I’ve been working in CH for 8 years now and I got interested in my second pillar value when calculating my net worth. While checking the insurance certificate received this year, I’m confused as I have the impression my employer is not contributing enough (it has the reputation to be one of the best pension fund in the country though).

It’s a difficult topic, I’ve read both the law and the rules of this specific LPP, but I’m still struggling to understand. I’ve asked them by phone already and it wasn’t conclusive, I’ll keep trying but would appreciate having an external opinion.

Here’s an anon version of the insurance certificate:

The first arrow is on the line “Sum of all employee contributions”.

The second arrow is on the line “Vested benefits”, i.e. what I could take away if I leave the company.

I observe that:

There’s no concrete amount near “employer contributions”

The sum of all my contributions amount for 67% of the vested benefits

I’ve always read and heard that the employer is supposed to contribute at least 50%, so my question is whether it’s normal that my contribution is in fact 67% ?

I can’t be sure of what’s happening here, but here are a few points which may be of interest:

The contributions (both employer and employee) to your pension fund are used for some insurances (death and disability) and your retirement capital. Thus, your vested benefits should be something like total contributions - insurance premiums + interest on vested benefits.

Normally, before 25 yo all your contributions go towards the insurance premiums, none towards your retirement capital.

You may be voluntarily paying more than you have to, while your employer sticks to his minimum. Your employer does not have to match your contributions.

The nominal contributions of the employer and the employee are usually displayed on these certificates (or at least, they’ve always been on mine), separated in different categories among which, usually, “savings”, “risk” (the risk insurance part of it) and “administrative fees”.

Is there something on the back of the page or a second page, somewhere? What does the art.61 of the “règlement” say?

Thanks @anneaun, this could explain the difference of numbers, but I wonder why it’s not shown in a more transparent way in this case. Anyway I didn’t do any volunteer contribution yet to my second pillar and I don’t remember having been presented with any option such as choosing how much I contribute, it’s just deduced from my salary.

@Wolverine Thanks as well, no there’s no second page. Article 61 defines how the employer contribution is calculated, it translates to:

The yearly amount of the employer contribution equals:

1% of the sum of all contributing salaries of those insured to the risk insurance

11.1% of the sum of all contributing salaries of those insured to the full insurance

As I don’t know these numbers it’s difficult to figure out what’s the amount. I wonder if this means that each employee receives as employer contribution11% of the average salary (80-85k), which should then be ~8-9k.

Is it a pension fund from the state(like CPEV for Vaud) ? with a “primauté de prestation” model?

Because in this type of fund the calculation is a bit more complex

that’s stange, according to BVG there is a rule of how much the employer/employee have to contribute as a minimum to the savings part:

Age 25-34 (7%)

Age 35-44 (10%)

Age 45-54 (15%)

Age 55-64/65 (18%)

This only applies to the BVG portion (CHF 24’675 - CHF 84’600), and as legal minimums. Some pension funds also increase these rates. If you earn above 84.6k, that portion might have other savings %, there the pension fund has more freedom in deciding what they want.

It’s indeed the one you mention. I didn’t transfer any fund because this is my first employer.

@kane That’s interesting thanks, I didn’t know it was capped at 84’600.-, maybe this is why the employer part is not higher. Although I’m still far from figuring out how all this is calculated.

the main issue I see is that the statement has no details. Ideally, there would be a statement on how much is contributed towards insurance, fees and savings portion, and of these numbers, how much of it by you, respectively by employer.

The 86.4k is the BVG max, the salary above this is usually also insured but not according to the BVG rules, but trough the pension fund’s own regulation.

After having gone through the pension plan document linked by @wapiti, I’ve got to say that’s a funny way to calculate pensions and rights to capital.

Your pension amount is a fixed 1.3% of the insured salary per year, no matter your contribution amount (which grows with age), as per Appendix B.

The equivalent capital depends on the accumulated pension amount (a factor of how long you’ve stayed in the company and your insured salary) and a multiplicative factor depending on age and gender, as per Appendix A.

On a global scale, the employer will contribute 11.1% of all insured salaries, which is more than the max employee contribution of 8.9% at age 65, however, that contribution will be more beneficial to older employees who have been working in the company for a long time than for younger and/or short term employees. If we took an equivalent on an individual level, there would be situations where the employer contributes less than the employee to the calculated benefits, this seems to be your situation. This isn’t how things are processed, though: things only happen on the global plan level, trying to project things on an individual level seems foggy at best. I have no idea on the legality of it.

