Historically higher inflation was generally a killer for growth stocks (e.g. tech stocks), but it wasn’t affecting that much value stocks. Very high inflation is a killer for everything except gold (and perhaps bitcoin) - as the rising costs of inputs, and need to constantly pass higher costs on clients, and the constant push of the employees for higher wages ruins the macroeconomic stability of the economy - look at any scenario of hyperinflation, like Poland in late 80s, Weimar Republic in 20s, or modern Zimbabwe. A sudden rise in inflation is also a big problem for companies because they need to instantly pay higher costs for inputs, but they aren’t prepared for passing these costs on to clients - this obviously takes time and can’t be done overnight. But I doubt we will have really bad inflation. My view is that it will be elevated for some years and this should boost value stocks and handicap growth stocks. In any case, this should be anticipated by investors and thus priced in the market. Probably we will see lower real returns in the coming years.

High inflation sucks especially for the poor who don’t have stock market investments. They usually are in the worst position to negotiate a raise (to catch up with rising prices), and their savings are getting crashed (especially with the zero interest rates on the bank deposits and low returns on government bonds). IMHO, high inflation in combination with low interest rates is a machine to exuberate wealth inequalities.

Another practical impact of inflation is that it will cause USD worth less in CHF. A practical recent example is PLN (Polish zlotys) which was about 4 PLN for 1 CHF a few months ago, but now after a few months of elevated inflation 1 CHF costs 4.5 PLN. I think in the long term similar effect will be with USD, so our investments will be worth less in CHFs. Bad news for those who plan to retire in Switzerland with USD-denominated dividends and capital gains.

PS. I elaborated a bit on inflation and money supply here:

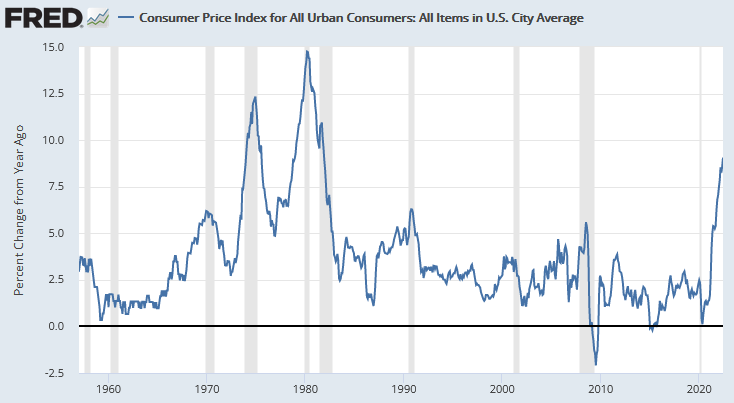

Why use CPI-W and not CPI-U (at 6.8% YoY)? That’s less than 1/3rd of the total population. Also, why is inflation hitting wage earners more than, say, self-employed, retired or unemployed people?

It is per se interesting. But for various reasons it is especially interesting IMHO: unions, or workers who are switching jobs or negociating wage hikes, are likely to monitor that metric rather than CPI-U. CPI-W is used for automatic increases in social benefits. And FIRE candidates are often urban wage earners, aren’t they?

Here a good summary in French of inflation and FX situation in Switzerland on RTS (7 min video, also a shortened text summary that can be translated)

My own takeaways:

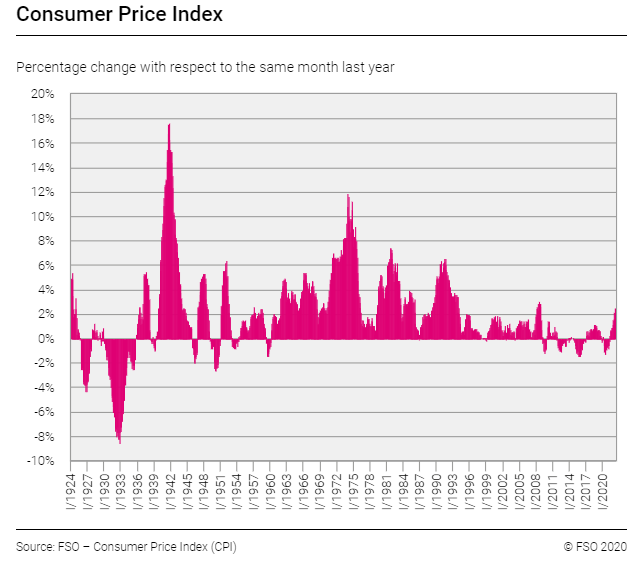

Versus other countries inflation today is moderate in CH at 1.2% thanks to the strong CHF. Higher inflation in other countries will put further upwards pressure on CHF FX rate

Inflation is somewhat a self-fulfilling prophecy. What happens in CH will depend a lot on salary negotiations

There is potential upwards pressure on salaries because many employers are looking to shorten supply chains so cannot negotiate with unions with the same threat of off-shoring as they did in the past

Regarding 1 it depends how far the SNB can (and wants to) let the CHF appreciate given its enormous FX reserves (around 1 trillion CHF currently). Theoretically its own capital could become negative but… hum… Do they want to be in such a situation?

Well, it seems like inflation is finally hitting Switzerland. We’re just at about 3% year on year but we’ve got a massive 0.65% increase month over month, which annualized would be 8%. Without surprise, wood, oil based energy, transportation, used cars, some foods and clothing (women get hit much harder than men, here) are the main culprits.

If you’re eating rice, pizza, pork, sausages, fruits, potatoes and preserved vegetables, you’re fine. While coffee gets hit pretty hard, tea drinkers go mostly unscathed too. If you want to buy a TV or a console, now’s a good time for it. Also, consumer medical costs are going down…

Anecdote: Out of curiosity I completed a Credit Suisse online mortgage calculator last week. It proposed a 12 year fixed rate 2.9%. Much higher than the rates we were talking about 6 months ago

I tried to replicate it today and it gave me 3.05%

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.