Sounds like it can (and I’m sure will in the same form or another) happen again. The question is when and at what circumstances. As we have now “everything bubble”, we may have “everything crash” and people counting on using their funds nicely growing in the stock market, may not be able to do so, at least not to the extent they think… Tough topic, tough decisions :).

5 Likes

If you buy a house for 1.5 million with a 1.2 million mortgage (80% LTV ratio) and the value drops by 25% down to 1.125 million, you end up with a LTV ratio of 107%. Banks wouldn’t force you to sell (as it would realise a loss for both parties) as long as you keep paying interest. But they would force you to amortize it down to 80% within ~10 years. So your amortization will probably increase from 13k/year to ~32k/year.

I actually had such a case in 2017 (I don’t remember the exact numbers, but it doesn’t matter). It was a woman who didn’t look after her house (the state of it was just horrible) and it was overpriced anyway when she bought it back then. We corrected the value from 1000k down to 650k. She had a mortgage of 600k and the sad part about the whole thing was that she was in a legal dispute with her sister and contacted us for increasing the mortgage to cover the costs of laywer. Not did she only end up with no money from the bank, suddenly she had to amortize the mortgage that had a LTV-ratio of 60% before she contacted us and 92% after revaluating the house. She could barerly afford it.

People just don’t realize how much risk there is involved with owning real estate. You are highly leveraged and anything can happen, prices don’t always go up.

22 Likes

This is something making me feel “a bit” better (being fresh owner). Of course it would be very bad, but good to know that I should not expect the bank knocking at my door and asking for a huge amount at once (which of course makes sense, not to trigger the loss for both parties as you mentioned).

BTW - many thanks @Cortana for those very valuable inputs!

3 Likes

Great history lesson, @Cortana! I heard about Basel I etc, but only the name, didn’t know it’s about regulating the mortgage business. So Basel III should go into effect in the future and it will be stricter for the bank? Maybe this could be a trigger for the next correction. Because ok, the bank will play nice as long as you pay the interest. But if they themselves don’t fulfill their obligations, they will have no choice.

One other component of the mortgage scheme is the Pfandbriefbank. Maybe you could tell us a bit about it, too? Do you think it could also pose a risk for the banks?

Since we’re talking about scary mortgage stories, in Poland people used to take mortgages in CHF. In the best moment you only paid 2 PLN for 1 CHF, but shortly afterwards the exchange rate exceeded 4.00! Many people had LTV over 100%, even though there was no real estate crash (in PLN). To this day thousands of people battle with banks in courts, saying they were tricked into CHF loans…

4 Likes

The Basel contracts are for a a couple of things: minimum capital requirements, liquidity, leverage ratios etc. It’s goal is to create a framework of rules to strengthen the financial system. But of course mortgages are a big part of that. Basel III implentation did already start a couple of years ago with a couple of banks. But the major widespread implementation in the EU etc. is expected to take place in 2023+. I don’t think that it will trigger any correction, quite the contrary. The stricter rules should reduce the overall risk of debt.

As RE prices in Switzerland keep increasing (5-10% in the last 12 months alone), I expect a stronger regulation from FINMA in the near future. Possibly a total restriction for using 2nd pillar, increasing capital requirement from 20% to 25-30% (they already did that for rental real estate in 2019) and other things.

My knowledge regarding Pfandbriefbank is very limited.

P.s. The same thing happened for some Germans btw. Crazy thing.

6 Likes

Yes, but in order to reduce the risk of debt, you need to reduce debt. In order to meet Basel III restrictions, the banks could be reluctant to give highly leveraged, high risk loans. This could trigger a correction in real estate prices, as people could not afford a loan so easily.

2 Likes

I remember discussing that with friends in 2013. Now it’s way too late. Everybody (SNB, FINMA, politicians) is too afraid of being the first to intervene and being accused of crashing the market.

1 Like

There are so many similarities to 30 years ago. Back in 1985 pension funds became mandatory In Switzerland which lead to a sudden increase in real estate investments by institutionals. We see that too now as pension funds are looking for alternatives to bonds with zero interest. 25% of their asset allocation is real estate, 20 years ago it was 17% and 10 years ago 20%. Pension funds keep allocating more and more to real estate which is making everything worse. Interest rates on mortgages were historically low back then, they are too now. Prices doubled from 1980-1990. They doubled again in the last 10-15 years. So what will happen next? Rising interest rates combined with more restrictions from the government?

Will history repeat itself?

5 Likes

Market can also stagnate for very long time.

