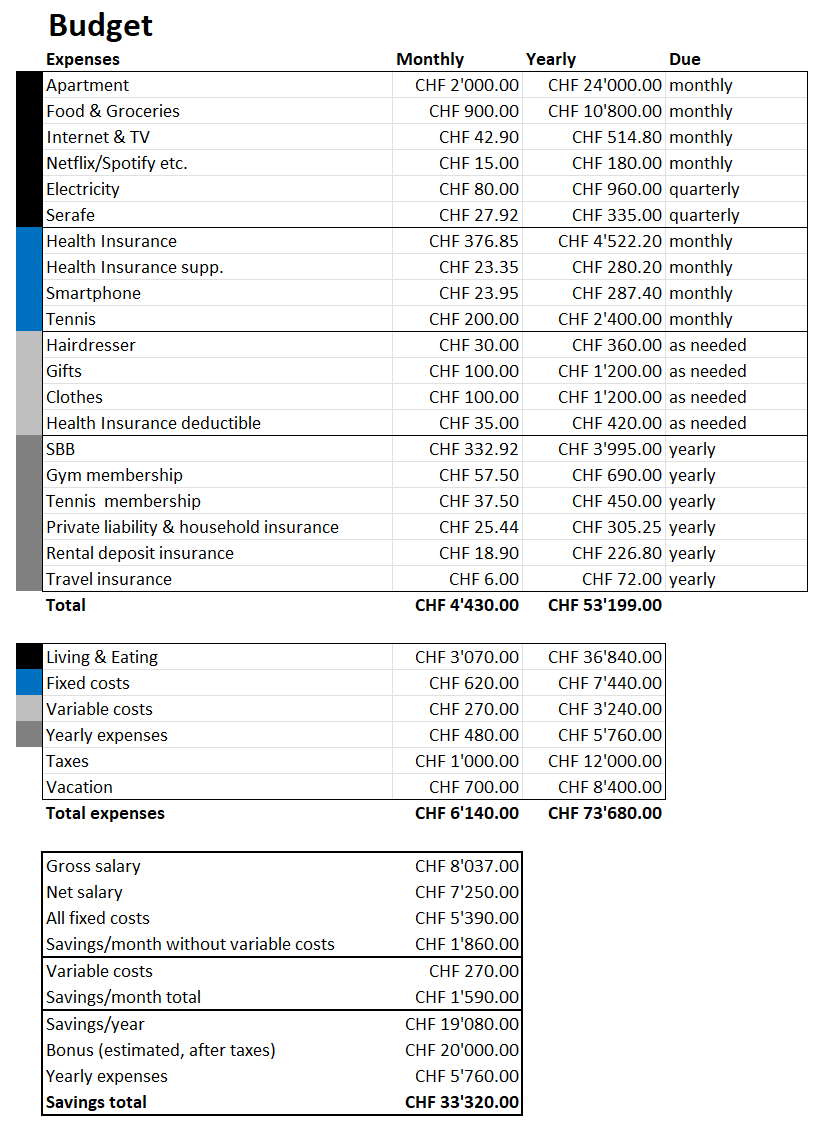

I always considered myself a rather frugal person. No car, cheap lunches while my working colleagues regularly go the restaurants, optimizing all regular spending by looking out for good deals etc.

Splitting up with my GF and moving out increases my costs by 1.2k/month. But still it seems rather odd that I can only save 1.6k/month on a 8k/month gross salary. Is my lifestyle far away from being frugal?

My expenses are very similar to yours, except for SBB and tennis (clear transport need and specific sport you like - so still all reasonable), and vacation.

To me vacation sounds a bit much and the only room for saving opportunity (but hell if you enjoy it - spend it, you earned it).

Do work out a lot and need lots of food? Then could be fine.

In comparison, I‘m an athlete and I am at 500-600 / month, and I eat about 3000-4000 kcal a day.

I do however shop 80% at Lidl and if there are special offers for meat I stock up my freezer etc.

Also generally buy lots of stuff in bulk online or on offer.

