I think what’s missing in your numbers is the opportunity cost of not having the downpayment money invested.

That said, my wife recently started fantasising about a place in the mountains which we would use during weekends and which we would rent out during the school holidays. I don’t see this a good idea for the following reasons:

A chalet in the mountains is probably more subject to market corrections than, e.g., a flat in downtown Zurich

Having to pay someone who would manage the property when it is rented out will eat up most (if not all) profit.

Of course I’m thinking about this. The capital we’d need is about 300k. This would earn “8-10% on average” - the problem is the on average bit. It might be -15% this year, then -5% next year then 0% for years afterwards, then 30-40% sometime (like in 2020). So there is no guarantee for the next 5-10 years about what’s gonna happen.

I haven’t picked a financing provider yet, but yes I’m aware of the concept. Considering all the savings we’ll do vs renting, I don’t think it would be a problem. Also sellers on used property are always counting with cashing out the bank first.

That’s the thing. I am looking at things that were not benefiting a lot from the pandemic, like Spotify. Years hovering around their average prices of $150, then boom 250% up in 2020. Lot of these will need to normalize somehow in 2021… the upside might be more limited.

US mortgages that run for 30+ years, backed by US government, allowing you to go underwater, cancellable any time without consequences are a completely different product with very different characteristics from swiss fix mortgages. And you pay 2-4+% in interest for them, not 0.x%

There’s a loose equivalent in Switzerland - variable mortgages. Costs 2%+ in interest too. Not very popular for this reason

I thougt the higher interest was mainly because of higher risk (less downpayment, less stable job, no social net) So no possibility for “Sondertilgungen” in CH ? (Finally found the correct word).

I know most of the people here are anyway more enclined to leverage, I am a bit more conservative and in the case of buying a self used RE, I would prefer to pay it down as quick as possible. My approach ould be different for rented RE.

About 1-2% delta is due to currency, the rest is due to different characteristics of the product - compare swiss fix to variable mortagages.

Most importantly, a bank cannot offload your variable mortgage on the open market and collect another 1% or so from other suckers, unlike with fix, it has to be you who pays everything with these. The other side of the medal is of course when you want out of a fix here, the bank wants that 1% out of you

This is possible and the recently introduced SARON mortgage specifically has a variant which allows you to prepay back a certain amount only 1x per quarter or year.

Obviously, for the convenience of this approach, the bank will charge you a certain premium over and above your negotiated mortgage interest rate.

For e.g., in our case, we were considering the full-flex SARON mortgage with 1x extra payment per year without any charges. For this convenience, the bank proposed to charge 0.2% more than the prevailing SARON rate (at that time it was around 0.66%)

0.2% surcharge is not that bad I guess to get that flexibility for extra payments (if the goal is to reduce risk by paying the house as quick as possible)

I mean I see more probable than in the next years interest will go back into positive territory again. If they increase much, your house value is going to suffer a bit.

I always think like this: take your net monthly rent (without charges: you are going to have similar charges when you buy, such as electricity, warm water, etc) and multiply it by 12 and then by 25, so in total by 300* net monthly rent. That’s the amount of money you need to have in the stock market to fully payback your rent without ever going out of money.

In my case is 1800 chf net rent per 300 = 540’000 chf . Comparable flat in my street are going for 1.2 million. No thanks, I prefer to save 540’000 in VTI on IB and know that even if I’m paying rent, I’m actually covering it with my investment if I want.

*This is obviously very much simplified; if yo uprefer a conservative appraoch (ie 3.3% swr instead of 4%, you can multiply by 360 instead of 300. In my case it would be 648’000 chf. Again nothing to do with the asked 1.2 millions.

Hope this sparks some thoughts.

In the end, buying an home is perfectly fine if it is what you want, the peace of mind and the emotional aspects. That for sure supersedes any financial calculation.

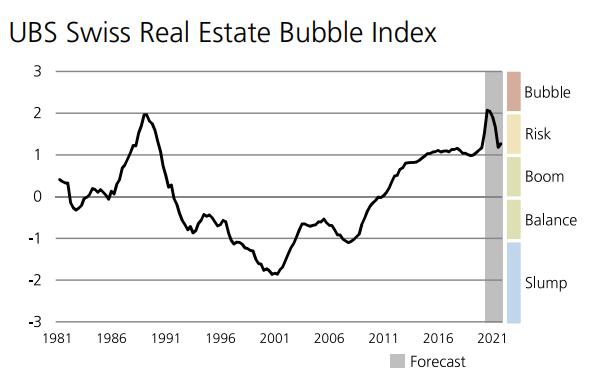

I think the main point is that RE is not reevaluated every second, and therefore people actually do not see how volatile it actually is.

In general people got the value of the house if they buy it, when they redo a mortgage every 10y (if any) or when they sell it. By the time of selling some decades afterwards, they do not take into account the inflation and the mind goes WOAAAAAH WHAT AN INVESTMENT IT WAS.

And then you can brag about it and it is much more tangible than some VT…

In my case is 1800 chf net rent per 300 = 540’000 chf . Comparable flat in my street are going for 1.2 million. No thanks, I prefer to save 540’000 in VTI on IB and know that even if I’m paying rent, I’m actually covering it with my investment if I want

Same approach for me considering self lived RE. But actually it is even worse since liquidity and maintenance. So actually you should multiply the monthly rent by 400 (considering 1% maintenance cost, which is rather optimistic. Sometimes you hear more about 2% maintenance cost (Gerd Kommer).

That is the solely financial part. Afterwards quality of life plays in, and this is not easily quantifiable.

For a 1.2 million house you only need 240k cash (maybe even just 120k with pledging pension money). And the downside risk are not more than 10-15% instead of 50%… ?

Whereas with housing due to the high leverage your downside can easily flip to negative. Potentially taking decades to just break even, c.f japan in 80-90s. We’re in everything-bubble, stocks, bonds, crypto, RE. Coronavirus rally hit all them, the loser asset was cash. Investment-wise I don’t see that much difference now between going all-in to stocks vs all-in to RE in prime markets like Switzerland. RE is actualyl riskier due to no diversification.

Unless you want to buy and hold the house for non investment purposes, such as to live in it for decades to come. But how certain are you of these plans? Since we’re on a FIRE forum and there may be decent chance you’d want to FIRE elsewhere than Switzerland due to how expensive life here is, you might want to consider the possibility that you’ll have to move. And boy there’s a whole world where 1/10th the swiss real estate prices buys you like 10x the space. You really want to commit to living in a tiny apartment because that’s all you can afford here?

I don’t see a real risk that Swiss real estate get’s cheaper with the current inflation and low interest rates… we don’t have unlimited space to build on in the end.

This is also a common myth. Switzerland has a massive amount of housing waiting for renovation. And raising 2 stories on top of houses could house another 5million people without any major downside.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.