad for company, I did not tell them that I was not living in Switzerland anymore, and it was fine…, but not really compliant.

If you have a joint account and one account holder is in Switzerland, then you shouldn’t have any issues. In fact, some banks will already let you keep your Swiss account if you give a resident a power of attorney (Vollmacht) over it. So if there’s someone here you trust, a joint account is a good option.

Alternatively, you could consider a Swissquote account. It’s primarily a brokerage account, but also has basic private account functions (your own Swiss IBAN, incoming and outgoing transfers). AFAIK you can keep your account after moving abroad and you do not pay extra non-resident fees. There also isn’t any basic annual account fee. If you just need a Swiss account to receive money into and make transfers to other accounts from, this could work.

My suggestion for your second pillar: If you don’t have a clear plan for the money, leave it in a Swiss vested benefits foundation for now. This will give you time to find a free or very low-cost vested benefits foundation in a canton with low withholding taxes on vested benefits. You do not have to withdraw your benefits when you leave the country, and you can transfer them between Swiss foundations, so there is no rush whatsoever.

Thank you so much for these replies. Honestly, I’m really struggling in deciding what to do and having your support is priceless.

Thank you for confirming this! My partner already has Postfinance, so we would simply open a second account there. The costs should be 60CHF per year for a joint account (5 per month), and I’d take care of it. Since I am unsure what will happen in the future (coming back or not; I’m in academia, we never really know where we end up moving to…), it gives me time to figure that out. Also, I really don’t want to change all my money into pounds or euros. Thank you for the reference to Swissquote. I didn’t know it. I’ll look into that.

I read about it this morning! That’s great. I’d then open something there, and transfer from my postdinance to Wise, and from Wise to the UK bank I’ll choose (they recommended me Monzo). I’ll inform myself more about Wise today, but I imagine that since you suggested it, it must be more convenient than Revolut.

I’ve heard that many people did so. But for me, if I open it now and leave in a week (considering also that my B permit expires in 1 month), it might be a bit suspicious.

My stay would be of 24 months; then I really don’t know what will happen. I might come back, or I might decide to move somewhere else. But for now, keeping my money in CHF is the most stable choice, I feel.

Thank you so much @Daniel - to be fully honest I am going a bit crazy in figuring out whether to invest them directly or to put them in VIAC. From what I understand, the best would be to put them for now in VIAC, and then in the next years see if I come back to CH or not. If I don’t, take them away and put them e.g. in IB (while becoming more comfortable with using it). If I come back, I simply transfer it to my new employer 2 pillar.

Am I correct to say that, I don’t come back and I withdraw them in few years from VIAC, I would be taxed in Switzerland and due to double agreements, not in the country where I’ll be living (it depends of course, but it seems that for the UK for instance this is the case). Or am I completely wrong, and it is smarter to take them now, in these last few days that I live here, and am taxed here?

Wow, I feel like once this is solved my life will feel much lighter!

You mentioned partner and kids, I guess they will come with you.

For that long period, I would open an account in the UK and look to close everything in Switzerland in the medium term (no need to do it right away). If you want to keep some CHF, you can keep it in something like IB.

So what I would do for cash/savings accounts:

-have Revolut or Wise ready with some Pounds for the move and the first days.

-choose a UK bank you want to use over there long term once you moved. Use Wise to get some money until you can live off your local salary

-Open an IB account once you are settled and life becomes less stressful

-Transfer your CHF to it

-Close your local accounts in Switzerland. Then you can choose what to do with it (invest/keep some cash/transfer to pounds)

The 2nd pillar and 3rd pillar is a different story. You will have to look up the DTA and the UK pension system and then choose what is the best solution. Maybe looking up for an advisor might be helpful (btw big universities should have some help office for internationals concerning this kind of questions).

Until you know what you want to do, put your 2nd pillar in VIAC/Finpension or similar. The 3rd pillar keep it as is and then figure out what to do with it once you moved and stuff has settled.

