Found this on ch.ch, although it’s not a legal text:

Les cotisations au 2e pilier doivent être versées en parts égales par vous et votre employeur (mais celui-ci peut aussi décider d’en payer plus de la moitié).

It confirms the employer should pay at least half. Now, how much of all this should be part of the vested benefits when changing company?

A disclaimer that I am not a pension fund specialist but just a random guy on the internet who likes to discover/understand things and often gets carried away. Others may have better insight.

For the pension part, it looks very good to me. However, if you leave before retirement age, it seems to take quite some time to take off. It seems to me to be designed for employee retention.

The employer’s contribution should be at least equal to the sum of the contributions of all its employees.

La cotisation de l’employeur doit être au moins égale à la somme des cotisations de tous ses employés.

So it seems they are operating within the scope of their discretionary margin. You’d have to decide whether the whole package of your current employment suits you (base compensation, bonuses if applicable, enjoyment of the work itself, ambiance, 2nd pillar, other benefits) and decide on your next course of action, if any, accordingly. If you don’t see yourself staying 10+ years in this company, the pension scheme is a negative for you, at least in its retirement savings part (but it could be compensated by other things).

I think most people here would like it more too. However, not everybody is financially literate and many enjoy just receiving the money they think they’re entitled to without having to ask themselves questions about it. Your plan is perfect for them.

I would prefer a 3a-like solution for myself but, from a common good perspective, I’m not that sure it would be the best option (also, people who don’t have enough retirement assets are supported by complementary AVS/AHV benefits, which are paid for by taxes so it’s in our interest that people reach retirement with enough assets even if they’d have a tendency to squander them on the way (by either investing too conservatively and not having enough when retireing or too aggressively and gambling it away).

“Art. 66 Abs. 1 BVG legt für den obligatorischen Bereich den Grundsatz der Beitragsparität fest; für den überobligatorischen Bereich ergibt sich dieser Grundsatz aus Art. 331 Abs. 3 OR. Diese beiden Bestimmungen verlangen jedoch nur eine kollektive oder relative Beitragsparität, nicht eine individuelle: Die Summe der Arbeitgeberbeiträge muss mindestens gleich hoch sein wie die Summe der Arbeitnehmerbeiträge. Das schliesst nicht aus, dass einzelne Arbeitnehmer mehr bezahlen als andere und auch mehr, als der Arbeitgeber für sie persönlich leistet”

Oh, I missed that one. However the ratio it mentions seems to be on the sum of all employee contributions, rather than for an individual. I guess it’s all put in a common basket and redistributed later, and there’s no such thing as individual accounts as with 3a.

Yet, assuming my employer puts at least the same amount as me, it’d mean that together we’ve contributed 82k CHF, and what I can take with me when leaving would only be 62k CHF. Seems a bit low, but maybe the difference lies in the risk insurance.

I would prefer a 3a-like solution for myself but, from a common good perspective, I’m not that sure it would be the best option

Yes I completely agree with this, it was more of a rant. I’d appreciate more transparency behind this fund and the whole LPP system, but I agree with the general idea of forcing people to contribute to a fund designed for not losing the money, and ensuring they won’t need more after they retire. I have older family members who burned part of their LPP with terrible real estate investments when the system was more liberal (vacation house) and who are now in a difficult financial situation after retiring.

My understanding is that your plan is designed such that younger employees pay more contributions than the employer and older employees pay less contributions than the employer. All in all, the employer contributes (sensibly) more than all employees together, which means that for a whole career path in the company, your benefits would be likely to be better than those of a plan where the employer and employee contribute 50% each.

We can’t dismantle savings/risk premiums and employer/employee premiums per employee, that is not how the fund works. We can, however, make quick and dirty assumptions to try and compare with other pension funds structured differently. It’s very approximative, it’s very dirty and it’s downright not what happens in reality, but it can help to understand what may be happening.

The terms of the plan posit that employees of 24 years of age only contribute to the risk insurance and do so at 1% of the insured salary. The employer must also contribute 1% for the employees who benefit from the risk insurance. I’d posit that the total risk insurance premium could be assumed to be roughly equivalent to 2% of the insured salary, paid 50/50 by the employer and the employee.

In order to compare with other plans and since you can get the pension only if you retire while employed there, I’ll consider only payouts in capital going forward.

There are three parts of benefits to your pension plan:

the risk insurance, which I haven’t studied at all.

the new capital your contributions and the contributions of your employer buy.

the rate at which already accrued capital grows.

