- I am selling BOXX and buying VT at each 2,5% drop from the last one

- I also filled in the car tank today (almost cried)

- I checked to heating oil prices (really cried) - but I can’t order at this price, you think it will go up more?

1 Like

They can. The US are apparently wargaming crude oil reaching $200 per barrel (double its current price).

Why crying? Higher energy prices were always a hazard we could be exposed to at any point in time with a meaningful warning coming in 2022. They’re not that unsustainably high right now unless one is exposed to needing a lot of it for their professional activity with an inelastic ability to rise the price of their own services/products.

2 Likes

The way I think about it is:

- WAIT: I can wait and hope things get better and prices come down so I save some money

- BUY: Or I can buy now and end up paying more if prices come down later

But if things get worse and not better (I will need to fill up anyway by this time next year at the latest if not before). Then:

- WAIT: Prices could be even higher, or in extreme cases be subject to rationing or shortages

- BUY: Can ignore the noise until time to fill again next year and saved some money

The tank is half full so I only have to fill half. I’m OK to pay a premium now for peace of mind. My own view is that the downside risks have been greatly underestimated and the severity high. Everybody is relaxed now, but I can imagine panic happening in a few weeks. I’d rather get ahead of that.

I spoke to the oil delivery people during covid times: there’s limited capacity of trucks to deliver fuel. A lot of people held back hoping for lower prices and then experienced delays as when orders finally all came at once, there was insufficient delivery capacity.

I normally top up in summer during low demand season and hopefully low oil prices. I actually wish I had a bigger tank to allow for building up some stockpile during cheaper times.

My motto is: if you’re going to panic, panic early! (or at least earlier than everybody else)

