I’m convinced we reach the end of a cycle however I’m about to pull the trigger on a 1.5 Mio chalet in a famous ski resort in the French speaking part of Switzerland.

I’m calling your contrarian spirits and kind souls to share your counter arguments with me so I could potentially reconsider this potentially (very silly) decision.

You provide absolutely zero information. We need a whole lot more if you want us to weight in on this decision. I hope you did more due diligence than what you are sharing with us.

From a valuation standpoint the chalet is aligned with similar items in the area

I don’t have an expected return per se as I believe I can’t predict market behaviour and I don’t plan to rent it however I know that compared to our existing monthly rent our quality of life will improve for a similar amount of money spent per month

Today I pay 2700CHF of monthly rent vs a 2200CHF of monthly mortgage repayments (calculated on a fixed 1.2% rate for 10 years) for a much larger place to live

I believe that even if real estate prices crash (next five years) and then recover (from year 5 to 10) it will always be money not “thrown away” to a landlord each month.

the down payment will be around CHF343,500.00 (notary fees included)

I’m forecasting operating costs for the property to be 1% of the acquisition value per year so it should be CHF15 000. Please note that I believe a good chunk of these will be tax deductible

If I add mortgage repayment plus operating costs I end up at CHF3,530 of monthly costs

*I don’t plan to rent the chalet for short term rentals but it could be an option in a couple of years time

Now if I rent the chalet for 10 weeks per year at CHF571 per day / CHF 4000 per week (for 10 weeks per year)

Total yearly rental revenues CHF41,683.00 (which is almost a break even from total cost of ownership for an entire year (meaning mortgage costs + 1% of purchase price for maintenance)

Net operating income per year is CHF26,683.00

Cash on cash return (gross) is 7.77%

Cap rate of 1.73%

Monthly cashflow is still negative, it’s -CHF673.61 (but not too bad compared to the -2700CHF I pay monthly for a lower quality of life as a renter today)

My Yearly ROI (on cash invested) is a -0.12%

I’m glad to share more details if needed. I’m also on the market for a financial advisor if you know a great one

The relevant data would be: how much rent would someone pay for this place (the repayments aren’t comparable).

IMO that’s the wrong way to look at it, owning your place is mostly paying yourself market rate rent. If the ROI of the property is like 1%, you might be way better off paying a landlord and investing the same capital somewhere with better returns.

Are you going to live in this chalet? I ask because you compare the future mortgage to your current rent. Do you already live in the ski resort town now? I can’t imagine living in such places, so cyclical over the year, locals a special bunch, others come and go seasonally, how far to commute…?

Yes I already live in a chalet in this ski resort for many years

I don’t need to commute as I work remotely.

I like the idea of living here for many years to come. I also potentially think of buying another house abroad on the beach so I can switch homes and rent them out when it’s peak of the season.

From a purely financial perspective, it doesn’t seem to make sense. Though from an economic standpoint (in the wider sense of it), it can, for the enjoyment you get out of living there.

I agree it can be useful to hear / read contrarian opinions - yet somehow I get the feeling you’ve already made your mind up. You want that chalet. And it’s not for financial reasons.

Hard to argue against that.

If you can, try to put a price on the enjoyment you’ll be getting out of it.

…which, if I understand correctly, you don’t plan to anytime soon?

Eigenmietwert. Not a lot of money but it should be considered

If you live in Vaud, you are currently deducting your rent from taxable income. If you live in Valais, this does not change

