Rental real estate. Of course, it is not easy to find a good opportunity…

Inflation Protected Bonds: good, but it would be nice to have positive yields as well ![]() .

.

Are you guys preapring for a change in the interest rate scenario?

Have you seen Burry’s strategy buying PUTS for the Long Term Treasury Bond / add more FB and GOOGL in his portfolio? Shall we hedge buying Cooper/Silver/Gold?

WHat’s your view in the topic?

Thanks

Regarding interest rates, the tightening sequence that the Fed followed last time (2014-2018) was to taper (reduce progressively to zero) bond buying first, and after that, to begin to raise rates. Perhaps there is a reason of doing it in that order.

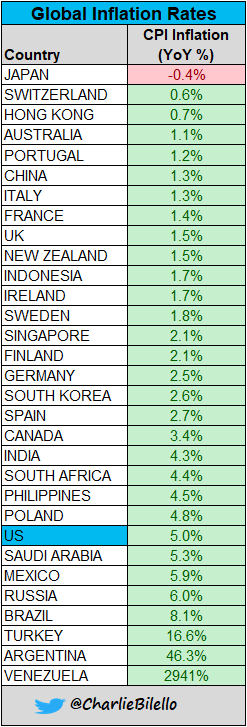

The big question is: is it purely a post-COVID temporary bump (a), or is a permanent >>2% consumer price inflation cycle in the works (b)?

Clearly one should prepare some hedge in case of scenario (b)…

An issue with derivatives is the timing.

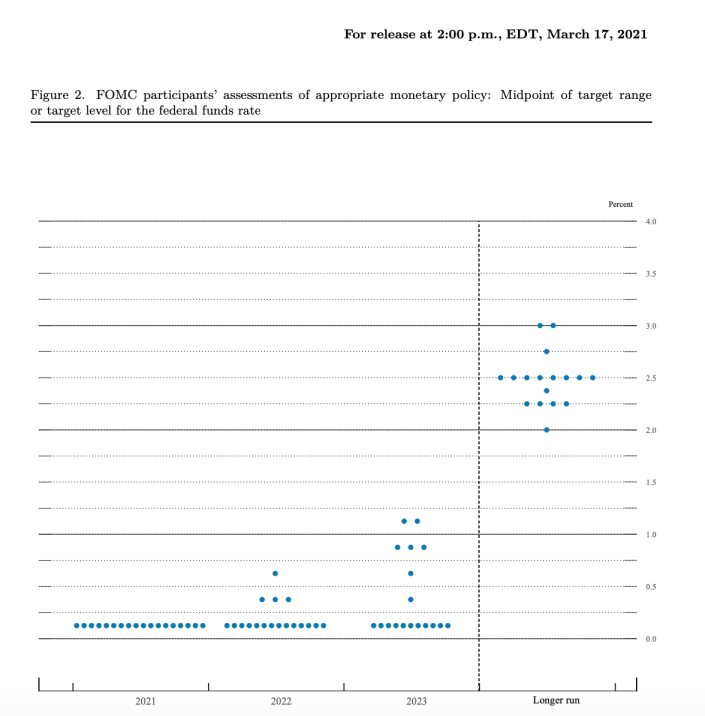

Currently the Fed (median opinion) doesn’t prepare any hike before 2024:

…and today: Producer Price Index +6.6% (but it’s just a one-time, transitory bump).

1 Like

The FOMC meeting concludes tomorrow and may or may not change that. We will get a statement tomorrow (but the detailed meeting Minutes will not be released before Mid-July)…

2 Likes

Speaking of a change in the FED interest rate, I don’t see how this would affect us enough to warrant specific preparations, unless one invests in US bonds or Real Estate (why would we do it, though?). Stocks price would probably be affected somewhat but if we consider we are buying sound businesses, their inherent value shouldn’t vary too much because of that. If we consider that “nobody knows nothing” and are buying the haystack, then nobody still knows nothing and there’s no reason whatsoever to adapt our approach in any way.

Speaking of changes in the SNB interest rates, I don’t see it coming anytime soon: inflation is still very low in Switzerland, we haven’t printed much money that I know of and the SNB should still try to peg the CHF to the Euro in the near future, which I don’t see loosing that much value.