In my opinion, this is a case worth discussing with an independent, competent, pension fund specialist. I don’t have any to recommend.

Edit: on a side note, the pensions seem pretty generous. No idea about the capital if you leave before retirment age, I haven’t made the calculation.

The 2nd pillar system is terribly opaque. And most people do not realise that individual situations can vary greatly depending on their pension fund provider, which is to be picked by their employers.

Imho it must go away. I would love to see the 2nd and 3rd pillar merging with one part compulsory contributions (with employer-matching, 2nd pillar replacement) and one part voluntary (3rd pillar). Provider to be chosen by the employee.

Wow, thanks a lot, this makes a lot more sense. I’ve read this document many times and have never been able to synthesize it as good as you did.

I was told something similar on the phone actually, that there is no precise answer to my question as it’s all handled globally. I’ve never found this answer satisfying, but it seems to actually be the only realistic answer for this pension fund. I wonder why they made it this way.

I was also told by more senior colleagues that this pension fund benefits better the employees on the second half of their career, but when I asked why, no one was really able to answer.

At the end of the day I’m satisfied if I know it’s fair, even more if I can understand how it works. It’s not my intention to legally challenge this, I just wanted to be sure that I wasn’t victim of any kind of calculation error with my 2nd pillar.

Having seen other LPP certificates from my friends and wife, I found theirs much more detailed and transparent.

This one is pretty weird. If you bring 20k at 30 yo or 20k at 40k, the value is not the same. It’s a mix between “primauté de cotisation” and “primauté de prestation”

I have never seen this type of plans…

To sum up your certificate, it’s seems that you have contribute 40k and the employer has only contributed 20k. So in your specific case, the current plan is bad.

I would assume that the plan was pretty generous in the past, but it wasn’t sustainable. So they decided to reduce the deficit with new rules, but tried to keep the current level of pension for older employees and avoid backclash/strike. With the new rules, the new/younger employees seems to finance older employees and retirees.