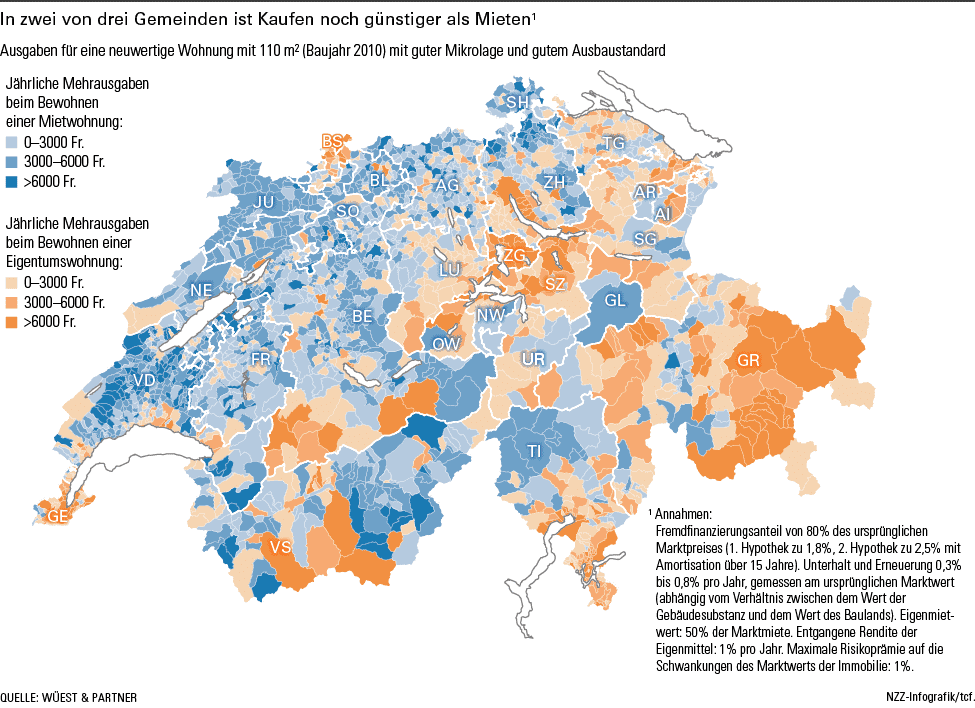

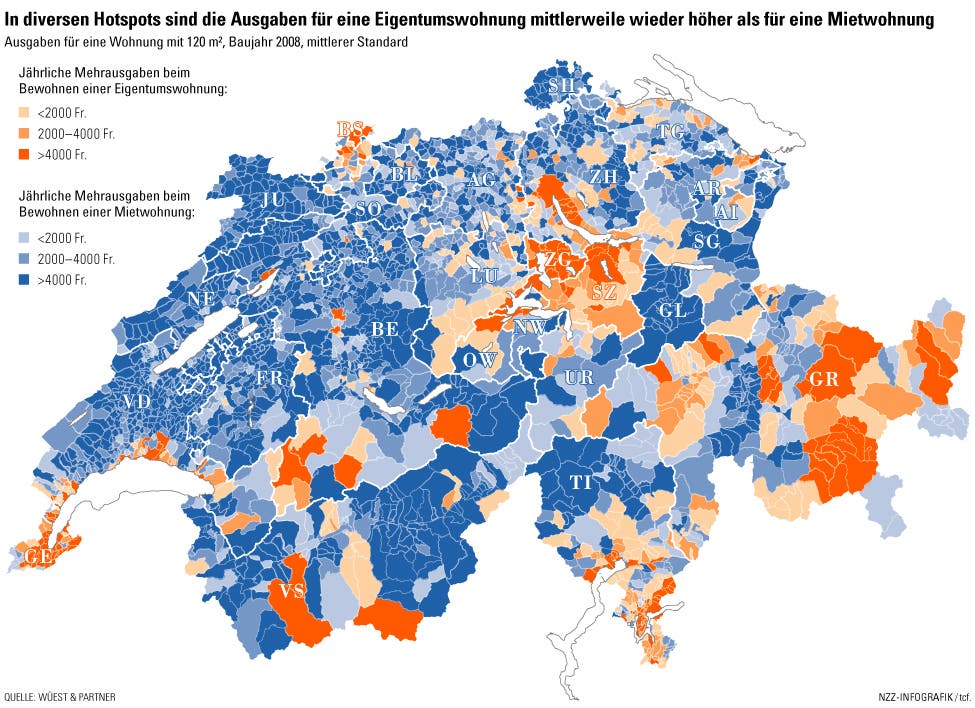

Wüest&Partner and CS are evaluating rental vs. ownership every now and then. CS is pretty optimistic that ownership is cheaper almost everywhere (for me they are desperate selling mortgages) while Wüest&Partner gives more detailed information per municipality (see attachment, red=rent is cheaper, blue=ownership is cheaper)

sorry it’s from 2015 but no media have reported sinking real estate prices so far.