Rent seems okay-ish for a single.

Tennis you need to have memeber ship + pay each time playinz probably?

I guess you play a lot?

Not critique here, I approve of sophisticated sports activity. It costs what I cost, what can you do.

Gifts 100/month seems high? What do you gift whom all the time?

Houeshold insurance, do you really need it? Is your houshold expensive enough that it‘s worth it to cover?

I only have private liability for 60/year.

Rental deposit insurance, due to no caution?

Vacation at 8400/ year is also rather high to me. But I‘m single currently so not much vacation pressure

Mind you this comes from a pretty frugal person.

Overall nothing too crazy and not that much to optimize. But I do think you could get an extra 5-10K per year from optimizing food/vacation/gifts

8 K gross, 1 K tax, 1.6 K savings and 700 CHF per month vacation means you are spending 4.7 K per month on your actual expenses and 700 CHF on vacation.

4.7 K sounds very reasonable. I wouldn’t worry about it. In fact I don’t know many people who spend less than that.

700 CHF per month on vacation is quite high but that’s totally dependent on what you consider normal. But if you ask me, frugal people will never spend such money on vacation.

Last point -: 20% savings rate on Gross income is not really so bad. Bonus would be in addition I guess, you can technically save all of it.

P.S -: I am not frugal even though my friends say I am ;). So maybe my observations are from POV of an average person.

I see some big differences e.g. your food budget is almost as high as ours for a family of 5. Your holiday budget is about 3x what we have for a family of 5. Bringing these 2 line items down to 10k will increase savings by 50%.

In the end, Switzerland has high fixed costs, so the key is to increase your income to benefit from a kind of ‘operational leverage’. Doubling your income can lead to 5x savings. So rather than cut back, maybe focus on increasing income through career and additional income streams.

I spent a lot of money on travelling in the last 7-8 years. Probably around 50k, but I don’t regret one single CHF. I have seen so many places and had so many great experiences. It’s just something I love doing and I’m not sure if cutting this in half and saving an extra 4k/year would be worth it. I would get to FIRE sooner for sure, but I might regret holding back there. I know too many people (also clients) that are telling me “when I’m retired, I’m going to travel the world”. Well who says that you’ll still be able. Health shouldn’t be taken for granted.

But of course there are several things one could argue I guess:

Apartment was built in 2021. I could have found one for 1.3-1.6k/month in the same city, but it wouldn’t be as close to the train station (important to me as I don’t drive a car) and/or as modern. As I spend a significant amount of time at home, I prefer a nicer place. Plus commuting time is 40/min per way, so I don’t want to increase that by another 10-15min by not living right next to the train station.

I could probably cut down further on food and groceries. As I’ll live in Rheinfelden, I could buy more food in Germany and cut down on restaurants too. I’m not sure if I will really need CHF 900 per month though, maybe I’m overestimating this.

Sports is expensive in my case. Tennis membership and gym membership are 1.2k but the monthly costs make up a bigger part. Weekly tennis coaching, new strings, overgrips etc. and then of course the higher food (and especially protein) consumption.

Gifts seem high, but I have a rather big family (parents, 2 brothers with one of them having 3 kids, 2 close cousins with 6 kids in total…I’m invited to like 20 birthdays/year. I don’t go to all of them, but I should spend CHF 50-100 per gift).

Clothes: I don’t really spend much on my everyday clothes. I’m not into fashion at all, most of my shirts cost like CHF 10-20. But I need suits etc. for working.

SBB is just the GA. I could reduce this by taking a Streckenabo from Rheinfelden to Baden. But as I don’t have a car I would need to pay for every other trip I’m taking. Visiting my brothers, parents or friends, going to Basel or Zurich. I haven’t run the numbers in detail, but my gut tells me that the difference won’t be significant at the end of the year. So why bother and not just taking the all inclusive solution so to speak.

