I am not sure how recent this news is, but I just saw that IKEA has a credit card. They offer 1% “cashback” that is earned everywhere, but can only be spent in IKEA. Since the other cashback card is an American Express, it might make sense to use the IKEA card whenever Amex is not accepted? They also offer a free additional card, which is great for couples.

Looks like a nice deal. The operator is Cembra, which is the same as the Cumulus card. Only there you get 1 “point” for every 3 CHF spent outside of Migros. Here you get 1 point for every 1 CHF spent outside of IKEA. And if these points are valid at least a year from the date of issue, then it should not be a problem to find something valuable in IKEA at least once a year.

What about the “free additional card”? The card is anyway free, so what’s the advantage here? That you can collect points from both cards in a single account?

I don’t see the advantage of a single bill. Cembra is anyway not in e-Bill. It would be good to have a credit card that you can automatically pay off with e-Bill.

I don’t think it makes sense, waste of time. I thought you would only use this card. After all, cashback is just a psychological trick, a marketing gimmick, to keep you in their loop. But for someone who was looking for their first card, this looks like a good option.

These kind of micro-optimizations are misguided, IMO. 1% cashback is better than 0%, but 0.33 vs 0.20, forget about it. You should not have to think twice how you spend your money and time to manage it should also be minimal. Migros sends me these Rabatt coupons, I throw it right into the trash, I’ll buy the stuff when I need it, not when there’s a 5% reduction in price.

I think you misinterpret how it works. If you spend, say, 5’000 CHF per month outside of IKEA, you will spend 60’000 per year, or 600’000 in 10 years. For that you will get 1% cashback, that is 6’000 CHF to spend in IKEA. So even with such high spending, there would for sure be enough furniture that you could buy over 10 years.

I think what makes this card stand out aren’t the rewards, but the complimentary travel insurance and purchase protection perks. It’s rare to find those kinds of benefits on a no-annual-fee credit card.

I would agree with Cortana that the psychology behind reward credit cards is to incentivize you to spend more. It takes a very disciplined person to not get caught in that trap. I pretty much only use credit cards for travel bookings, so complimentary insurance saves me more money than rewards.

For anyone interested, here’s a review of the Ikea Family credit card:

Those are the same you have with the Cumulus CC, right?

I think this card is not worth the hassle. I don’t buy that much stuff at Ikea, especially because some of the small stuff you can buy there is crap. Ikea is all about making cheap products, sometimes too cheap (pans, batteries on top of my mind).

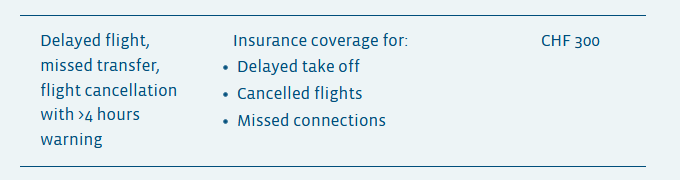

No. The Cumulus card only comes with complimentary emergency medical evacuation/repatriation insurance. With the Ikea card you get compensation for extra costs resulting from trip interruptions/cancellations, which is the one travel insurance coverage I have ever actually used (and more than once). Also, you get purchase protection. So the Ikea card is really the first Swiss no-annual-fee credit card I’ve seen with really useful insurance benefits. But with regards to the rewards, I agree that cash back is much more useful. I pretty much only buy household and furniture items second-hand, so I very rarely spend at Ikea.

I can’t find any info on their website though. I just found the text "Attractive supplementary insurance (find out more at ikea.ch/creditcard) " with an useless link.

If it’s true, I’ll probably cancel my cumulus card and use this only for flights. I don’t buy much at Ikea though.

Gotta compare the Ts&Cs. It’s important to note that the Ikea credit card does not have trip cancellation/interruption insurance. If you miss a trip (and the airline is not at fault), you won’t get your bookings reimbursed. Interestingly though, I’ve never been in that situation - it was always the airline at fault so I could never claim on the trip cancellation insurance. But the coverage for unexpected costs (which you get with the Ikea card) always came in handy in those situations for the expenses that weren’t covered by the airlines.

I can relate to the Ikea points being kind of useless, even at 1% of spending. The Cumulus points are much more useful (I use them to pay for municipal garbage bags). My ideal would be the Amex Cashback credit card with these insurances.