Ah ok, then buying could make sense. I didn’t read that out of your OP. And sorry, I didn’t want to “bash” living in a resort town, just feel it’s not for me. Living where most others only can come on vacation is surely also a nice feeling. :-)

You need to separate the investment aspect from buying a home/lifestyle aspect. Which is more important to you here?

Financially = compare the returns from this chalet with low cost index funds

Emotionally = could you achieve the same lifestyle/home goals at a lower cost?

I’m right now selling a chalet at a famous ski resort in Kanton Bern and I’m happy it is “only” 490K since that money has not worked at all as hard as the index funds (at a long term time horizon). I’m happy if we break even on the sale.

We are now moving to a small, cosy apartment in a good location in a Nordic country that allows us to FIRE immediately and move on to pure fun projects.

Bump up. Same dilemma with a flat with an asking price of 1.2M, property ready in 2023.

I know it’s financially not the best option vs stock market investments, but:

am a bit reluctant to put large sums into stocks near our ATH. It might go another year or two but inevitably we will run into a larger correction/crash again (my view)

you gotta live somewhere and putting 36k every year into some pension fund’s pocket for rent starts to bother me. Owning is still cheaper for the next 10-15 years in a newly built house (no renovation costs)

Zürich and surroundings are getting more and more expensive and I’m not counting on a reversing trend much

I’ve piled up a lot of 2nd pillar pre-savings exactly for this purpose years ago

I can lock in 10 years under 1% easily, then in 10 years I’d probably have the capital to cash it out if needed (or have the bargaining chips for a good renewal)

we can reserve now and pay in 2023, which means I still got 2 years to run on my ETF’s (I know it’s very risky - should anything happen we can still sell in 2 years before moving in)

I can’t leave Kt ZH as I’m closing in on my Swiss passport’s timeline (2 more years)

We can probably easily rent the property out as it’s very close to schools and central in the village

I don’t see much downside, but it’s a lot of money, so please help me see all the horrible things that can happen.

4.5, 121sqm, EG, plus garden.

(here’s the project website)

It was a theoretical first run on the numbers. I would want to lock in rates to have a peace of mind and not need to renegotiate financing in 3 years (where I’ll have zero bargaining chips). I’m calculating instant savings of about 12k a year on rent, 2x3a contributions, plus whatever we can get out of investments and other savings - comes to about 50k at least a year. In 10 years I’ll have a 500k chip on my table. But yes probably we can break the mortgage better into 2 parts.

good to know, thanks. I’ve planned pledging in the first place and not cashing out per se.

and who’s controlling if I have replenished my pension scheme correctly before renting?

But definitely not 2 parts with different durations… that makes changing providers impossible (and they always suggest to split them in prime numbers so they rarely align. E.g. 5 years and 3 years)

I see no issue with the general idea. Just some free tips:

That’s not really a valid reason to not invest. Stock indexes historically have spent MOST of their time near all time high, so what?

Mean reversion after this crazy coronavirus stimulus induced rally? Maybe a reason to hold off, or DCA

You can’t leave your town, not just canton.

Beware such long term contracts are also a huge liability. Fix is fix in Switzerland, you cannot break the contract without consequences. You are committing into paying 120k+ (and with negative interest that most banks charge on early cancellation, possibly even double of that!) in interest in total in one way or another. Even if you sell, this will come out of your sale price

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.