If you spend less than ~CHF2k in a year on healthcare, the CHF2500 deductible package is the cheapest.

If you spend more than ~CHF2k in a year on healthcare, the CHF300 deductible package is the cheapest.

At no point are any of the packages in between better value.

I ran the numbers for every insurer in my commune and found that this was true for every single one of them. The cutoff point between the CHF300 and CHF2500 deductible being superior varied from CHF1.6k-CHF2k (usually CHF1.9k)

Only take a basic insurance package with a CHF300 or CHF2500 deductible

As a rule of thumb, if you are 60% confident you will spend over CHF2k in a year on healthcare than go for the CHF300 deductible. Otherwise take the CHF2500

Not relevant to this analysis but check every year for any insurer offering cheaper premiums with the web link above. Can lead to huge savings.

I think that your reasoning is based on the fact that you know how much you are going to spend in an year. I believe that it makes sense to choose not extreme options if you don’t know.

If you believe that you are going to spend between 1500 and 2500, a not extreme option makes sense.

No thats not the case. This modelling shows that it is never worth going for the non ‘extreme’ deductibles.

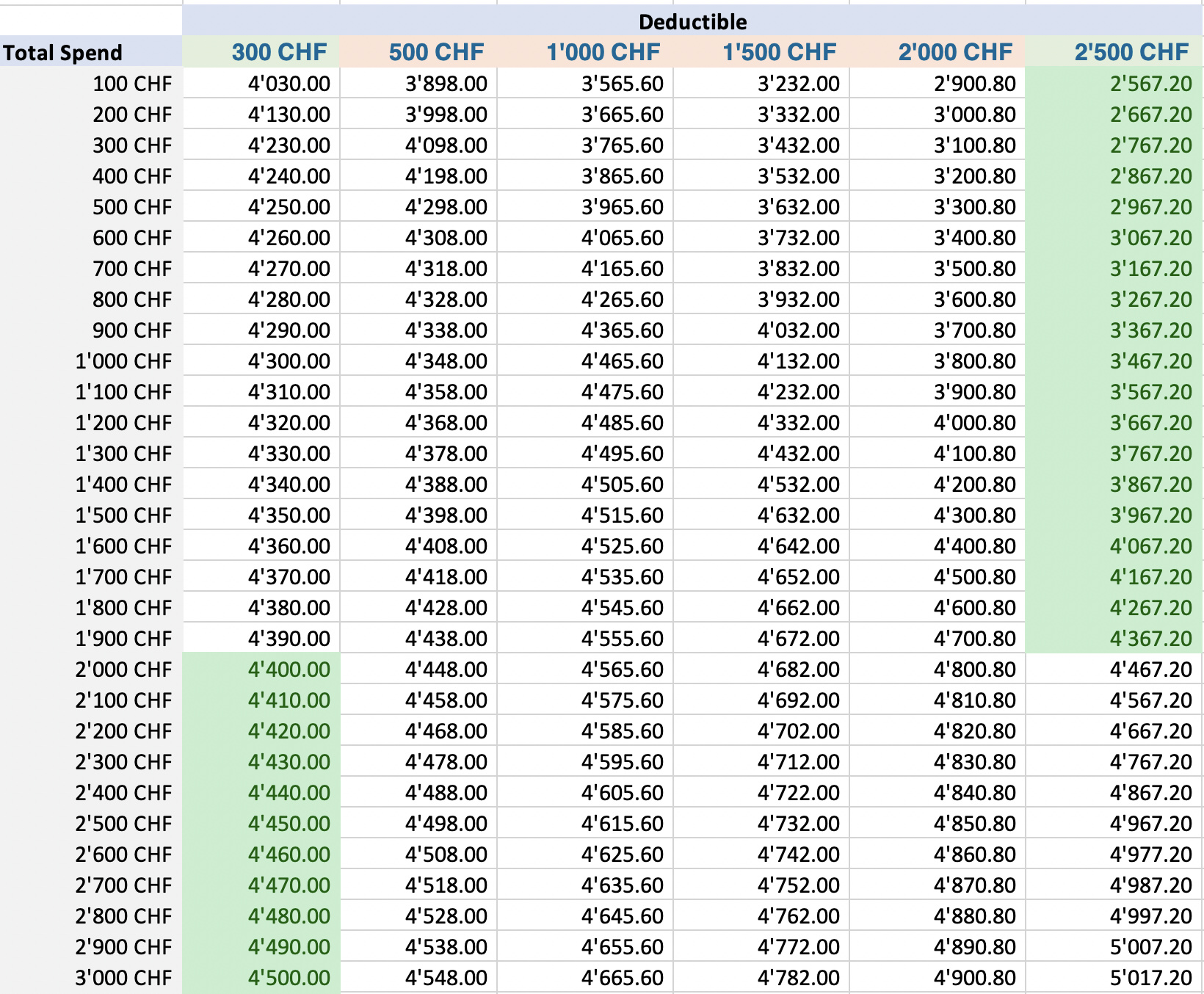

Take for example the CHF1500 row, that is if you spend CHF1500 on healthcare costs for that year. If you took the following deductibles you would pay the total amounts:

CHF 300 deductible = CHF4350

CHF 500 deductible = CHF4398

CHF 1000 deductible = CHF4515.60

CHF 1500 deductible = CHF4632

CHF 2000 deductible = CHF4300.80

CHF 2500 deductible = CHF3967.20

Here we can see that CHF2500 deductible is the cheapest.