5 Likes

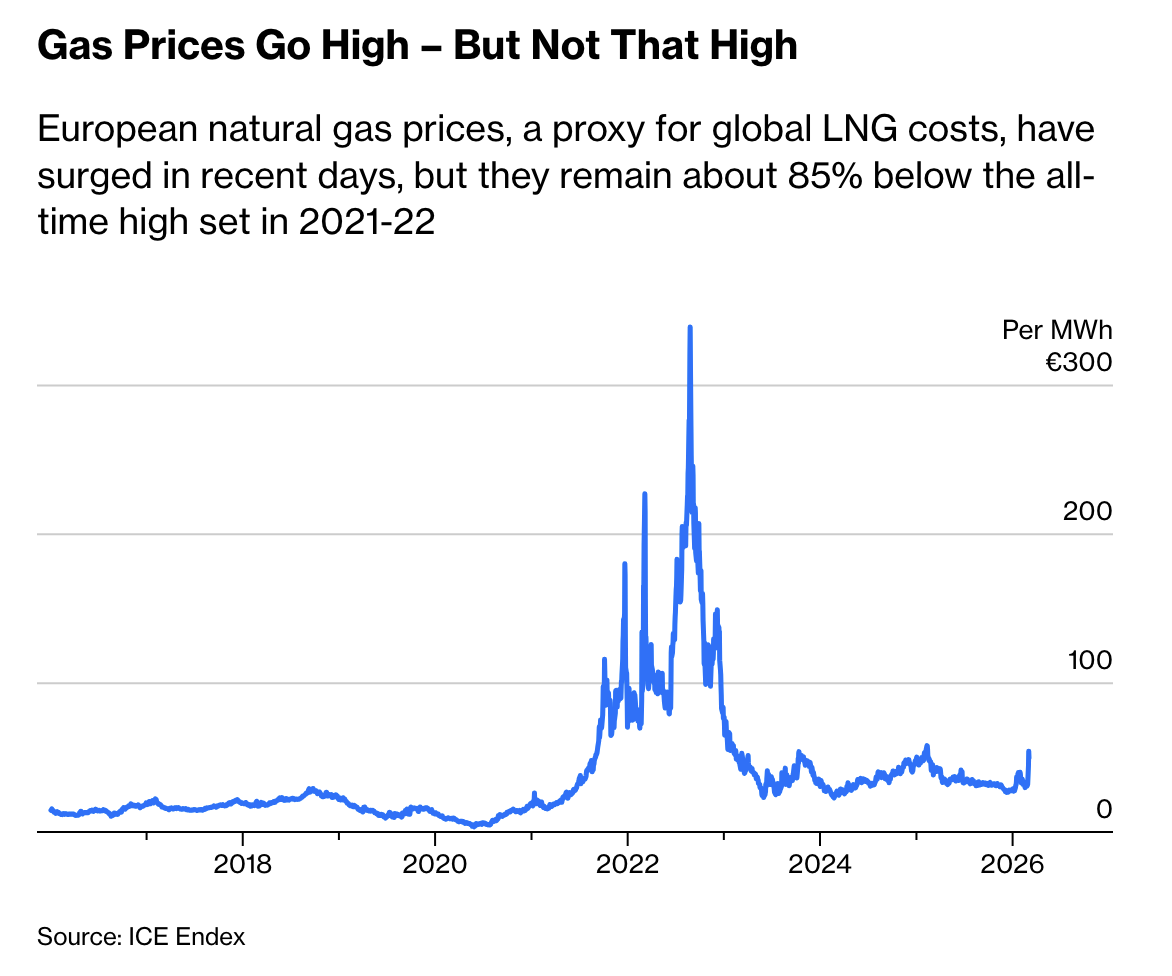

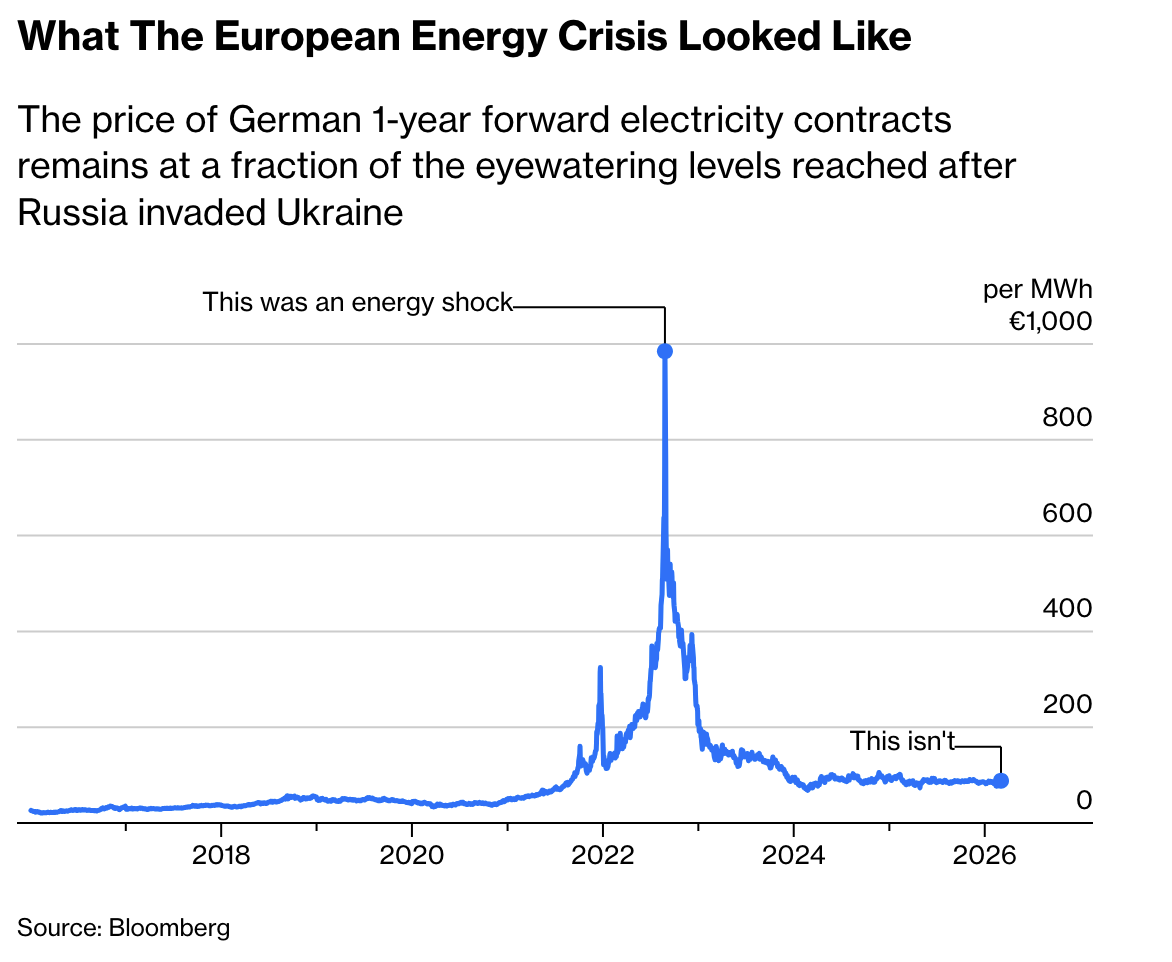

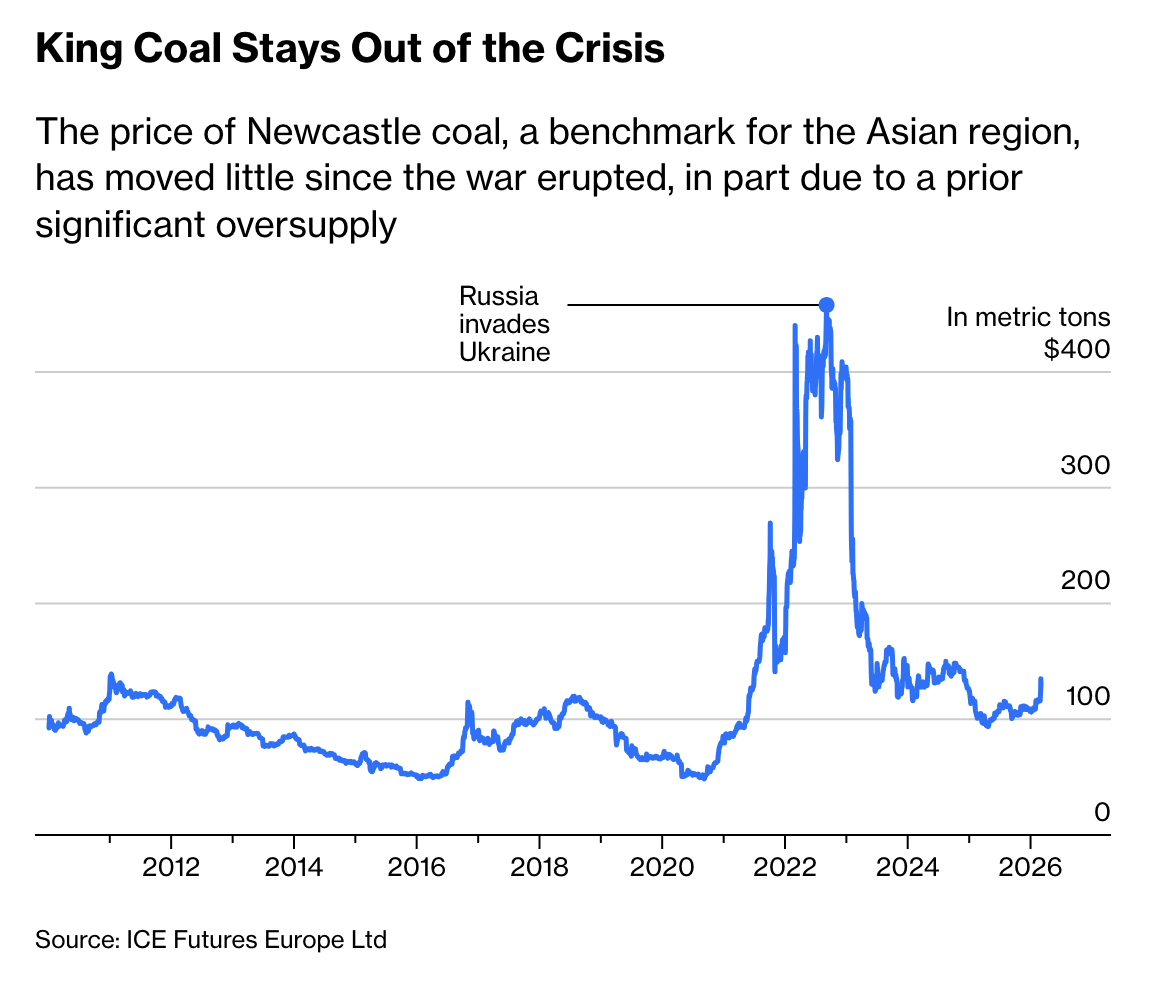

We have forgotten how bad the European energy crisis of 2022 really was. (..) It may still get uggly. Worst-case scenarios are horrible. But we aren’t there yet.

Source:

3 Likes

Don’t forget that the disruption hasn’t properly happened yet.

The last LNG tankers to leave before the war just arrived. There are still local buffers everywhere that can be drawn upon. Maybe some emergency supplies to be released.

We will only start to see the impacts in the coming weeks.

Also, don’t underestimate the first chart. The final line has stabilized at a new equilibrium that is about double the pre-Ukraine war level, with disastrous effects for European competitiveness. If we reset again at another even higher level, this is going to be very bad for Europe.

2 Likes

