I am in the phase of setting up my asset allocation and I am deciding whether to own a currency hedged world-equity ETF, or an unhedged one.

By reading around, see e.g. this post, it looks as if (Swiss) investors don’t quite hedge foreign equity.

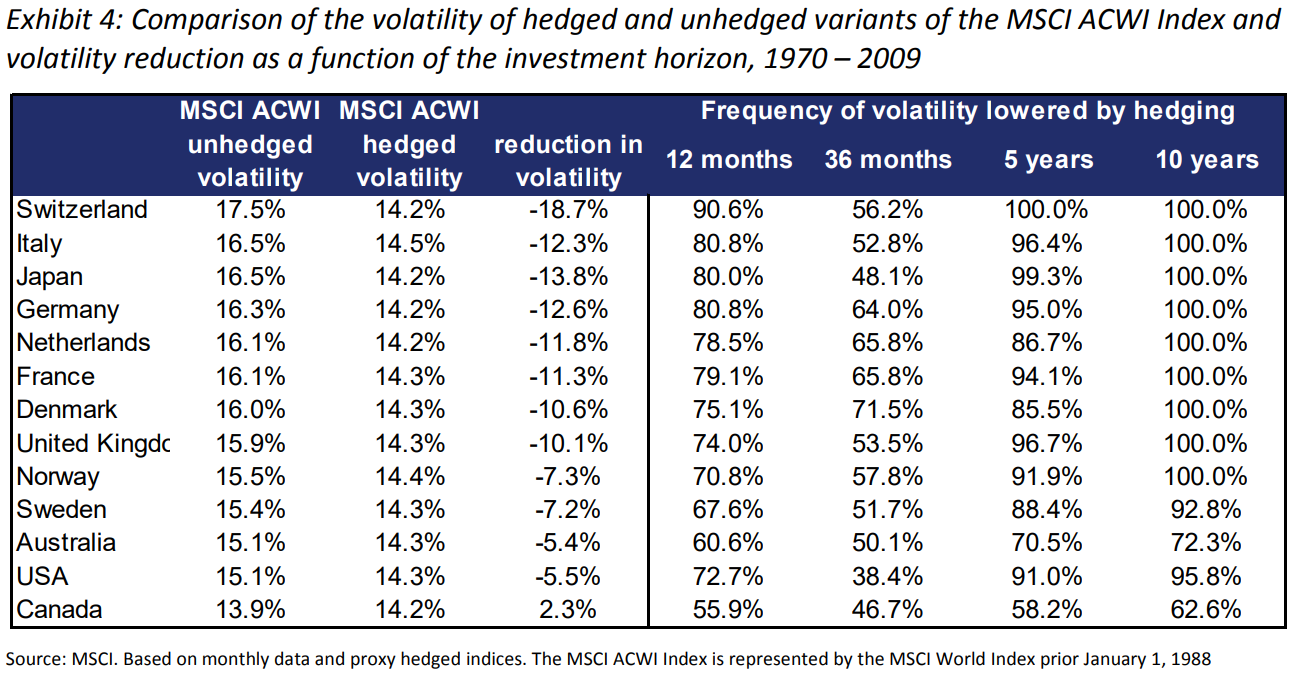

However, I don’t understand why. Consider this paper from MSCI. For the MSCI ACWI index (a world stock index), it seems that a Swiss investor, at least historically, could greatly reduce volatility by hedging:

without compromising returns (I assume that the return increase by hedging was eaten by the hedging costs, see also this paper from Vanguard)

So, why NOT hedging?

I can see a few reasons, please let me know what you think about them, and feel free to add more:

using the past to predict the future is not significant (but maybe, there are some “structural” reasons for the observations above that are likely to hold also in the future)

hedging equities eliminates some kind of diversification benefit, say, from having a home currency that is uncorrelated from the world stock market, or from just being exposed to multiple foreign currency (is CHF uncorrelated to world stocks? Are the alleged losses of such diversification benefits that significant?)

I wouldn’t call it a “cost”, rather, a return. It can be both positive or negative.

Anyhow, the article targets not foreign equity but foreign bonds, as far as I understand.

Over the long run, returns from hedged and unhedged foreign equity (but also bonds) should pretty much align.