Now if we look at the CHF 2000 row:

CHF 300 deductible = CHF4400

CHF 500 deductible = CHF4448

CHF 1000 deductible = CHF4565.60

CHF 1500 deductible = CHF4682

CHF 2000 deductible = CHF4800.80

CHF 2500 deductible = CHF4467.20

The CHF300 is now the cheapest.

For every single row either the CHF2500 deductible or the CHF300 deductible is always the cheapest option.

What you are saying is true only if you know how much you are going to spend next year.

For example:

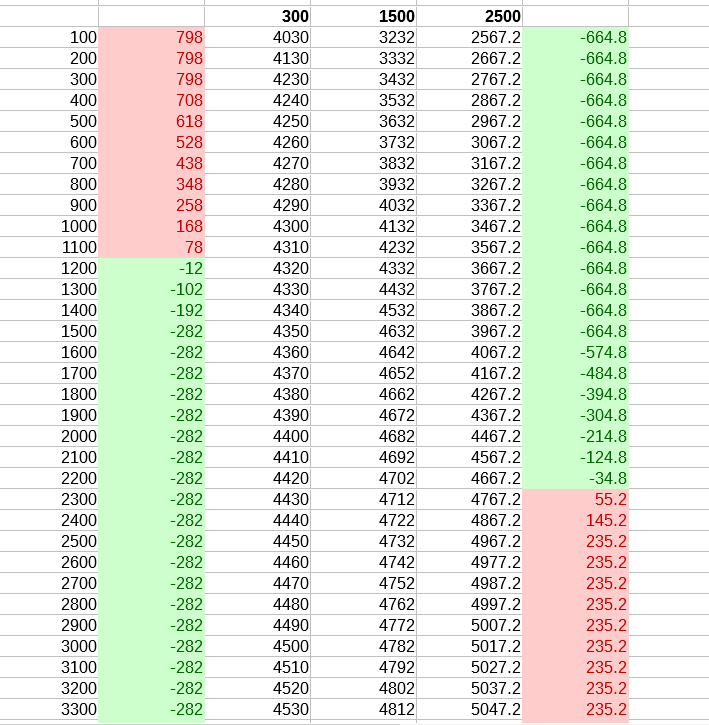

Let’s say that you think that you will spend 2000 so you go with 300 deductible. That year you are lucky and you spend only 1500 because you didn’t get sick much. If you had chosen the option of 2000 deductible you would be better off (CHF4300.80) than what you chose (CHF4350).

The next year you think that you will spend 1500 so you go for the 2500 deductible. That year you are unlucky and you spend 2000. If you had chosen the option of 500 deductible you would be better off (CHF4448) than what you chose (CHF4467).

It’s like if you buy a stock with an option to limit the losses. The option is going to cost you but in case things don’t go as you hoped, the option can save you.

If you know for sure what you are going to spend the following year they don’t make sense. In case of uncertainty of what you are going to spend the not extreme deductibles make sense. And we are in a situation of uncertainty since we choose the deductible in advance.

You are right to say that it is a bet to get a 300 or 2500 franchise (or any franchise whatsoever). But you must take the best bet, which is… the 300 or 2500 franchise depending on you. Other franchise are stupid bets.

Imagine, you bet you will not go to the doctor. If you are extremly wrong 3 years out of 4 years and you visit every hospital of the country. The fourth year you are also wrong but less wrong so you have 1500 chf of expenses. You will pay 3 * 235.2 and you will save 664.8, so in total you loose… 40.8 CHF in 4 years,

That the 300 and the 2500 deductibles are the only ones which make financial sense is a fact. I don’t know of any exceptions. The others are basically hangovers from the previous system (before health insurance became mandatory) where each insurer had its own benefit and deductible options.

The moneyland.ch health insurance comparison has the option of calculating the optimal deductible based on anticipated healthcare costs and uses the exact 2k formula you described. https://www.moneyland.ch/en/health-insurance-comparison

Great job and comparison but is not complete. It would be interesting to include opportunity costs and tax deduction. There are cantons in which you can deductthe single costs you have from taxes and is not a ‘pauschal’ number.