If so:

- Financially, You would be better off investing in VT

- However those buying won’t face doom day, just pay back their mortgage but not benefit from RE appreciation

In that case the question you need to ask yourself is how long do I want to be in Switzerland for. If the answer is over 20 years then you can risk to buy

3 Likes

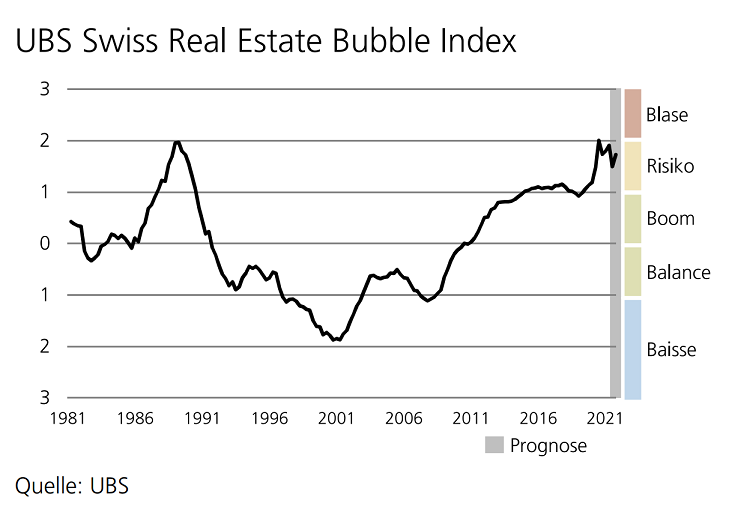

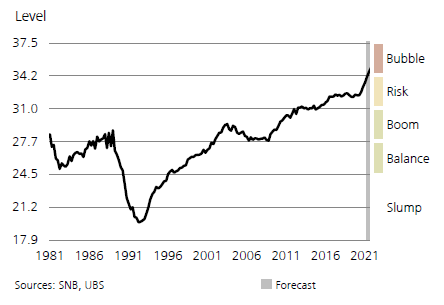

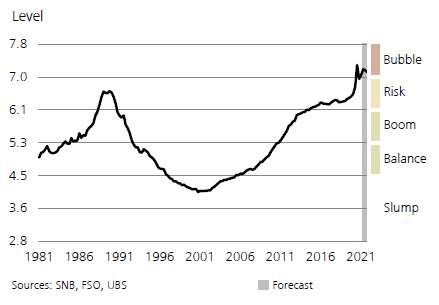

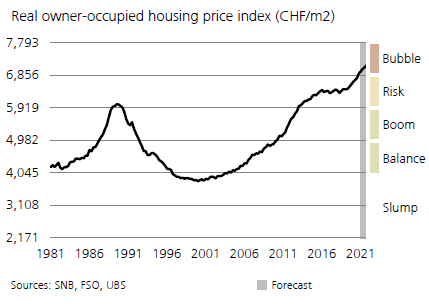

Note that all 3 of the sub-measures used to build the aggregate UBS index that measure prices are all in “bubble” territory:

Home prices to annual rents

Home prices to household income

Home prices relative to consumer prices

The other 3 measures used to build the UBS index do not measure prices. They are input variables which influence prices. These are all outside of “bubble” definition and are thereby keeping the overall UBS composite measure out of “bubble” too:

- Construction relative to GDP: defined as “in balance”

- Value of mortgages relative to disposable income: defined as in “risk” phase

- Buy to Let mortgage applications: defined as in “boom” phase

5 Likes

Do you have insights how institutionals behaved during the crash - did they hold or sell?

If they were mainly swiss pension funds with low leverage I assume they held and rode out the ~20 yr cycle until inflation led to higher rents and prices. If they sold it would have worsened the issue (increased supply)

1 Like

Don’t know. But this whole topic might be a good a idea for my bachelor thesis

16 Likes

They are, though there are some redistribution mechanisms between Gemeinden and Kantons.

The situation arises when there is both dense and isolated living amenities in the same Gemeinde. Some taxes take that somehow into account (depends on the Gemeinde, many (most?) don’t) - tapwater, sewers, electricity, urban wastes - some are paid by the general taxes and don’t take that into account (roads, protection from natural hazards, pubic transportation and so on). The Gemeinden can levy some additional taxes (“appel à plus value”, in French) on the local population when new infrastructure (mainly roads) are built for the area (or existing infrastructure is significantly improved). That would be part of the political risk @Xorfish is talking about (in the Walliser Gemeinden I know, it used to never be done but is becoming increasingly popular).