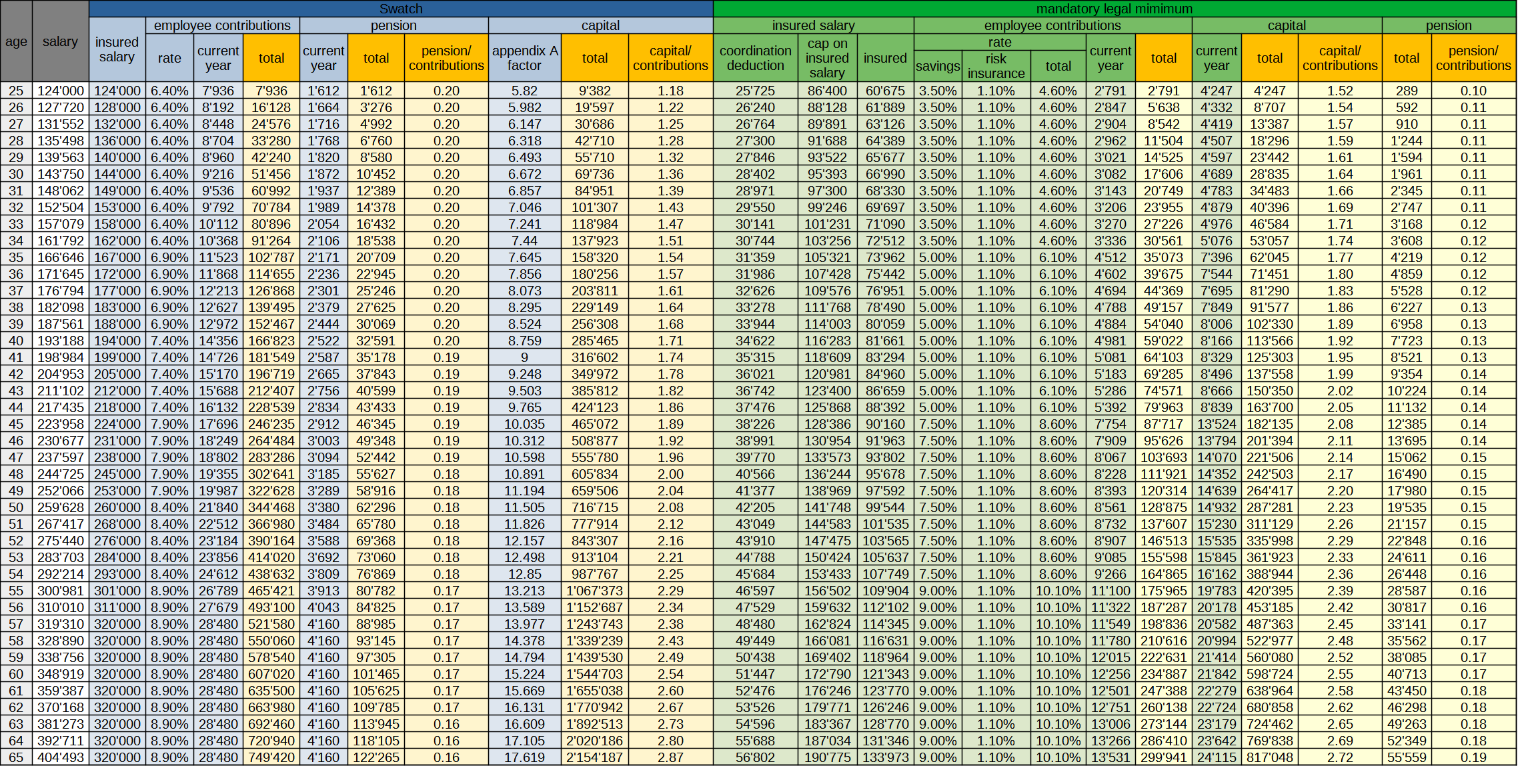

It’s hard to come up with comparisons. I’ve tried to do a very flawed table just to give some insight, comparing the Swatch plan to the mandatory legal minimum for a male (I’m biased toward my own gender ) working there from age 25 to 65. The plan seems mostly in line with it, except that, for high salaries, it applies to a greater amount of contributions (more contributions, more deductions and more benefits). There are way better plans for high earners out there.

Assumptions:

2023 gross salary of 124K (nominal salary displayed).

annual salary growth of 3%.

inflation of 2% p.a.

the coordination deduction and the max insured salary increase by 2% p.a., following inflation in the mandatory legal minimum plan.

contributions of 1.1% (employee only) for the risk insurance part of the policy in the mandatory minimum plan (my last two plans had that).

the capital in the madatory legal minimum plan increases by 3% p.a. (interests), that is 1% above inflation.

the pension is converted with the full 6.8% mandatory rate (only mandatory contributions are taken into account).

It doesn’t take into account the risk insurance benefits (I haven’t read them). The “pension/contributions” and “capital/contributions” columns try to show the benefits per unit of contribution that the plans grant in regards to retirement savings (the higher, the better).

To note that, for a higher amount of contributions, most pension plans wouldn’t offer the full 6.8% conversion rate between capital and pension benefits so the pension part of the Swatch plan is attractive in my opinion (but you have to be working there when you reach retirement age to benefit from it).

Hidden in the numbers (I ran on the principle that it doesn’t matter to calculate employee benefits):

For the Swatch plan, it’s part of the plan’s benefits (since the pension fund would probably offer less without it).

For the mandatory legal minimum, it’s in the capital accumulation (that is calculated with 2x employee contributions, so a 50/50 repartition), which then gets converted into the pension at the 6.8% rate (so it’s in there too).

I had forgotten to round up and cap the insured salary in the Swatch plan, I’ve updated the table in my post above as well as the Swisstransfer link with the new file.

Edit: did it again @ 20:55 GMT+2 for minor formating issues.

Thanks for all the work ! Although I don’t understand everything here, I take it that it’s still a good pension fund, but it mostly matters if I stay in the company for my whole career.

The more I read into it, the more I’d prefer if all this was managed as a 3rd pillar instead. I put some of the money, my employer puts some of the money, I decide to mix all that into a World MSCI fund and forget about it. Probably better returns and much more transparent.

By the way, since we’re on the LPP topic, my assumption was that the employer had to contribute to half of the legal minimal contribution (half of 7% for my age class). We find this information everywhere online and many people mentioned it to me IRL, but I’ve yet to find where in the law this is stated. Any idea ?

I’ve been through the LPP Law text and didn’t find any mention of the employee/employer contribution ratio. The closest is in art. 46 al. 3, however the whole article focuses on people working for several employers, which is not my case.

Edit: For example this non-governmental website mentions that the employer should contribute 3.5% and the employee sees 3.5% deduced from his salary sheet. On one of my salary sheets I see a gross salary of 9’741.-, and the employee contribution deduced from it is 663.-, which is 6.8%.

So it seems I contribute a lot, but I still don’t see how my employer’s contribution would be 3.5%…

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.