One card which I can highly recommend if you do a lot of traveling is the Libertycard Plus. I go it with a special promtion so paid half price permanently. It has pretty solid travel insurance perks (including trip interruption/cancellation), bicycle insurance and a car rental collision damage waiver, and the insurance applies even if you don’t use the card to pay for bookings. Just those benefits saved me a couple hundred francs per year. Plus around 1.6% rewards for public transportation, gas, and travel bookings redeemable for gas stations, SBB and SWISS vouchers, among others. But there is the annual fee.

This doesn’t really help on my previous issue with a flight.

Also I’m not 100% sure what the card is covering since 100% of the flights originating or arriving in EU/Switzerland are equally covered by the airline insurance. Not sure for flights with middle stop (arab airlines) https://www.cancelled.ch/en/passenger-rights/

Can you give us some real-world examples of what they paid, as you seem to have claimed a few times? I’ve always looked at these free insurances included with a (free) credit card as “we’ll reimburse you something if there is a volcano, hurricane & terrorist attack all at the same time, but only by hitherto unknown terrorist organisations & volcanoes, else all claims are void.”

That would be due to a medical emergency or funeral of close relative for example. That is covered by various 'Annulationsversicherungen" costing Fr 100-200 p.a.

No “free credit card” would offer that, surely?

Recent examples of when I used the coverage for unexpected costs: I flew to South Africa once in 2018 and again in 2019. Both times the flights (one with Emirates and once with Swiss) were cancelled due to technical problems, and we (my fairly large family and I) were rebooked for flights the next day. The airlines put us up at hotels until new flights were arranged, but aside for some stale sandwiches and vouchers we couldn’t redeem, that was about it. In both cases I got our restaurant expenses reimbursed. That’s an example of how the coverage for unexpected expenses resulting from trip delays or cancellations saves you money. I actually have found this to be the most useful travel insurance, so I’m impressed to see it on a free credit card.

Yep. I haven’t seen annulationsversicherung (trip cancellation/interruption insurance) on a no-annual-fee credit card (yet). But in the time I’ve been in Switzerland I’ve seen free credit cards multiply, and their rewards go from a maximum of 0.3% to 1%, and insurance benefits go from emergency medical to the multiple benefits we now have with the Ikea card, so I keep being surprised. I guess use has gone up enough that the merchant fees being raked in make it worth throwing in ever more bait.

Trip cancellation/interruption insurance never covers cancellations/delays which are the fault of airlines. The airline is liable to cover those. You can find more info here. But the coverage for unexpected expenses does apply in this case, so expenses above the rudimentary provisions from airlines are covered (up to the insurance limits).

Trip cancellation/interruption insurance reimburses travel booking when you cannot make the flight (because of unexpected illness, your car breaking down on the way to the airport, etc.). In all my years of travelling, I only experienced this once (when the railway bridge from Sweden to Copenhagen Airport was blocked by a broken-down train). Otherwise, the 5 or so cancellations I experienced were always the airline’s fault. Mostly technical problems (so unavoidable).

hi Daniel, thanks for sharing your knowledge on this. Could I ask if you already looked at the following: Before C19 the scenario I started looking into how to insure one of our kids getting a bad fever whilst being away on holiday and having to book a different flight back. Does your Libertyplus card cover this and I wonder if it is better to take this card for 150CHF per year vs. buying separate insurance?

One of the grudges I hold with these credit card insurances is that they make it overly complicated to file a claim. Usually hand-filling a PDF document and then sending it per post or fax to some number. (well Viseca inofficially accepts them over email too). There should be a service that helps filing claims more easily @ma0

Especially for the best price guarantee it should be possible to have a website that tracks prices for the next 14 days (or whatever the best price duration is) and then automatically files a claim if a lower price was found…

I know what you mean. Citibank introduced tracking for price protection in the US some years back, with alerts if a lower price is found.

The fact is that it isn’t in an insurance provider’s best interest to make filing claims too easy. In fact, one reason credit cards, for example, can afford to offer complimentary insurance is that in practice, only a handful of cardholders ever claim on the insurances. If all insured persons would claim every time they were entitled to, the premiums would be much higher to match the higher risk. So actually, it works out pretty nicely for the frugal-minded few as it is right now.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.