Has anyone done a budget for retirement or have actual figures? I tried to make one mostly based on current costs. But still have a few things for kids in there and probably life insurance will drop off. I added a catch-all 2000 per month for retirement activities/hobbies/travel but I’m not sure how realistic that is.

Happy to get feedback on anything that looks wrong or I missed.

What the hell are you powering ? Taking todays cost of approx. 25 cts/kWh that would mean 7’200 kWh/y, and energy costs are rather going up than down. (only thing would be electric car and heat pump, but you have also oil and fuel, so would be redundant).

Average electricity usage for 4 persons is about 4’000 kWh/y

This would mean about 4633 L/oil per y (at an actual price of 108 CHF/100L, which is equivalent of 45’000 kWh/y. This would correspond to about 280 m2 of living space for an average heating usage. So either you live in a huge house or you should really think about renewing your insulation (or tell the kids to f*cking hurry up in the shower).

Should be about half if I look at actual black friday offers ?

This is higher than my average credit card bill (total) for 2 persons per month, and you already have 1100 CHF for food. What kind of hobbies do you have that they are so expensive ? Once you got the stuff you need, hobbies are mostly not that expensive anymore… BTW, you also have 130 CHF/month for trips, 60 CHF/month for sports and 250 CHF/month for Holidays…

For how many persons ? Including restaurants or not ?

Just wondering, are we still on a mustachian forum ?

You are right. I took a heavy month and extrapolated it, but the average is actually only 90 CHF per month or around 4400 kWh per year. Which isn’t too bad for 3 kids who do not know how to turn off lights…

Yes, we consume around 4000L +/- 500L of oil per year. The number might be higher due to the oil price spike after the Russian invasion which was when I took the cost after filling the tank then - rather unfortunate timing

Maybe we can get that down to 360, but yes, it is a large old house.

Yes, actual internet is 43 per month, but then there’s also the cablecom connection tax which doubles it. Maybe when fiber internet comes, this will be reduced down to 65 per month.

Food shop is for 5 people, no restaurants (we don’t go to restaurants) but includes maybe 120 per month for lunch at work. But I think 7.87 Fr. per person per day for food is OK.

Work from home gives food savings too, as then all meals are home cooked instead of having to spend money at the canteen (and I’m way too lazy to pack a lunch!).

250 a month on holidays is only 3000 per year budget for a family of 5…

60 per month is a weekly badminton court

I just put this as a placeholder as I have no idea how much extra will be spent in retirement. The friends I know in retirement are travelling a lot, which I guess is expensive. Right now, I feel that we are doing nothing as all time is just spent working and dealing with the kids, so I have no free time to actually spend any money. Although looking at the numbers, ‘doing nothing’ in Switzerland is not cheap.

I figured after retirement, I’d have more time to do stuff which will cost more money.

Yeah. There are things like university costs and wedding costs which appear in my model on specific years. Here, I try to include a typical year excluding these ‘special events’.

These are also in today’s money. In my model I inflate the costs for inflation.

I’m a little nervous also because I’m not sure how much kids will cost me as they get older. So the 2000 was a bit of a filler bucket of unaccounted for expenses.

But even if we exclude that 8k per month was a lot more than I expected, because the last time I did a budget/review of expenses, was in 2010 when I was single and spending around 2.5k per month.

I think if I make the corrections and reduce the 2000 to around half that, I end up with 8’500. I think the big ticket item is housing. Maybe with kids gone, it makes sense to sell/downsize and then I think I get down to a more sensible 7’200 per month.

This shows again that expected expense estimates depend on the individual situation one is experiencing. I’m currently planning with only half of your amount per month (5K), not including taxes. But I don’t have a wife, children, houses, cars, etc.

I do include a 2% inflation increase for 90% and 4% for 10% of my current expenses per year in my calculations. 4% for health related expenses.

Roughly results in doubling my monthly expenses after 30 years.

I am pretty sure that there is potential to reduce your oil consumation.My parents had the same number,I reduced it almost by half only by adapting the settings. Did the same at my house.

I think, you have all parameters needed - focusing on the numbers is probably a bit early, depending on your age.

I would add a “Pharma” category; couple of years after retirement, the need for drugs will increase heavily, statistically seen. Moreover, I think, 2k p.M. for retirement hobbies could be more or less right; the more time you have the more you will automatically spend.

Statistically, the spendings for hobbies will have a hefty increase starting retirement and the older you get, the lower they will be (maybe the category “gifts” will start to increase for potential grand-children). Moreover, medical consultation and drugs will also start to increase by ca. 70y.

I checked today, and my electricty rates are about $0.4/kWh (USD, I did a calculation where the currency was USD so just remember the final number and not the original CHF rate)

Also, I did something that I should have probably done at the beginning: I downloaded all transactions from UBS for the last 3 years and calculated what the total outgoings were. It also helped to identify some missing expenses (mostly kids activities which added up to a lot more than I had imagined!)

Never did a budget in my life because nobody knows the future.

But it took me 16 days to spend my first AHV in BBB (Beer, Booze and Babes, had a hard time to come up with that name). For fairness I have to say it was in Spain where you still can get a beer in a bar for a buck (wow, another BBB).

That missed my goal to spend it all in one night! 47 years ago when I first had to pay AHV I would have been able to reach that goal with any amount!