If you need to keep a CHF account over the whole term to receive some salary (you mention it in the first post, but I am not sure I understood it correctly. Will you still get money from Switzerland over your whole stay in the UK or ist it a one time thing ?), maybe look at a internation bank like HSBC. I am pretty sure you can have an account in CHF with Swiss IBAN to receive CHF easily.

I do not have kids, but only a partner who will stay in Switzerland. That’s why the join account could work - he’d stay here while I’m away. My fellowship lasts 24 months, we’ll then see where to move (hopefully together).

My salary will be transfered from Switzerland. They’ll transfer me 1 years altogether in january 2023, and the second year the following january 2024. If I have a Swiss bank account, I can keep it there, and then use Revolut or Wise to transfer it to my UK bank in pounds for instance. Or not have a UK bank at all and use Revolut in pounds

This seems a very good point. If I don’t come back to CH, I’ll move some francs to IB and others to the new bank, wherever this might be (HSBC seems very interesting, but it was occupied by XR in 2021 and received a lot of attention, so I’m desperately trying to choose banks that align with my committments - that’s why I was at the BAS before).

excellent idea - that you very much. I’ll do so. For now I won’t have access to the UK pension system, I only have a temporary 2-years visa and I am not paied by the UK. So I will have a ‘gap’ in my pension as well, since I won’t contribute to it for a while.

My 3 pillar - well, I’m taking it away, luckily. I made the huge mistake of doing it with Swiss Life and am happy to take it even if it entails loosing half of it. As long as I can take it back and put it on IB and have control over it, it’s fine

FYI I’d really look into the tax status, from what you describe you probably could be a non-domiciled resident in UK (esp if you’re being paid from CH).

This would avoid being a UK tax resident to begin with (and I assume you’d stay a Swiss tax resident as a result, which likely would result in more favorable taxation).

(Also sidenote, UK has a different tax year than some other country if that matters, iirc the cutoff is April instead of January in most countries, that might also impact double taxation if you end up being a tax resident in UK)

I’ve talked to people who got my same fellowship and nobody knows anything, which is crazy. Basically since it’s a fellowship it shouldn’t be taxed. And since I’ll receive it after leaving Switzerland I will not be taxed here. It might be, retroactively. The foundation that provides me the fellowship can not be considered as an employer, and neither the university where I am hosted. So basically there is a hole.

My temporary worker visa (Tier5) in the UK states my salary, but it is clear that it is not provided by the UK. And all the people I’ve talked to have no idea…

Especially if your partner stays in CH and you don’t have UK income, you probably have a good case. Note that to actually benefit from the status, you likely want to minimize the amount of money that touches a UK entity (so I’d only move stuff to a UK bank on an as-needed basis, and would avoid IB as much as possible since it’s a UK broker).

that’s a very good point. However I took the test, and I am considered as a UK resident, because I leave and work in the UK (that is why I have this ‘temporary worker visa’).

Also, in the requirements they write:

“You do not pay UK tax on your foreign income or gains if both the following apply: they’re less than £2,000 in the tax year

you do not bring them into the UK, for example by transferring them to a UK bank account”

And my foreign income is 59’000CHF so way more…

In any case, apparently we can really push for the fact that it is a fellowship that covers life expenses - so it should not be taxed…

I see, sorry!

I’ve just learnt a new English word actually. Domicile is a general legal concept. You will generally be domiciled in the country where you consider your ‘roots’ are, or the country where you have your permanent home. It is not the same as nationality, citizenship or residence. Every individual has a domicile, which they originally acquire at birth.

So my domicile will be forever the one of my parents from what I understand. Therefore I’ll be domiciled out of the UK, which means that I will be taxed only on what I will transfer to my UK bank. Now I see.

But in any case my fellowship should not be taxed because it is not income… My colleagues told me they weren’t; one of them called the HMRC 2-3 years ago, and they confirmed. Only few countries (like Austria) tax fellowships…

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.