For the opportunity cost, if you invest the 150 chf per month of difference you are going to have more return, particularly over 20 years etc. This could even impact other deductible making them better. Particularly in the case if you advance the money and pay everything at the beginning of the year to get some discount.

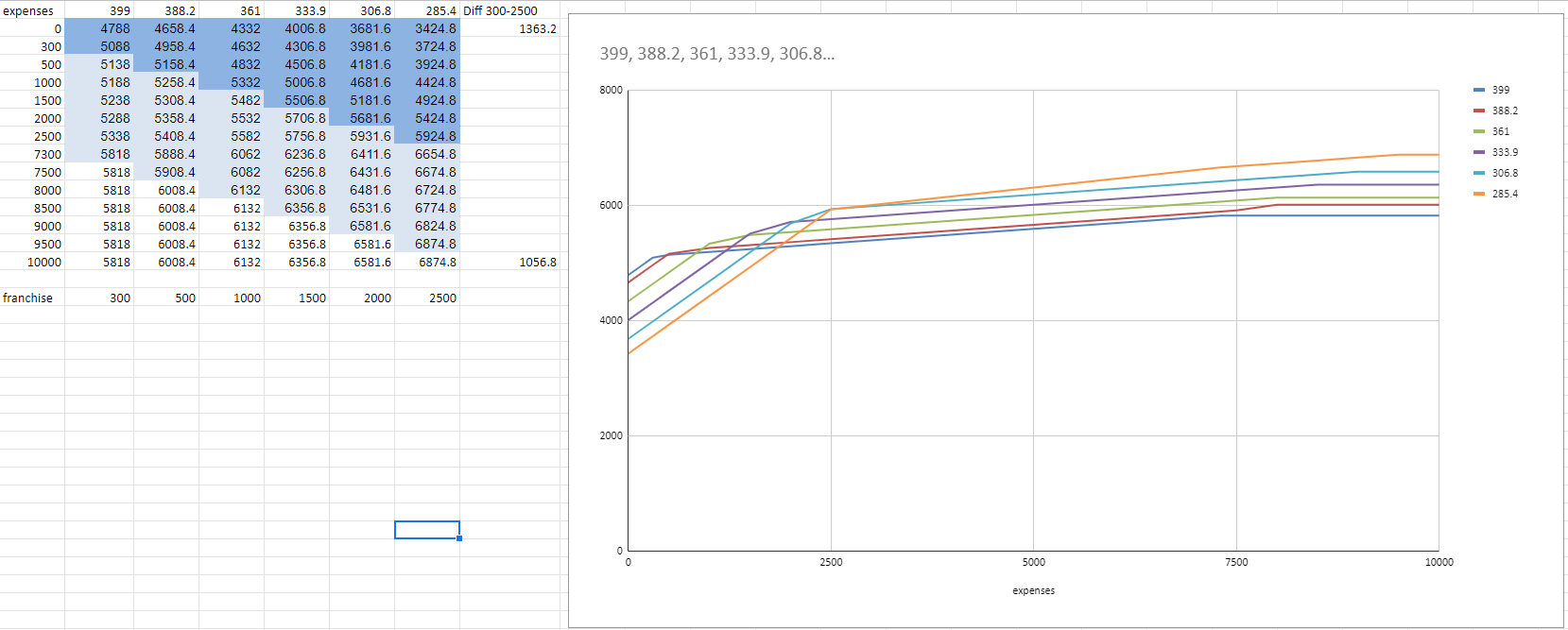

You can imagine a function like this:

TOTAL EXPENSES = function(HEALTHCARE BILLS, DEDUCTIBLE)

y = f(x)

Then for each deductible you can draw a chart, which I did already once in this forum, July 2018 (oh how quickly the stuff gets buried here). Then you can see which deductible gives you the lowest expenses for each level of healthcare bills, which as you said, you can’t predict. And then you will notice, that the middle options are never the best.

Now when I think about it, in order to get the best deductible for you, you should try to figure out the probability distribution for your predicted healtcare bills. Then you plug it into the function for each deductible and you get the expected total cost. Maybe then the middle deductibles would start making sense? Like, what if your healthcare bills would be: 50% 0 CHF, 50% 5000 CHF. Then it would be for some years the best to take the 500 deductible, and for the others the 2500 one. But since you don’t know what to expect, maybe the 1500 one would average out as the best one? Dont’ know, would need to calculate.

It’s true that probability distributions can lead to some of the middle scenarios being best but when I explored this I found the distributions so extreme that I don’t think I would ever advocate it.

To make this work complete perhaps some modelling would be worth doing though…

I was also doing a similar analysis back in 2015 or so - so mind the differences in fees (and SWICA data)…

Breaking point was again around 1800-2000 - good to see it still holds today.