You can see the effect of significantly higher interest rates (2.5%) on stocks, end of 2018: a 20% decline in the S&P 500. Then the Fed panicked and reversed the rate hike…

Then, you’ve definitely missed something…

…but the ECB tries not to deviate the Euro too much from the USD and prints like crazy, too…

So basically, if the US is hit by CPI inflation (more than their normal 2%), we will see it relatively soon on this side of the Atlantic.

1 Like

2 Likes

JPMorgan seems to be sitting on quite the sum in the hope that the Fed is forced to hike interest rates:

Jamie Dimon says JPMorgan is sitting on about $500 billion in cash, waiting to invest in higher rates - MarketWatch

1 Like

This only applies to the “money printed” part of Wolverine’s statement. And most of the increase in M+ happened quite far in the past with little effect on inflation.

1 Like

On consumer price inflation, so far, yes - perhaps rather on real estate prices, or other asset prices?..

Anyway the money did not disappear, even though it was printed “far in the past”. It is just mostly sleeping.

1 Like

On the short term? Sure, people would sell stocks to buy bonds. The thing is, if one believes that nobody knows nothing, then one would ride the wave on an asset allocation that can endure it. And if one thinks they know something, then they either have bought their stocks at prices that would hold their value through the changes provoked by a raise of rates or have a strategy in motion to try and time it.

So, making preparations now? If we think we know what we’re doing, then yes, sure, doing what we know we should be doing is what we should be doing. If we think that knowing that we don’t know how to adapt to such an event is the only thing of value we know, markets movements wise, then we should just keep doing what we’re always doing: being prepared for the best and the worst, since both can happen anytime, without warning.

I’ll admit to not being a monetary policies specialist and being way out of my league here but seeing the efforts the SNB has made to try and keep the CHF from appreciating and the dollar loosing value making the CHF yet a stronger refuge, I don’t see that “relatively soon” happening in 2021. Not saying it won’t happen and I’d definitely welcome a raise of rates normalizing our situation a bit. That I’ve already put my hopes high and ended up disappointed a few times in regards to a raise of rates may explain my pessimistic view of the situation on that front, so I may very well be blind to some domestic inflation facts that may be staring me right on the nose.

Yup, the question is when and why would it wake up if it hasn’t so far? Covid related helicopter money in the US is waking up now because it had few ways to express itself earlier but we haven’t really had helicopter money around here, so our sleeping money is older than that. As long as people who consume everyday goods (low income to middle class people) don’t get a large amount of money thrown their way (and salaries aren’t really climbing for middle class jobs as far as I know), then it will stay concentrated in assets like real estate, stocks, cryptos, gold and collectibles. Those have chances to hurt future returns for investors but shouldn’t funnel inflation as measured by the Swiss CPI.

1 Like

There’s a new podcast interview with Aymo Brunetti (former head of policy at SECO and head of economics at University of Bern) where they discuss this topic [in german]:

tldl:

He believes that inflation is mostly undesirable and has no issue with very low inflation in the long-run.

According to him there is a trade off between the SNB increasing rates leading to lower inflation expectation (and thus inflation) and it leading to a downwards turn in the stock market…

He is urging the SNB to increase interest rates as soon as possible.