I don’t know anything about the market (which is why I’m just a “buy and hold” ETF investor), but people often say “the market has already priced that in”. So why not in this case?

Hhm, true.

The market should have priced that in already.

There’s still quite a bit of uncertainty, the market can be pulling in several direction at the same time.

I mean sure, but the market definitely knows about where ships are and if the deliveries are stopping soon.

The uncertainty is about how long this situation lasts. The market will not be surprised if there are less LNG shipments in a week.

1 Like

Fwiw, to support, someone created the

Wall Street “TACO Stress Index” to Predict Policy Pivot

1 Like

You are right! ![]()

They do say that, but in my experience, they don’t really think about what this statement means. What has the market priced in? What are the implications of this pricing in? Brent has jumped up and down, what was the market pricing in? When did it price it in? Why wasn’t it priced in beforehand?

Be careful. It is too easy for “The market should have priced that in already.” to become “The market has correctly priced that in already and so I will turn off my brain and not employ any critical thinking.”

Instead, ask yourself what has the market priced in, how has it priced it in, does that make sense. Even if the market is absolutely correct in its pricing, it doesn’t have a crystal ball, and so mathematically speaking, the pricing is at best the calculation of the expected value, achieved by integrating all possible outcomes weighted by their respective probabilities. In reality, the probabilities have to collapse onto actual distinct outcomes.

And people say this based on the “efficient market hypothesis” which absolutely does not apply in real life. I’ve seem multiple examples of the market not pricing in things and I’ve been able to make money from these mis-pricings.

2 Likes

I might finally cash out the hefty cost of a heat pump, instead of filling the oil tank this year

