Is there any benefit of MSCI ACWI Quality vs MSCI ACWI from expected return perspective?

It sounds like stock picking based on some made up rules by MSCI & a very high concentration of US stocks (77%).

Is there any benefit of MSCI ACWI Quality vs MSCI ACWI from expected return perspective?

It sounds like stock picking based on some made up rules by MSCI & a very high concentration of US stocks (77%).

No comments on that. The post was for informational purposes only. I don’t invest in MSCI Quality myself (neither in 3a nor outside)

Here’s the latest holdings (per Bloomberg) of the VT (MSCI ACWI proxy) and the IWQU (closest public proxy to MSCI ACWI Quality? It omits EM countries, though).

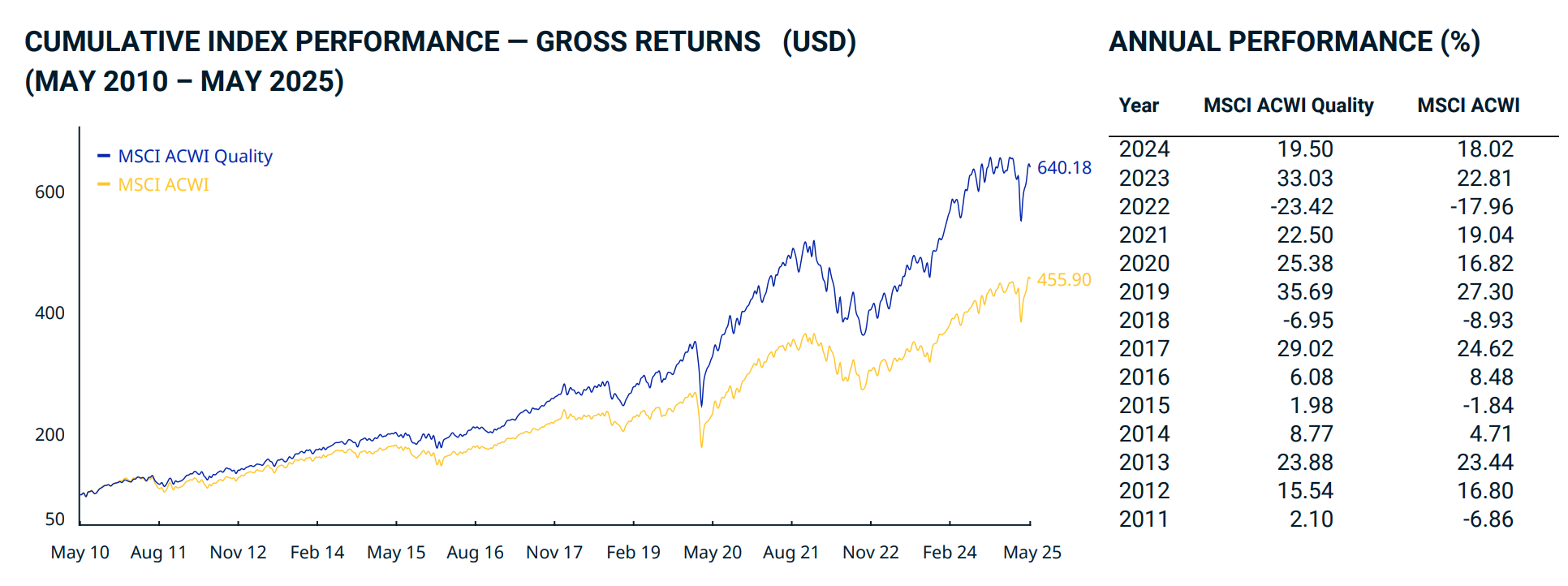

According to the index provider the quality index outperforms the ACWI index.

Edit: one notable difference I spotted after glancing over the two tables: the quality index does not include TSLA$ and it’s at weight #9 in the AWCI with .9%.

Personally, I believe this is great stockpicking by the quality committee, but YMMV, of course.

Indeed this is stock picking under disguise of index investing

Having overweight to US stocks has helped outperformance but I am not sure if this is luck or logic

When they outperform it’s clearly logic!

And when they underperform – like in 2022 – it’s … well, bad luck?