One could say that the people living in single family homes are usually richer than those living in flats and, as such, pay more taxes to contribute to the pool, so are not really subsidized in the end (and would actually subsidize infrastructures for other people in the Gemeinde by paying more taxes) but you can also have people leveraged to their knees, with no taxable wealth and heavy deductions on income taxes, paying very few taxes while adopting a high standard of living. My previous Gemeinde was facing this issue.

3 Likes

And between cantons as well afaik. Péréquation financière nationale

4 Likes

Real estate is not an asset class that should be looked to be sold after 1 year or so but to keep longterm for 10-15 years. Taking prices from now I am sure in 10-15yrs prices will be higher than now as inflation does the math. It will devalue your loan on the one hand which is good to have a loan longterm and at the other hand it will increase the value of your property. Interest rates might increase but the will not increase as much as we know it from the past. So for speculation purposes I would not go for real estate as a long term investment for sure…

1 Like

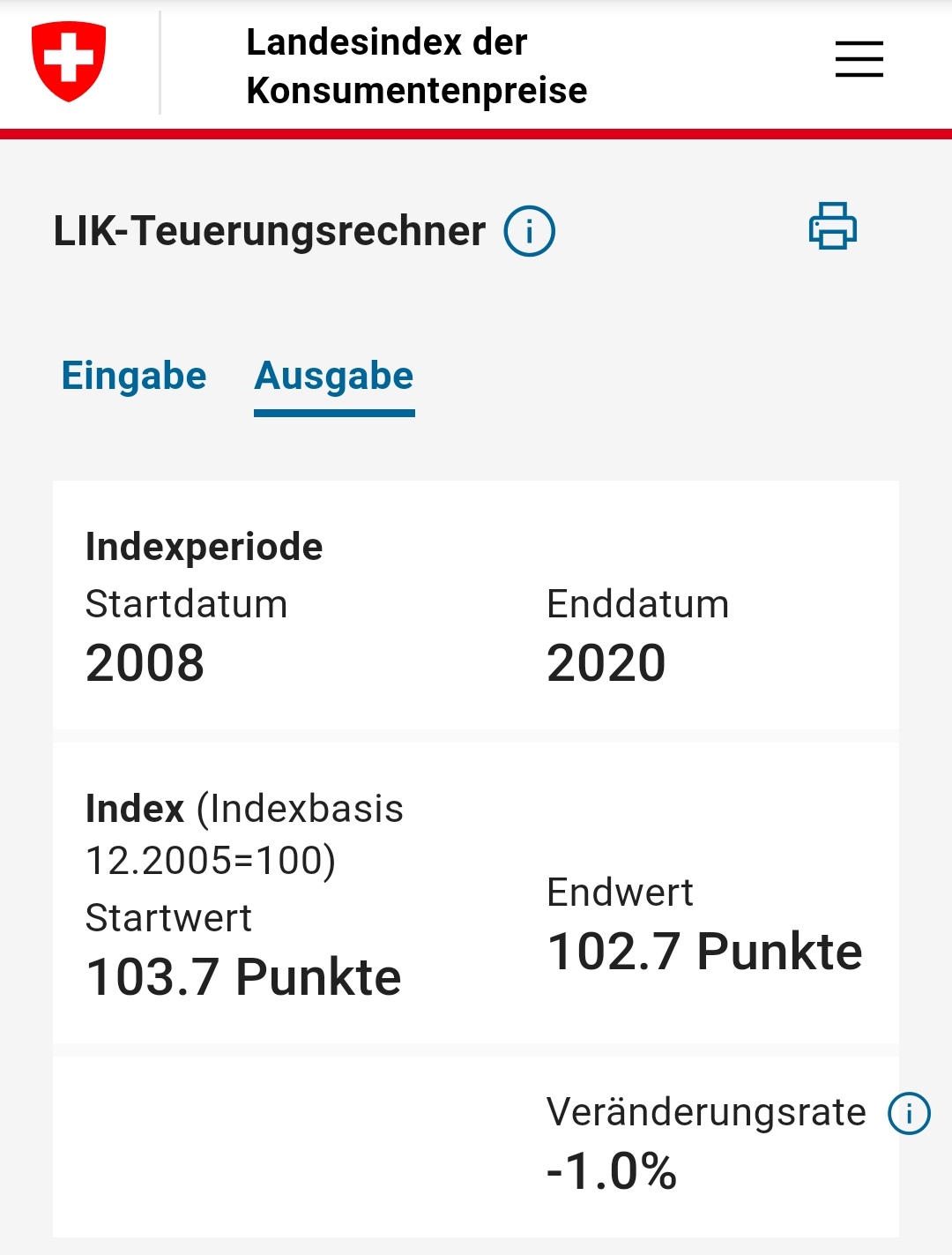

What math? For the last 25 years the overall inflation has been on average under 1%.