Can’t speak for @PhilMongoose, but 5k/month in taxes is about what you would end up paying for taxes on about 200k of taxable income in Zurich (city of Zurich, municipal, cantonal and federal taxes accumulating to about 60k p.a.).

Right — yes, for earned income. But in early retirement, you’re generally living off your wealth. At a spending level of 10 k CHF per month, you’d need around 3 million CHF in invested assets, based on the 4 % rule. I’m leaving the 2nd and 3rd pillars out of the equation here — they can be considered a ‘bonus’ at that stage. In Geneva, a 3 million CHF portfolio with a 1.7 % dividend yield would result in roughly 6–7 k CHF in annual taxes under the current rules — and Geneva isn’t exactly a tax-friendly canton.

What am I missing here? I ask not to challenge your assumptions, but rather to challenge my own planning!

There’s many ways to skin a cat live off your wealth.

One way would be to have your CHF 3M in liquid assets produce, say, 150k in taxable income. Maybe a little less, maybe a little more. As you’re still making some income from employment on the side, you end up with 200k in taxable income.

Another way would be to be completely retired, say CHF 3M liquid assets before you retire, add another 1M or so after you retire. This could produce 200k in taxable income just with dividends if you chose to invest (and consume) that way.

Any which way in between is feasible, too, of course, e.g. selling your capital gains instead of consuming the dividends of your cash flow producing portfolio, but since you originally asked how to arrive at 5k/month of taxes: I can easily see that path and in fact, I am pursuing that path.

But you’re missing 2 major taxes:

Wealth tax on 3M, which GE tax office will be sending you a bill of 17k for.

And the AHV-Beiträge (I’d say, falls under “tax”) for non-employed, based on your wealth, maybe 0.25% of 3M, let’s say 8k.

@PhilMongoose has surely, by then, put a good part of his 3M into 2nd pillar, which is then sheltered from the above 2 taxes!

So ja, even including the taxes above 60k is not “reachable” IMO, unless he is going for a lot of high yield stocks/bonds, all wealth outside 2nd/3rd pillar, an/or adding his family’s Krankenkasse and super-high electricity bill to his “taxation load”.

First, you shouldn’t forget wealth tax which can be substantial.

Second, assuming you want to spend 10k, you need to earn 120k, but you need to earn more than that to arrive at a post-tax budget of 10k per month. So you need to ‘gross up’ for tax. Only, when you increase the amount you need to earn to take into account tax, you notice that the tax rate rises, and so you need to increase a bit more etc. etc.

Also, I was looking at post-65 years (which hopefully are the majority of the years!) when pension shields are gone. That’s why there’s nothing for unemployment AHV payments and the title mentions ‘normal retirement age’.

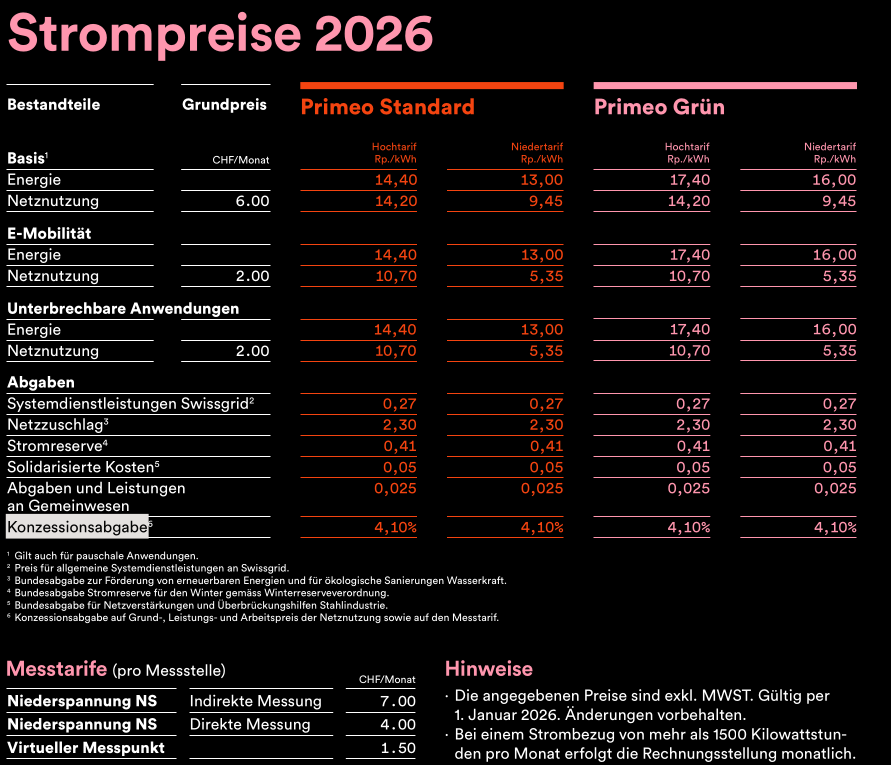

You can check primeo energy, they are my provider. I’m not even sure if I can change providers in Basel Land. They raised prices massively during Russian invasion of Ukraine and now that prices seem to fall, they say, oh, we will lower electricity prices, but basically increase the ‘grid’ prices by a similar amount so you’re stuck with the high prices.

IIRC, next year, the grid charge is more than the actual electricity charge.

It’s a bit intransparent, since they charge a flat 6 Fr per month in addition to the unit price so you have to divide that by the total consumption and add it on. Also prices they quote don’t include VAT.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.