If you don’t need to report your Assets Under Management in CHF on a, say, monthly, or quarterly basis, measured against some CHF hedged benchmark, what’s your benefit from reducing volatility in CHF?

I can see why it matters for a “professional” portfolio manager. They’re measured on a monthly or quartely basis against their hedged benchmark and their job & salary depends on not deviating too much from the CHF hedged benchmark.

But why would you care about volatility?*

You (IMO) in essence pay insurance for a smoothed out CHF value curve … which doesn’t matter if your horizon is years or decades?

Might also be worth looking at the sources advocating for hedging. Of course fund/ETF providers will happily offer you hedging and even tell you it’s great e.g. for reducing volatility … and equally great for them to make an additional buck or two for the hedged share class you’ll buy into.

YMMV, of course

P.S.: This topic has been discussed before on this forum.

* I could see hedging perhaps making sense if your asset allocation is 99% non-CHF, you’re quickly approaching retirement and you want to reduce currency risk (you’ll still pay for reducing that currency risk).

Is this scenario regular hedging, i.e., against the listing currency of each stock, not just USD, or is this partial hedging of only USD stocks, or some odd CHF-USD hedging of all stocks even for stocks that are listed in EUR, GBP, JPY?

With hedging costs, do you just mean the spreads of the forward contracts and possibly higher TER of the fund? Or do you mean that this completely excludes the price of the forward contracts (i.e., the interest rate difference)? The former shouldn’t make a huge difference (if an inexpensive hedged ETF is chosen) but the latter would make this data completely useless, as far as I can tell.

Well hedging certainly does cost something, it can influence the return, but still a cost, like an insurance premium. The article doesn’t once mention bonds?

According to the ZKB article: “The appreciation of the franc against the USD has been at an average of 1.5% per year for almost 50 years. Hedging the USD cost an average of 2.7% per year during this period – in line with the average interest rate difference between the USD and CHF. The continuous appreciation of the CHF was therefore not sufficient to compensate for the costs of currency hedging. On balance, there is a loss-making transaction of 1.2% per year on average (=1.5% appreciation minus 2.7% costs of currency hedging), which accumulates into significant losses over time.”

Conclusion: “If the interest rate difference is higher than the expected currency appreciation, it is not worthwhile to hedge the currency due to excessive costs. As we have determined in our analysis, currency hedging is not worthwhile if the interest rate differences are greater than two or even three percent. In the event of interest rate differences between 1 and 2 percent, the result is neutral”

Just to add on your points:

a smoothed out curve might make someone sleep at night and not quit their investing plan, this is more on the behavioural side but it could play some role.