4 Likes

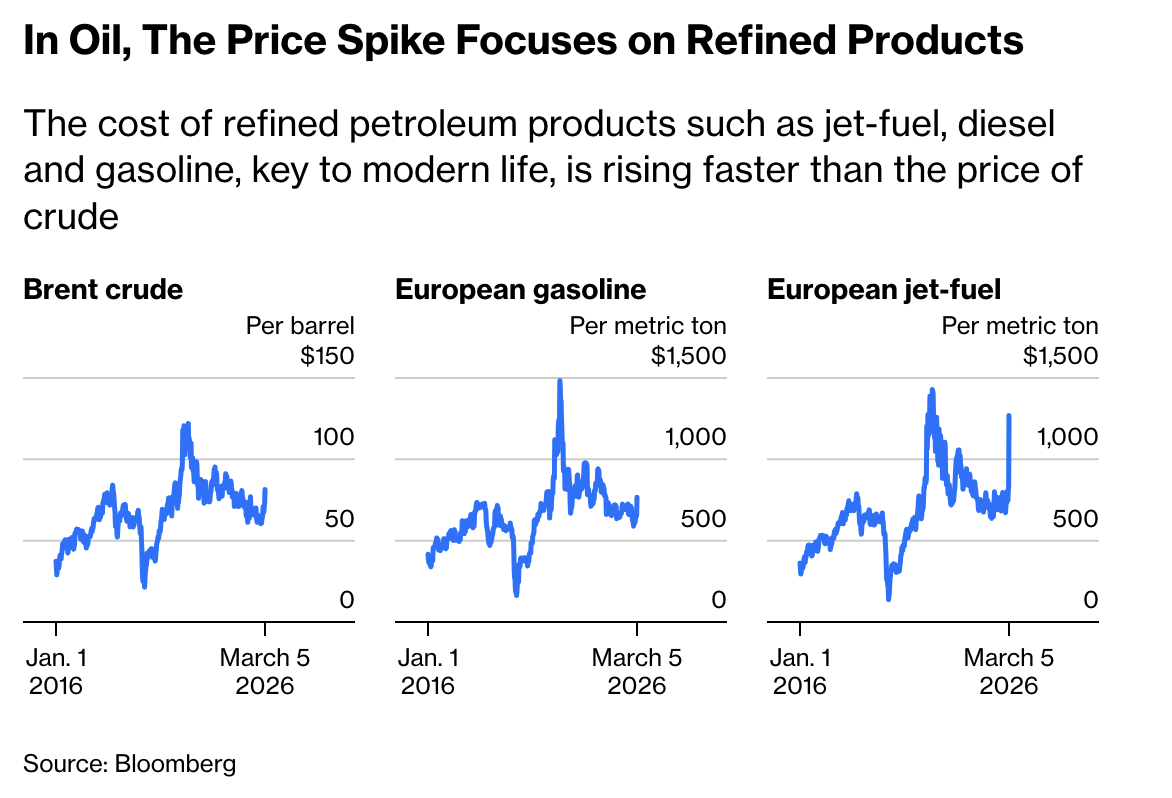

To be honest: I don’t understand the whole situation.

Only 20% of the world’s oil passes through the canal, that’s what was said in some SRG radio report. And most of it goes to Asia. Let’s assume 10% goes to Europe (I’ve no idea how much actually goes here, Perpexity says 5-7%). Let’s assume we can save 2% of that 10%, or that we’re already doing so automatically, because oil costs more and we’re therefore using less. That leaves 8% missing for europe. I mean, it’s a fact that oil costs more. And if we assume that the markets are efficient, then there is a valid reason for the oil price. And yes, high oil prices in Asia affect us indirectly as well. But I still find it absolutely baffling that we’re making such a huge fuss over a few per cent less oil and that this has such a significant impact on the price.

It’s clear that oil is getting more expensive, but by that much?

I know that was kind of bar talk level, but I honestly still don’t quite get it. And yes it also just show once again how little I know about it. But to answer your question:

Covid felt real to me. It was right here. It had a direct impact. The TV news read out the death tolls every day. Entire companies ground to a halt. Aaround the world and in my own country. The rise in oil prices, on the other hand, doesn’t affect me directly. At some point, food will probably get more expensive. And utility bills too. But that’s just “at some point”. Perhaps I’m being naive, but I would never compare it to Covid. I don’t see the the same impact here as with Covid.

Hopefully, when it comes to deaths, it will not surpass covid (a single nuke on Tehran would be enough). But leaving aside military deaths, the deaths due to impact of food and economy could be quite substantial too.