Insurances: It’s just CHF 600 per year in total. Don’t think saving here would be worth it. It’s for peace of mind.

your budget is good. The only thing that i consider interesting is your health insurance (go for a higher deductible) and SBB. You shouldn’t be spending 4k with SBB. Other than that, I think you are fairly goo…

Already discussed this with my boss. He admitted that my current 96k base salary is on the low side for Wealth Management and that he plans to increase that to at least 120k in steps, starting in the beginning of 2025. My total comp for 2024 is 132k including bonus, so I guess it‘s fine. But I aim to increase this to 160-180k within the next couple of years. Have to be patient.

It doesn’t matter if other people think you are frugal or not. What matters is what you want from life.

The beauty of being members of this forum is that we understand the trade off. We can plug savings into a spreadsheet and understand the likely impact of current spending decisions on our FI date, then decide.

If you are looking for ideas where to cut back I agree with the previous comments. Regards tennis and gym costs, did you look into the combination with supplementary health insurance and whether there is an option to pay a higher monthly premium but they reimburse sports ? SWICA pay me 800 CHF/yr plus ~250 CHF/yr in vouchers for activity tracking

Obviously, you cannot project exactly how much physical activity reduces your risk of mortality/illness but it sure does. (that means that you do actually save in contrast to someone who doesn’t do any excercise)

Could you get 3 pairs of running shoes and have the same amount of activity or even more? Sure, but if you’d enjoy running you’d already do that.

I would do some calculations here. If you check the Halbtax Plus (even the highest tier where you pay 2k and get 3k), it could make quite a difference in the end. I wouldn’t stick to the GA only because of convenience but mainly because it makes financial sense. There are also daily Spartickets for ~60 CHF where can enjoy GA life if you do super long trips.

→ if you however need a streckenabo from Rheinfelden to Baden, I agree with your GA conclusion. Streckenabo itself would be like 3400 CHF yearly.

Smaller points I see (but won’t make huge difference):

-Smartphone: I assume you mean the subscription? Then there would be cheaper options (I pay 11.- for unlimited in CH and 1GB roaming) for likely a similar offer. If it includes phone amortization it sounds good though.

-Health insurance: I don’t know your age, but if I assume 30y in Rheinfelden you can get basic insurance for ~280.-/month. Thats 100.- per month! Given that you are okay with some models like calling a free hotline before you go to the doctor etc.

All the basic insurance covers the same, so personally I change them yearly to the cheapest one.

-Electricity: Don’t know the price in Rheinfelden, but 80.-/month for a single household seems very high, unless you run mining rigs, lots of freezers (or A/C), using the oven long and often etc., no?

The rest looks good to me! Not hardcore frugal, but reasonable spendings while still enjoying your life!