3 Likes

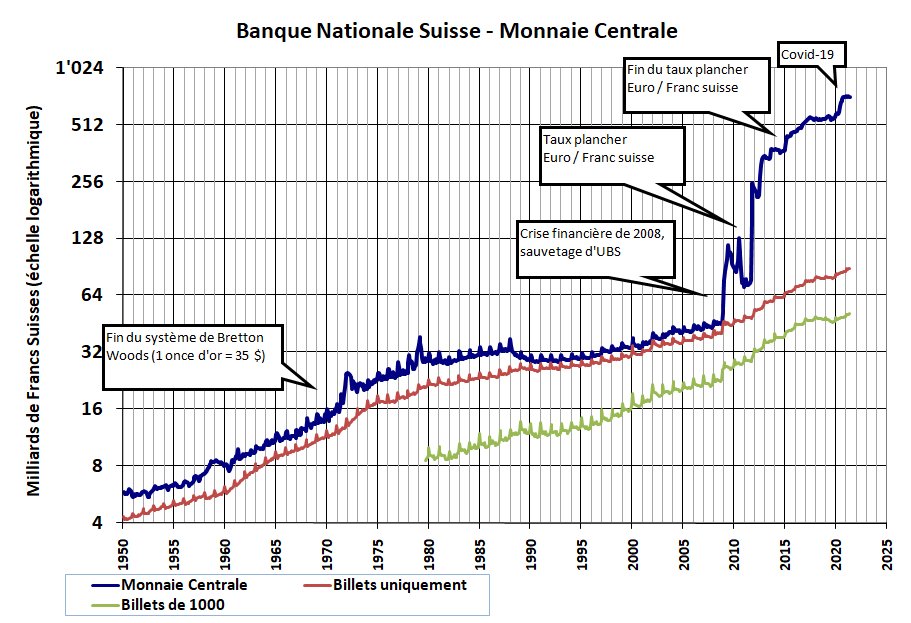

People are fine hoarding CHFs (this includes ~50 billion stored as 1000CHF banknotes!): political stability, low government debt, and flat CPI. But, if we enter a phase with, say, 2%+ inflation for a year or more and overnight rates still at -0.75%, some people (and then their neighbours and friends) may reconsider this strategy. Just a possibility…

1 Like

Super interesting! It’s very unusual to hear an economist who is not in the inflation-targeting groupthink crowd, and still has a teaching position.

Now, the SNB (*) won’t have the guts (NB: I wouldn’t either) to raise rates before the ECB, and an ECB official has said that it won’t tighten (via less QE or via rates) before the Fed. And both the ECB and the Fed cannot really tighten, so all they can is to hope the inflation is going away from itself. But when you hear from Pr Brunetti (~ -4min in the podcast) that from experience, with 3% - 4% you have good chances to have the start of a price-wage inflation spiral, then well… at least, fasten belts!

__

(*) Recent quote from SNB’s Thomas Jordan: “It would be wrong to signal to the world now that the SNB will be the first central bank to envisage a restrictive policy.”

Nice Article on protecting against inflation in FT, no paywall

Suggestions in the article:

Buy good quality equities

Residential property prices are frothy but not a good time to be out of the housing market

Commercial property not good

Avoid bonds

Makes sense to have a small stake in gold or commodities

5 Likes

Thanks Barto for posting this FT article. It is an interesting read and makes me think of evaluating a 5% tilt of my portfolio in some form of ETF which can provide some at least partial protection against inflation.

In the past I found out that TIPS could do this job and if I would go for TIPS I would definitely go for Vanguard Short-Term Inflation-Protected Securities ETF (VTIP) which has a very low TER and seems pretty secure with low volatility. In terms of TIPS there is not so much choice of ETF anyway so that makes it quite easy.

Then on the other hand you have more more commodities ETFs to chose from which have for most of them high TER in the range of >0.5% with some volatility and much more risks. So I am not sure why would one go for commodities ETF…

Having a look on ETFdb.com for (broad) diversified commodities gives 22 ETFs. My rationale here would be to find a sort of VT ETF (as broad as possible) but for commodities in order at least to diversify as much as possible among the commodity categories (e.g. agriculture, energy, etc) and therefore lower idiosyncratic risk.

For the fun of it here are a few potential ETF candidates which seem to me as “interesting”:

- WisdomTree Enhanced Commodity Strategy Fund (GCC)

- Invesco Optimum Yield Diversified Commodity Strategy No K-1 ETF (PDBC)

- iShares U.S. ETF Trust iShares GSCI Commodity Dynamic Roll Strategy ETF (COMT)

I would tend more towards GCC from WisdomTree because it has less percentage of energy commodities and not too extreme TER at 0.55% but its AUM is quite small at 140 mio$.

Anyone of you have any TIPS or commodities ETF in their portfolio? and if yes which one?

1 Like

Regarding TIPS, a large holder is… the Federal Reserve. Uh-oh. Read for instance:

“Digest that for a moment: the Fed bought over $175 billion of TIPS from March 13, 2020 to the end of February, 2021, whereas only $150 billion or so of new TIPs were issued (Source: Bloomberg, Federal Reserve). In percentage terms, the holdings of the Fed have gone from less than 10% over the same period to over 20%.”

It always amuses me that most of the people giving out investment advice in newspapers are such successful investors that they have to work at newspapers writing newspaper articles.

3 Likes