At the start of Covid, some people said it was an over-reaction and it was just the flu and it would all blow over. It turned out much worse.

We are at the start with Iran. Hopefully, it will just all blow over, but it has the potential to escalate all the way to nuclear war. While deaths might be limited to the region (and so impact us less directly). There’s also the economic impact. While it is too uncertain to say how things could be, it would not surprise me if it is worse than covid.

Actually I think this is unironically the best way to think about it, if you believe in an efficient market and are a passive investor. Which I certainly subscribe to, while still persuing other statsitically sound risk premia.

I think it‘s hubris to think one knows for certain more than the market (at least on the level we are playing here).

The current market price is the best guess the market has about the fair value of something.

It prices in uncertainty, as we have seen. And of course it will move if either this resolves or it goes on.

There are many that are long and many that are short. Lots of experts with PHDs and whatnot on both sides.

The market not pricing something correctly can only be said in hindsight, or when information is missing.

The efficient market hypothesis was never about saying the market is this infallible pricing machine.

And it absolutely does apply in real life.

2 Likes

As usual bad things will happen to everyone except the USA because US doesn’t import much energy products. The people in US might pay higher prices but they will still get all their needs met in terms of volume

I believe Europe and Asia will suffer the most with any further escalation and unfortunately for them they wouldn’t be able to tell the initiator of the war to stop. Because let’s face it who can tell US to stop and how can anyone stop US

I believe Europe and Asian stocks will suffer very badly because economy need energy , fertilisers etc to function

2 Likes

Exactly how I think about it as well.

Is the market perfectly efficient? Absolutely not, but it is quite close to. And Hedgefunds etc. are basically working all day and night to identify the leftover inefficiencies, exploiting them and closing them with that.

1 Like

The core assumptions of the Efficient Market Hypothesis are:

- Rationality and Profit Maximization: Investors are considered fully rational and aim to maximize profits based on available information, minimizing emotional biases.

- Full Information Reflection: Asset prices are assumed to incorporate all relevant, available information instantaneously.

- Costless and Instant Information: Information is free and becomes available to all market participants at the same time, preventing anyone from having an unfair advantage.

- No Transaction Costs or Taxes: The theory assumes there are no costs associated with buying or selling assets, and no taxes that could create market distortions.

- Large Number of Participants: The market consists of many competitive participants who, through their trading, correct any temporary price inefficiencies (arbitrage).

- Independent Decision Making: Investors act independently, and their collective actions cause prices to follow a random walk, meaning future price changes are unpredictable.

Let’s take these in turn:

- Rationality and Profit Maximization: Exhibit A: r/WallStreetBets

- Full Information Reflection: Physically impossible

- Costless and Instant Information: Obviously not true and see also Polymarket

- No Transaction Costs or Taxes: ha ha ha ha ha

- Large Number of Participants: Not true for specific markets

- Independent Decision Making: Observe human behaviour.

Forget whether EMH is true or not, even if we accept it as true, we can see that the markets that we are trying to apply it to in the real world hardly meet any of the assumptions for it to apply, let alone all of them.