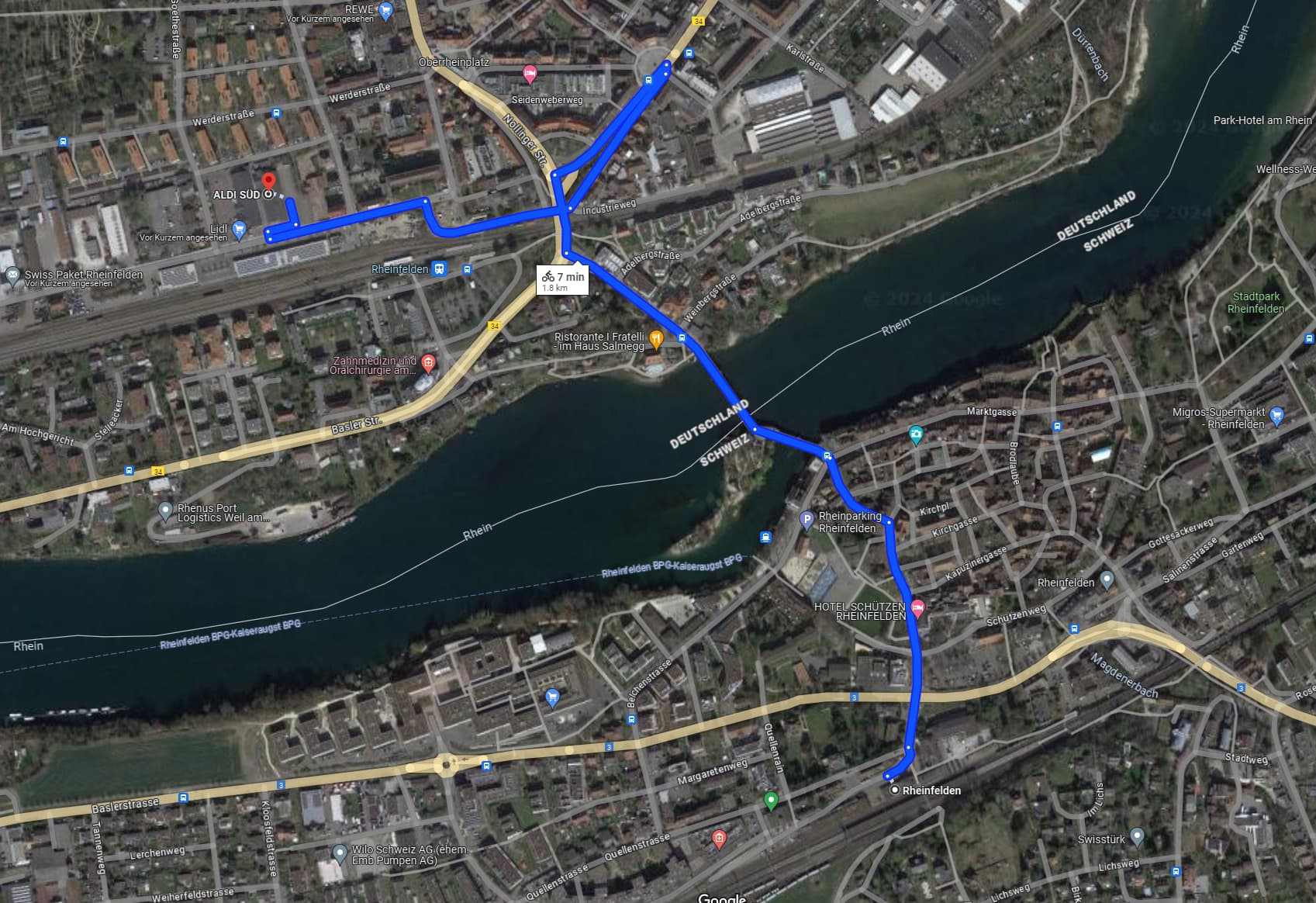

Regarding public transport I have several options (half tax is paid by employer):

Streckenabo Rheinfelden-Baden would be CHF 2’511 per year. Any other trip would cost me extra.

TNW U-Abo CHF 824 + A-Welle CHF 2’691 would be CHF 3’515. I could go to Basel, visit all my friends and family (BS/BL/AG/SO covered). Would only pay extra if I go to Zurich, Luzern or other places.

GA would be CHF 3’995.

One daily TNW ticket (going to Basel and using the trams there) costs CHF 13.10 and a single fare trip to my brother and back would be CHF 8.40. I would do this quite regularly to be honest, 1-2x in winter and 2-4x in summer. So I think option 1 would cost me more than option 2. I’m not sure about option 3 though. If I start dating someone in Zurich for example, GA would be definitely worth it.

Smartphone: I already tried Sunrise (and Salt many years ago). Network coverage just isn’t good enough for me as why I reverted back to Wingo.

Health insurance: I need the 300 CHF option. Don’t want to get into many personal details, but everything else would be more expensive. I just checked and Rheinfelden would be even slightly more expensive than now.

Electricity: Just a guess on current consumption and expenses. I think I’m going to use around 2000 kWh and that would be CHF 70 per month in Rheinfelden.

I might need less for food & groceries. Aldi, Lidl, REWE, DM, Swiss Paket, H&M, Deichmann are all there within 1.5-2.0km. I need 5min with my E-scooter. Germany prices and you get the MwSt back.

