Regardless if we speak about MSCI Quality or MSCI Momentum or NASDAQ 100, what is the reason behind their ability to outperform the market? Is it sustainable? Past performance does not mean future returns. Yesterdays winners might become tomorrow’s losers.

But the crucial question is really, once again: why does the market price these assets below their value, so that even with a couple of passive indicators you can build an index with higher return, without higher risk exposure?

Look at the turnover % of both indexes, Quality has 22% and Momentum has 156%(!!) so as you mention how can this be termed “passive”… For an ETF to be based on these indexes they should have in theory a high TER. Looking at IWQU shows 0.30% TER which is not even high but yes still 4x more than your usual VT.

I wonder why Vangaurd does not have any Momentum/Quality ETF… maybe precisely because it can not be so “passively” managed…

Nevertheless these two indexes are very tempting and @Julianek’s research super interesting to read!

Quality and Momentum are considered smart beta ETFs, not really passive indeed. Some people would also argue that SP500 is not passive, because a committee will select the stocks (like not including Tesla).

In a way, it’s easy to create a smart beta index and backtest it to beat the market. I’m not really convinced about backtests

I stopped believing in all those factors. It’s just artificial. Like looking at 100 years of US stock history and coming to the conclusion: If you bought stocks which name started with A/F/M and left out the others, you would have increased your returns by 3%/year. It’s the AFM-risk premium and should also persist in the future, lol.

The reason we buy VT is because we know everything about the past and don’t know shit about the future (sorry about the expression).

My point is, Quality, Momentum or even NASDAQ 100 are chosen in a non-arbitrary way, which makes them kind of passive. There is a set of rules which determines which company gets included and at which weight. And they seem to constantly beat the market. Then why does the market put such a high price on stock of companies that are known to have trouble and nobody expects them to make a sudden rally?

According to the efficient market theory, when we see a risk premium from investing in quality stocks, we should asks ourselves, what is the extra risk that the investor is taking? To me, it’s weird, because it seems like the quality stocks only have upsides. If investing in quality yields better returns with no increased risk, the prices of these stocks should go up to make this premium disappear. Why does this not happen?

Thank you for noticing this, i had totally missed it. Although it makes my point a bit weaker, I still think that it is remarkable that:

Buffett (arguably one of the greatest investors over the last 60 years) says in his letters since the 70s that the number one criteria to look for is return on capital

40 years later, when we say “Wait a second, what would actually have happened if we had followed his advice”, we end up with a very fine result, even if backtested.

I’ll grant you that. I will rename the topic from “passive” to “index fund”. The approach i am trying to follow here is to ask:

The first step (totally passive) is to say that I do not know anything.

But then, is there a single decision that could dramatically improve results? Thinking from first principle, what drives wealth over the long term? I’d argue that a consistent high return on capital comes pretty close to that.

You only need a database of 10-K filings (or local equivalents) to be able to compute a return on capital, growth rate and financial leverage. The factsheet says that the index is rebalanced every six months based on these criteria.