However I also wanted to have a look at what happens in the extremes - if you make the worst/best possible decision.

If your expenses were zero, and you picked the lowest franchise, you would have lost (max) around 1400CHF.

If your expenses were maximum, and you picked the highest franchise, you would have lost (max) around 1100CHF.

So nothing too critical over a year, I would say.

Nevertheless, would be interesting to see the numbers today, as the costs have risen significantly.

And I continue taking the max franchise (as I am relatively young and healthy), unless I know for sure I will have a surgery or something next year (e.g. changed it for 2018, then went back).

Savings over the years would more then compensate a one year “mistake”, as per above.

I think about that function with a probability parameter as well.

Let’s say that you have a probability of 73,88% of being sick for 2500 and of 26,12% of no medical bills this is how you would compare:

Deductible 300= 4450x73,88%+3930x26,12%=4314.176

Deductible 1500= 4732x73,88%+3132x26,12%=4314.08

Deductible 2500= 5017,2x73,88%+2467,2x26,12%=4351.14

So here is a mathematical valid case in with it’s worth taking an health insurance with a non-extreme deductible.

In reality that probability parameter is also uncertain. This means that you might estimate the right thing to take the 300 deductible but then you aren’t. Then next year you think that you will pay 3000 but then you pay 0. I that case it makes sense to go for a middle deductible.

To generalize:

if you are bad at estimating how much you are going to spend it makes sense to go for a middle deductible.

If you are extremly good at estimating, there are some rare cases (see above) in which it makes sense to go for a middle deductible.

I disagree with your conclusion. Unless you have something chronic isn’t it likely you will have very low cost (maybe 1 doctor visit a year, with some normal medication, flu or similar, nothing special, <300) or high cost (catch something strange, some tests, referral to specialist, more tests, expensive med). At least that is my experience.

I’ll use your odds 74 to 26, which I find quite reasonable.

That means in every 4 year period in 3 of those years I save 1400 francs, and then 1 year I pay Fr 1100 more.

Sounds like a good deal to me!

Yeah I know, bummer if the expensive period is spread over 2 calender years. You really can’t choose when u get sick (usually), but still in the positive with the max.

But it’s like investing - don’t look at one year, look at 10 or 20 years.

Max your franchise/deductible - the only option for healthy adults IMO.

There is also one thing we haven’t covered. If I have a high deductible, I am discouraged from taking care about my health. It really has that effect on me. Got a fever? Probably some cold, just stay home a few days and it will get better. Got occasional stomach pains? Doctor recommends gastroscopy for 800 chf as diagnostic, it might find something, it might not. So I don’t do it.

At some point it might happen, that you will downplay a serious disease, just because you were not sure if its worth it to visit the doctor. I remember in Poland I went much mire often to the doctor, because it was for free in my health plan.

Totally agree with that one. I switched from 2500 CHF to 300 CHF couple of years ago because of that. I rarely went to the doctor when I was sick, because I didn’t want to spend any money if it’s not something serious. But can you really always tell that?

Now I don’t really care about my medical bills. Especially after paying the franchise.

See? That’s why we are going to be like in the US in 10-15 years. People don’t care.

Don’t plan to FIRE in CH then because it will get worse and worse.

True, I think the lowest deductible should not exist, just the same one for everyone, say 2000 chf. Plus, the obligatory insurance should only cover things that most people can’t afford, that is treatments costing over 1000 chf. I don’t see why a visit at a general doctor, which costs 150 chf should be covered. And let’s be clear, I’m only talking about the scope of obligatory insurance. People could still insure for more if they pleased.

I think some things might have gotten a bit mixed up, towards the end of this conversation. So here are some points to push back a little

Health insurers already take into account this kind of ‘bad’ behaviour you describe. Prices are set accordingly.

Yes, it’s probably bad for the health of a health insurance system, if you go to the doctor for every small thing. But it’s probably good for the health insurance system if you go check out that bump early, get antibiotics for your cough before you get full fledged peumonia, etc. The behaviour Bojack describes is probably good from a social welfare perspective, especially if you also take into account lost productivity from being sick. [But please don’t go to work if you are infectious ]

It’s a good thing that health insurers are able to provide different contracts. Insurers always want to risk select, it’s the way they can have an edge over competing firms. By only offering pooling contracts (e.g. everyone has a deductible of 2000chf) you incentivize insurers to only want to insure people with low health risks, as far as legally possible. [At the beginning of the KVG there was something similiar to that and they had to change it, if I`m not mistaken.] By allowing for seperating contracts you allow the insurers to put prices such, that people self-select towards the contract that is optimal for them. This reduces the interest of insurers to do risk selection (but it’s still there).

(The point of the OP is a fact, as far as I know. The middle contracts are just there to confuse you.)

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.