Like others, I’d say your budget is mostly fine. My few remarks:

Apartment: 2k is on the higher side of it in my opinion, but location impacts it and it is very important in life to feel well where we live. I’d not save too much there and given the floor plan of the appartment you’ve provided, this is probably fine.

Food: 900.- is not frugal, even for bulking up. For a frugal bulking budget, I’d aim at 350-400.- with mostly cooking and meal prepping at home. Internet/youtube searches can yield plenty of cheap bulking up recipes. The extra expenses may be worth it to you, though.

Tennis+Gym makes sports rather high but it’s also very worth it. With time, I may try to save on the tennis coach and do tennis with friends instead (there again, the coach may be worth it to you).

Clothes: 100.- is not frugal in my book but you do have to present well at work so it’s probably fine given your situation.

Vacation: 8.4k/year is not frugal, there are plenty of ways to travel for cheap and reduce that budget if you do wish it. There again, it may be totally worth it to you (as you state it).

I wouldn’t worry too much: 1.6k/month is what you save on your base salary. That means all of your bonus, potential 13th and 2nd pillar savings contributions are extra savings on top of it. If your purpose is FIRE ASAP, I would cut on varrying expenses. If your purpose is healthy savings while still keeping a balanced life, your expenses seem pretty fine to me.

Everyone is saying how this is totally fine, which it is, there are people burning through more than 10’000 per month and racking up debt. Who am I to deny them their choices?

But for what is possible in Switzerland, we could also notice that Budgetberatung Schweiz (German) states that around 2500 is realistically doable for a single person. This is in line with my experience.

This is without the more esoteric options of saving money (e.g., sleep in a tent or on the street). For example, I once spent a grand total of 20 CHF on food for 5 days to see how low I could go. I had pizza, spaghetti, bread, cheese, tomatoes, carrots, and apples.

These extreme measures are not required, but you could still spend double on vacation and save even more if you started cutting. Not that you have to, but you certainly could, if you wanted.

Main areas for cutting (in stark contrast that nothing can be done):

Vacations: Does it need to be 5-stars in Japan 2x a year, wouldn’t hitchhiking in Europe also be an adventure?

Food: Don’t want to do fancy meal prep? At least buy bread, sausage, and apples in Migros instead of Sushi in the restaurant. Colleagues go to eat in expensive restaurants? You need to lose weight and take something small.

Home: Why need 2.5 rooms, when 1 would do? Or get roommates to help pay bills. Have them be subtenants, kick them out, if they are annoying. But better chose nice and interesting ones. This could also build strong connections.

Variable costs: Do you really need this much each month? Don’t skimp on health, but what is this 100 CHF per month for clothes? Pants cost maybe 30-50. New pants every week? Do you really need 100 CHF per month to keep your relationship with other people running?

SBB: Do you really need a GA?

Memberships & exercise: Don’t skimp on health, but wouldn’t you be able to get a workout by running or using weights and your body at home? Running can also be a social activity.

Edit: Suggestions ninjad by others.

Put the difference in Total Market ETFs, become lower level rich in your lifetime, or do the RE part of FIRE. Anyway, not needing much will make you free from many things, and free to do other things, just not free to spend most of the money you have for consumption.

A lot of valid points so far. Some things can’t be changed (I obviously already got the apartment and also want to keep it), but there are things I could clearly spend less.

Limit restaurants to max. 2-3 times per month. Use Lidl/Aldi/DM in Germany to buy most of the food and Coop/Migros for some things that I consider worth it (especially meat). This could reduce food & groceries down to CHF 500 per month and increase savings by CHF 400.

My younger brother will also register at the tennis club in Rheinfelden. We agreed to play once a week together. Maybe I could stop with coaching and just play with him. Would save me another CHF 200 per month.

Spend slightly less on clothes and gifts, could save another CHF 50 per month.

Maybe slightly reduce my vacation budget as I stopped enjoying all inclusive hotels and started exploring more (will visit Thailand again in January 2025 for 3 weeks). So 6.6k might be sufficient which would save another CHF 150 per month.

Total savings would increase from CHF 1’600 to CHF 2’400 per month (+50%).

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.