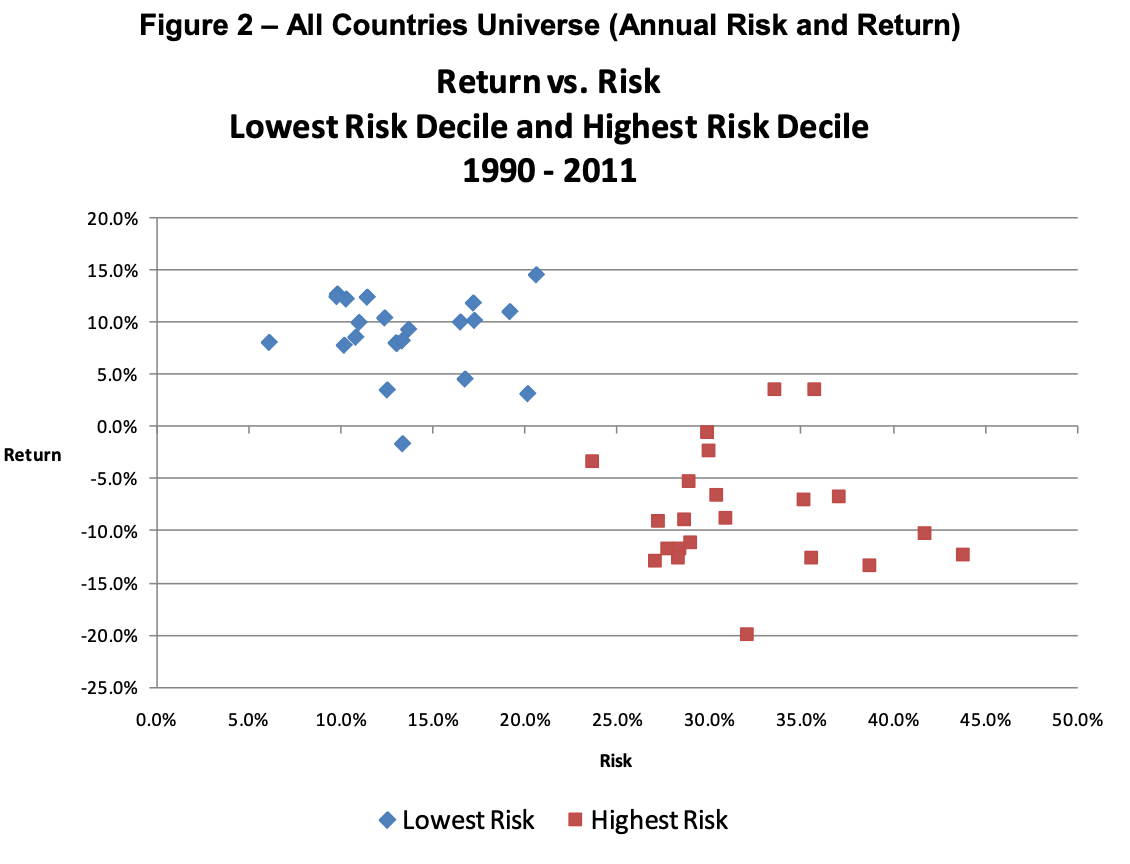

I like Ben Felix but sometimes he should not rely so heavily on modern portfolio theory. MPT works in some cases, and not at all in others. For instance, in this study, Baker and Haugen showed that low-risk stocks (as measured by volatility) consistently over-perform high risk stocks in every developed market.

Someone will try to find a new factor to explain the anomaly and make the French-Fama model consistent, but at some point it is better to ask if you cannot start again on a better basis.

the fact that the human brain works in a logarithmic way and is incapable to grasp exponential growth

But mainly, i think there is a structural issue with how the industry and analysts evaluate stocks. Let me explain.

You might know that the number one valuation method to evaluate a business is the discounted cash flow analysis. Analysts try to forecast the cash flow for the next few years, after which they say that they don’t know what’s going to happen so they assign a GDP growth rate in perpetuity after 5 or 10 years. That is to say, they assume that after 5 or 10 years, the business is going to grow at the same rate than the economy, i.e not a lot. That means that each of the forecasted year will have its discounted cash flow, and after that they will add what we call the Terminal Value, i.e the value of all the cash flows after the period of projection.

The vast majority of analysts will use 5-year or 10-year DCF models to value a company and pay painstaking attention to the assumptions to drive their interim period cash flows. If you do yourself the exercise, you will notice something interesting. Here is the contribution of the terminal value to the appraised value of the firm given different interim growth rates in a 10-year DCF model:

Projection Period Growth Rate

Terminal Value Contribution

5%

73%

10%

78%

15%

82%

20%

85%

25%

87%

30%

89%

In other words, what happens before the 10 years only weights for 11% to 27% of the company. What is 11%-27%? A margin of error. You can get the next 10 years of projections wrong- as long as you know what the company will look like 20 years from now.

This has a lot of implications:

Again, people use 5-year or 10-year DCF models where they model in high growth rates and high rates of return. At the end of the “projection period”, they will plug in a perpetual 2% growth rate to the then “boring” company. What if a company can compound capital at a higher rate than its competitors for longer than that? A junior analyst will get laughed out of the room for creating a 20 or 30-year DCF, so again, unfortunate situation for the junior analyst but an opportunity for investors.