![]()

Well played, Supervisor Goofy.

Watch your back.

![]()

This could be said for any factor investing: you select a factor, you select (pick) stocks exhibiting that factor, you make an index, you make an ETF tracking that index ![]()

Yes

I think - The factors are nothing but quantification of what happened in past. It’s basically people trying to explain market results

There was this very smart person Rational reminder once who said that most factors are very difficult to make money from because everyone knows about them and things get priced in.

I am curious though if ETFs tracking those factors actually started before the factors started outperforming or after.

Tomorrow someone can say there is a factor called Geography. And being an American company is a factor for outperformance . Then plot the chart of S&P 500 versus rest of the world and viola.

I checked the performance of Ishares MSCI world vs Ishares MSCI world quality. Outperformance means factor outperformed. All numbers are cumulative and not annualised

Source -: justetf

10 years -: outperformance of 1.3%

5 years -: underperformance by 9%

3 years -: underperformance by 2%

1 yr -: underperformance by 6.7%

That’s the crux about why, in my opinion, economics and finance are no more scientific than reading tea leaves and phrenology is. Science understands the past to predict and impact the future - like building a space shuttle or engineering a gene - finance barely manages to clutch some straws which kinda fit, but not quite, and doesn’t make any assumptions for the future.

you are not doing an apple to apple comparison here.

the ETF you selected is a sector neutral quality ETF and not the one shared earlier in the thread. A pure world quality ETF did not exist for retail investors till about Dec 2024 when this one was launched so there is very little data for it to compare with. There is data provided directly by MSCI if you would like to use that.

Again, factor investing is not for everyone and for me personally I keep a small portion of my portfolio in value and quality factors to provide a marginally better long term risk adjusted returns and protect my overall portfolio against a drawdown respectively. There is a lot of literature around it but again analyzing past trends can never ben an indication of the future.

Big tech has performed exceptionally over the past 12 years so any portfolio underweighting this would lag during this time frame as well.

Yes I used the ETF I could find for quality.

I don’t necessarily have an issue with Quality ETF or factor investing

I just think that this is much more of an active investing than passive. That’s all

It is a rule based investing and these rules are clearly well defined in advance (so yes can be called active investing, like any other when creating an index such as SP500 etc.)

what would be more worry some is if these rules keep changing regularly but at least what I found with MSCI indexes are that these rules are fairly applied (this could be called a mechanical strategy, as discussed in another thread)

Quality is as much stock picking as value, momentum, size etc., no?

Just to mention that these are risk factors “on top” of the market risk. Though the Quality is not exactly part of the Fama-French 5-factor model (it is close to profitability I guess)

The “stock picking” is based on specific criteria that have been thorough studied.

Not exactly the kind of stock picking most “daily traders”/active investors do…

I think if someone says that “this factor” always outperforms and they overweight this set of stocks, then it is an active decision and an assumption that rest of the market is mispricing those specific stocks. Isn’t it?

How can both of the following be true

Not quite sure if you guys are serious.

Sirs, Past performance is no indication of future performance.

This.

Yes, but I don’t understand how this relates to my question if quality factor is just as much an “assumption that rest of the market is mispricing those specific stocks” as the other factors.

I don’t understand what you’re trying to say. I was just asking if investing with quality factor was basically the same active process (“stock picking”) as investing with size factor, momentum factor or value factor.

Sorry . I forgot to say

You are right. It’s indeed the same as other factors like size or value.

Not sure what you consider lack of seriousness. Risk factors / market efficiency etc?

I am not an expert in Factor investing so take my comment with caution ![]()

My understanding is that it is not about “mispricing” but rather taking different type of risk.

Companies that meet the criteria of a factor (lets assume for example the Fama & French 5-factor model) have more systematic Risk than the others.

For this additional risk, investors are expected to be compensated more in the long run.

e.g. small cap companies may not behave well in a crisis vs big cap → higher expected returns

The market is pricing in this independent systematic risk they have.

Now if the factors still persist (now that they are known) is another topic. ![]()

One can argue that waiting for 15 years for a factor to pay is not preferred by all. Tracking error is also a big concern even in institutional investors.