Whatever you win on inflation or immigration can be easily offset by the fact that currently we’re in a bubble (if we really are).

The current supply and demand of real estate, which is only a small portion of all real estate in existence, sets the price for all properties in the country. People who live in their own house don’t sell it just because its price went up 100% in the last 20 years. So the current positive conditions for the real estate market would have to persist into the future, to secure high prices.

3 Likes

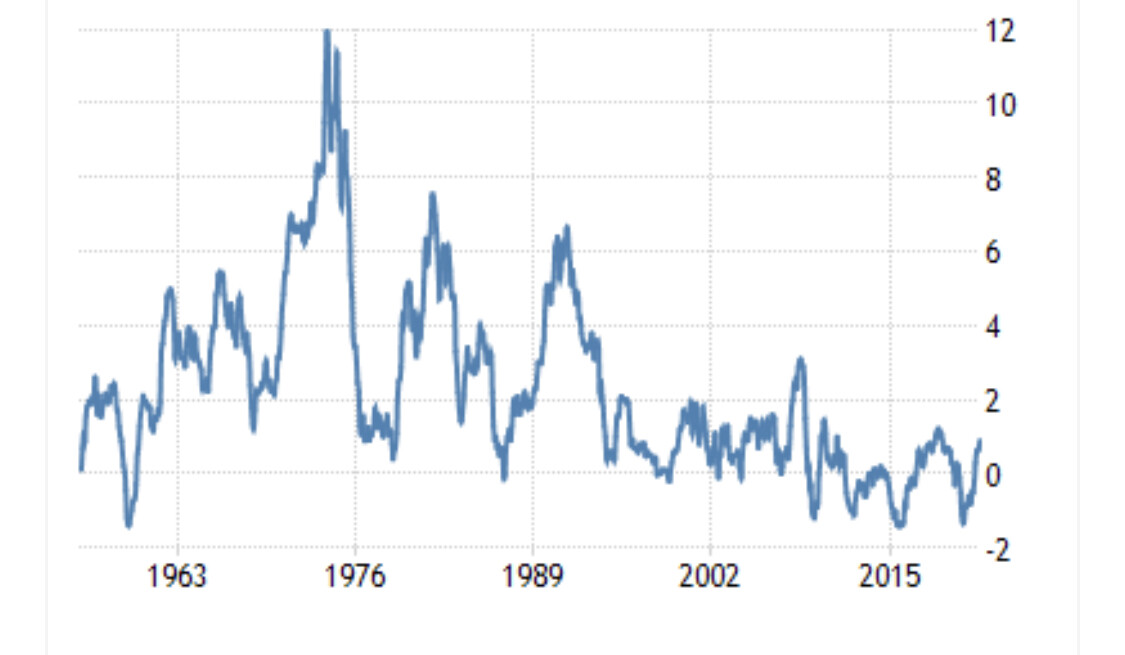

Over the last 40yrs the avg inflation rate per annum was 1.7%. So for a 15year period it would mean that your reals estate increases just on this Basis by 25%. The same value your loan is worth less…

Avg. mortgage interest rate in the last 40 years was 4.5%/year.

Switzerland will probably be like Japan now…no inflation for decades.

3 Likes

My doubt is whether we can assume 15 years is a long enough period to assume consumer inflation = house price inflation

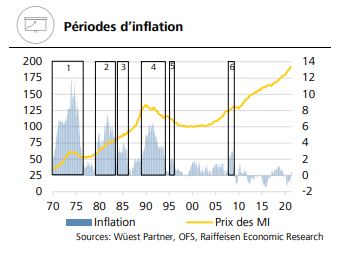

The article I shared above (page 14 of the French version) discusses the mechanics why property prices and consumer prices are not correlated in the short term.

Prices of houses (MI = Maisons Individuelles) have decreased during prior periods of consumer inflation in the past - for example periods 4 and 5 below.

There can be a lag: higher consumer inflation means higher interest rates which puts downward pressure on house prices, it may take a while until inflation leads to higher salaries and rents and then higher house prices again

[Edit: the same article says that if you exclude rents from the consumer price index, consumer prices have decreased 4% since the 2008 crisis. Rents increased 15% during this period - the significance is that rents have moved in the other direction to other consumer prices during a 13 year period]

1 Like