If you follow financial news, you will notice that experts and Wall Street all focus on next quarter EPS expectation. This is all noise and is irrelevant. First, next quarter EPS weight close to nothing in the value of the business. Second, remember that instead of focusing on EPS, you should ask if the profitability of the business has not been impaired.

Now that you know that most of the value of a business lies in what happens after 10 years, next time you see a -30% drawdown like we had in march, if you believe that the business has the balance sheet to survive, you should pounce on the occasion.

This is another topic, but this comes down to the qualitative analysis of the competitive environment of the business and its competitive advantage (i.e “moat”). Maybe at some point i will do another thread on the subject.

Thank you for the post Julianek. This is very helpful as I am considering whether to invest my 2nd pillar currently being transferred to Value Pension vested benefit account in MSCI World Quality or MSCI world

Did you find anything in your research on how they did the backtest - did they go back and apply the quality algorithm fully to 1994 financial statements and then model which stocks it would have bought ? And update the portfolio for every year between 1994 and when the index was created

Yes, you’ve raised this argument once. But is it seriously so bad? I mean, individual investors can be short-sighted, they are mortal. But institutions exist for 100+ years. A fund should look 30 years into the future, because they should still exist and be in the game at that point. You’re saying that most of these companies don’t?

It just seems like such a simple thing to overlook. To think that you could invest into an ETF and get 2-3x returns in 20y horizon is just incredible. If you were a passive investor (in the understanding of betting on one horse and sticking to him), would you seriously go for MSCI Quality in favor of VT? Is this something you would advise to consider for me and other holders of VT? Do you have some links to other FIRE sources where they encourage this approach?

And finally, what’s your take on MSCI Momentum, mentioned by Glina? I like that it includes Tesla & Amazon, but at the same time I don’t think it’s a smart index if it only looks at the price graph, without looking at the fundamentals.

He also says that at least for his estate planning, he wants it in a pure passive fund:

“Well I can tell you I haven’t changed my will and it directs that my widow would have 90% of the funds in index funds,” Buffett said. “I think it’s better advice than people are generally getting from people that are paid a lot to give advice.”

Every factor, every country, every sector will once shine bright in the sun. There is no point in chasing past winners. Reversion to mean will eventually occur.