3 Likes

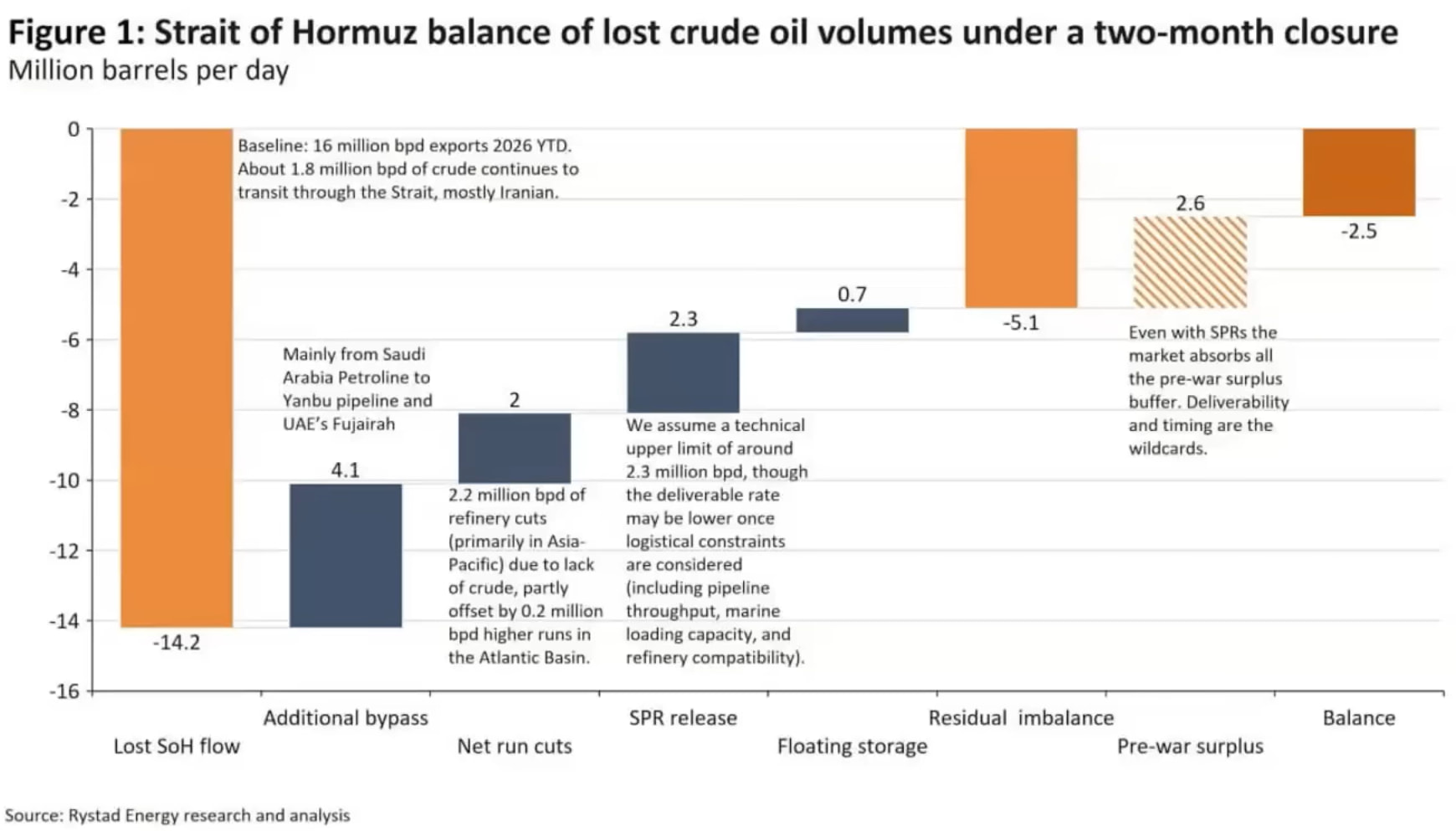

The headline loss is mitigated by a lot off stuff. If Houthis block Red Sea then this makes things worse.

Oil demand is fairly inelastic, we saw in the extremes of covid a 20 mb/d drop in demand send oil prices negative and that was with the whole world shutting down.

If SPRs run out and Red Sea bypass is stopped, we are talking about close to covid levels of energy austerity being imposed, only this time focussed on Europe and Asia as the main energy deficient importers, so even if the headline numbers are smaller than covid, the impact on Europe/Asia might actually be greater.

We’ll see demand destruction help keep a lid on prices, but the demand destruction itself will have its own negative impacts and knock-on effects.

Example here, even with current prices, half of Dutch fishing fleet is now idle due to high price of diesel.

1 Like

6 posts were split to a new topic: Save money on heat pumps: DIY