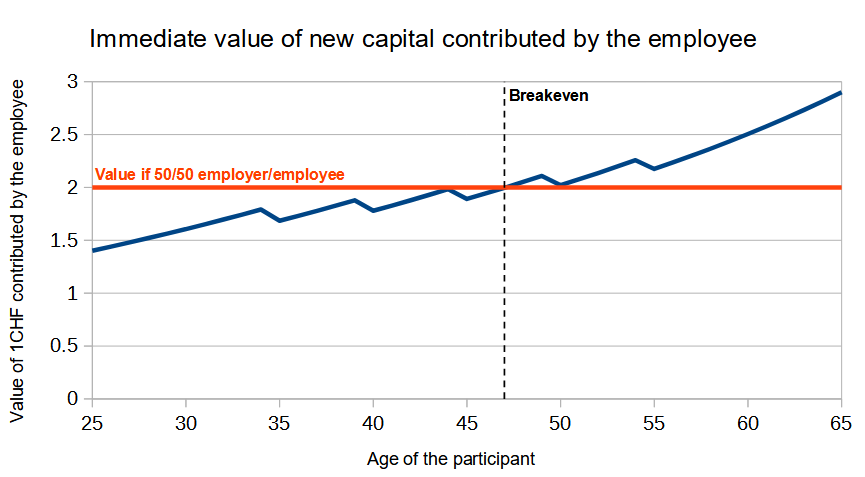

For 2: Using the 2% assumption on the risk insurance premium, this is what your contributions would buy you (using the male table):

It depends strictly of the age (and gender) of the participant (x axis). The red line is what your contributions should buy you if your employer contributed as much as you do to your specific benefits. Each 1 CHF you contribute should be matched by the employer and, as such, be worth 2 CHF.

We can see that younger workers pay more than the employer and get less benefits from the plan than older worker. The breakeven is at age 47. If you are younger, you are subsidizing your older coworkers. If you are older, your younger coworkers are subsidizing you.

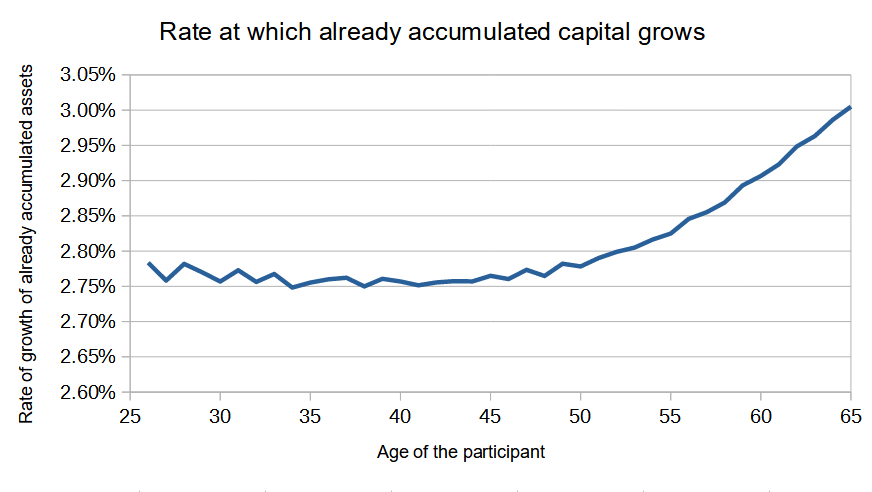

For 3: the rate at which already accrued capital grows also depends solely on age and gender. However, since it applies to all the already accumulated capital, it favors workers who have spent more time in the company (and have participated in the plan for longer) more than new workers.

It varies between 2.75% and 3%, older employees get a better deal.

So, your employer participates more to the benefits of older employees and they get rewarded with a better rate of growth. All of that is fixed and in no way depends on the returns the pension fund manages to do on the markets, which means they may have to adapt their terms if they can’t sustain it.

To note that many other pension plans, notably all the plans I’ve been a part of, subsidize already retired people with the contributions of those who are still working. They do that by applying a ridiculously low interest on the already accrued capital (I’ve had 1% this year, which is the highest I’ve had in 5 years, wohoo!) which allows to divert more of the growth of the capital they have invested toward paying the pension amounts that they are liable for.

Edit: one of the benefits of your plan that I would take into account is that it scales all the way up to CHF 320K of salary. Not all pension funds do that (some even stop at the legal minimum of roughly 90K). 2.75%-3% guaranteed returns with a tax saving on top is a pretty good deal so that has its own value.

Thanks a lot for compiling all this information and explaining it in such a clear way! I understand better, and it makes sense given the values of the company/group as well.

Note that this current plan has also already been downgraded a few times in the past years, especially during covid.

It could be designed in a way that we avoid those pitfalls:

Employers could wire both employees and employers contributions to an escrow account, and then the employees give instructions to the escrow account manager once they have chosen a provider. Eventually, the escrow accounts could be managed by AHV, so the overhead would be rather small (already exist, employers already working with them) and would guarantee employees have no direct access to the cash.

Restrictions on the investment strategies can be put in place (like it is today with 2nd pillar) to make sure they are not too conservative nor too agressive.

Kind of like the Swedish model. And if the employee does not react, it goes to the Swedish national fund (which has a rather good performance and low costs).

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.