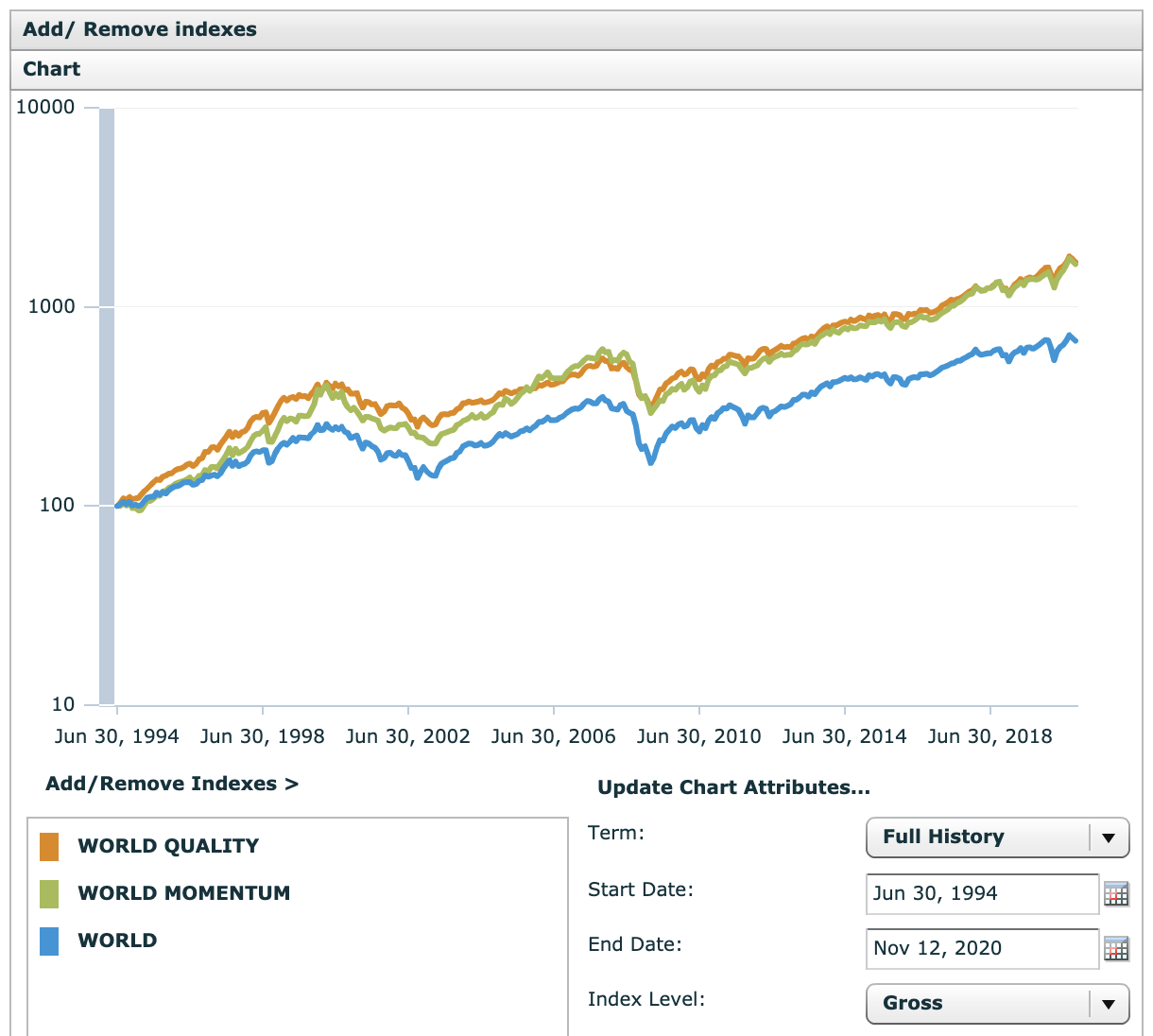

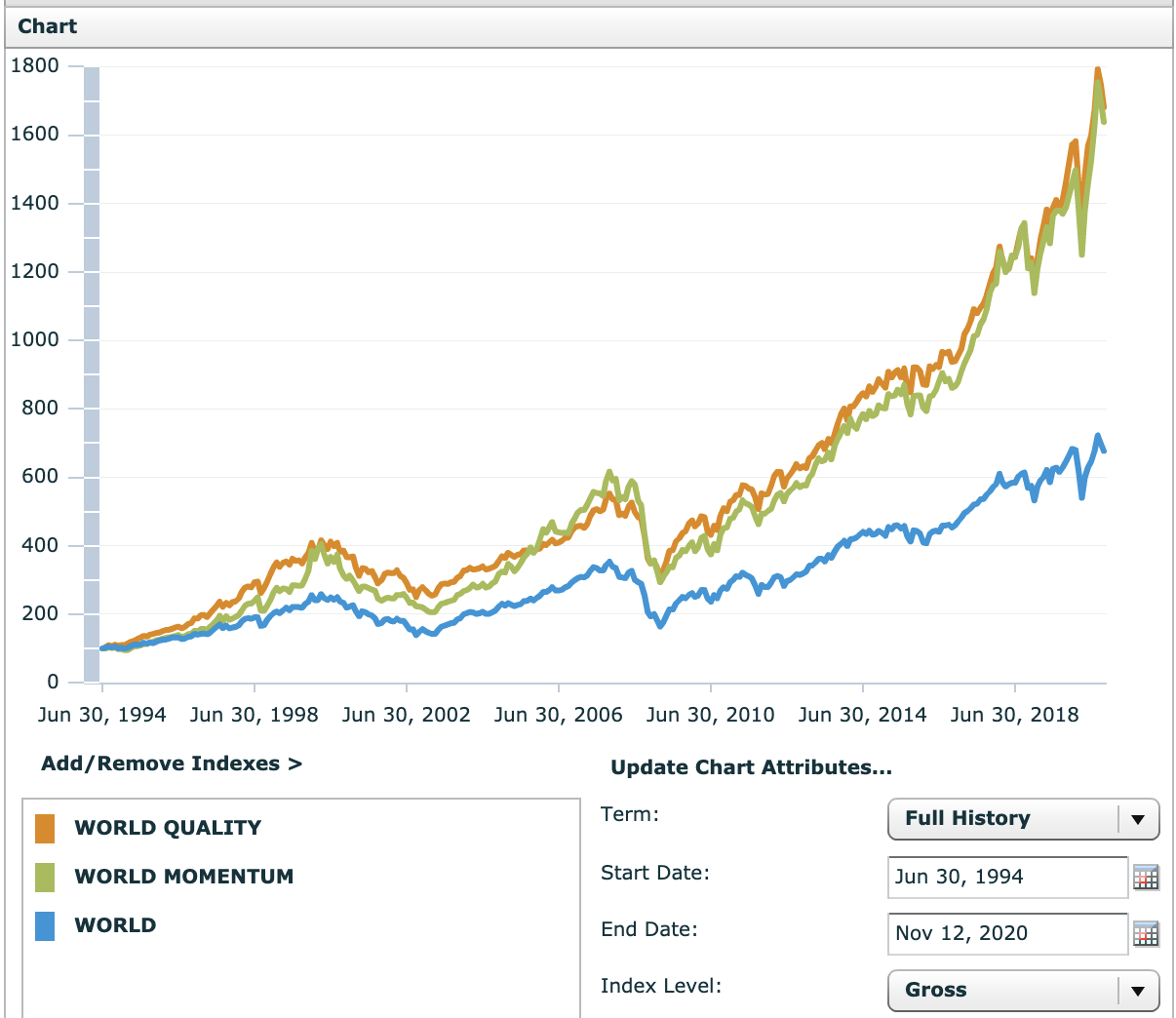

We can see that this seems to hold true for Value vs Growth. Value has been superior for at least 50 years, but recently the gap is very small (see chart).

If the same will happen to Quality & Momentum, time will tell. Right now we only have 25 years of data. (MSCI has price data since 1975, but no point to compare without dividend). But I have to say the advantage is impressive. And it’s funny how Q & M go almost neck and neck.

Mhm… I seem to be quite late to the party here, but…

I happened to settle on the MSCI quality index about 3 and a half months ago as main investments

Though I might not have shared it on the forum back then

But… see the bottom of this post for the caveat.

Beware, it does not.

This is quality factor ETF. It’s a trap that I almost also fell into myself, cause you do have to read the fine print. I’ve even seen an ETF having switched from the Quality index to the Sector Neutral Quality index. I think it was an iShares one, might be this very one (though I’m too lazy to check).

Again, this also does not track the MSCI Quality, but is a sector neutral factor index ETF.

The funny thing is though: Retail ETFs actually tracking that very index seem impossible to find.

You can look it up on JustETF, ETFdb or Yahoo. I haven’t been able to find one.

(I haven’t yet looked into the specifics of the institutional investor ETFs offered by Finpension).

The Amundi ETF, though named “factor” ETF similarly to the iShares and Xtrackers above does track the (non-“sector neutral”) MSCI Europe Quality index, whereas IWQU and XDEQ track the “sector neutral” variants of the indices.

What does sector neutral mean? See MSCI World Sector Neutral Quality Index. Or simply: they keep the sector (IT, Health Care, Financials etc…) weighting the same as in “plain” MSCI world.

Personally I see no point whatsoever in doing so and staying “sector neutral” to the MSCI World. Especially since I’ll be diverging from MSCI World’s weighting of stocks anyway. I’m not convinced either that every sectory is just a “good” as any other. If there’s more “Quality” stocks in one sector (for example the overweighted IT and health), why shouldn’t I overweight that sector myself and invest more in it?

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.