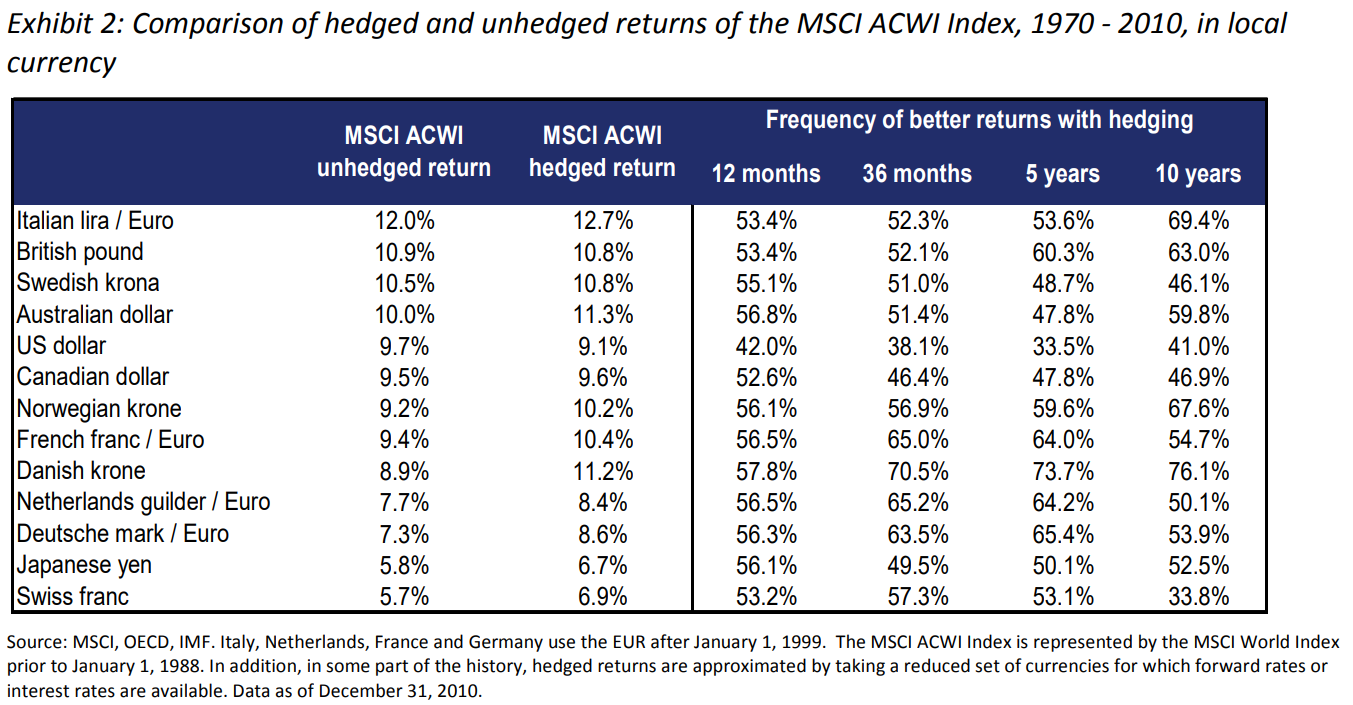

Yes, but as @oslasho points out, including more data in the time window makes the return bigger. Could be interesting to see the same column with “20 years” instead of “10 years”

@ternes11, the ‘cost’ of hedging (for some countries other than Switzerland it’s a ‘positive cost’), tends to bring the interest rate of the country you’re investing into (bonds), close to the domestic (bonds) interest rate, there’s nothing around that:

(bonus: and according to real interest parity, all “domestic” interest rates are equal after taking into account domestic inflation… there is no arbitrage opportunity in the long term!).

Your argument is (?), if I don’t hedge, I won’t have this cost, so my interest will be the one of the foreign country.

But this is wrong, because if you don’t hedge, you’re taking up a different risk (currency risk instead of hedging risk). And the same paper mentions that

investors might expect a similar result when remaining unhedged over the long run, with currency returns producing a similar adjustment for underlying fundamental differences across markets

Onto the ZKB article I believe that their reasonings make sense for short periods of time. Say you have a bond, and you want to use that bond in e.g. 2 years to buy a house. In that case, I believe it is beneficial to do the kind of reasoning that ZKB is doing (hedge if the interest rate differential is…), so that you don’t lose money in the short term, which is the horizon that interests you.

PS: can you please point to where the topic has already been discussed?

I did a search before posting (probably not thorough enough) and I couldn’t find anything.

This thread is about hedging foreign equity, not bonds? The article also only covers hedging in the equity context?

Why on earth would I do that? (With perfect markets ok, but that would assume no taxes, no illiquidity, no transaction costs etc.) Keep it simple and just have (or convert) your bond in the currency you want to use…

I think hedging currency makes sense in the short-term if you happen to know that a currency is depreciating above average, which of course no-one knows, which is why for (private) investors it makes no sense IMO.

Hedging long term equity portfolio for currency risk is mostly meaningful with respect to peace of mind but not with respect to actual returns. Because if you expect higher returns then there is no research to back this up.

I see it like following

hedging is a cost , so it should impact returns.

in Swiss investor case, the idea of hedging always comes with assumption that CHF will appreciate against the world. What if it doesn’t happen?

I would be surprised if expected appreciation of currency is not already somewhere in cost of hedging . It cannot be the case that one can expect to always benefit from hedging

Looks like we need to getvthis conversation back to the basics aka Data. Hedging Shares is a very important tool to protect against Governments‘ Financial Repression.

In theory, Hedged and Non-Hedged Shares have the same return. This however only applies if the central banks allows the interest rates flow to their equilibrium. Once that is given, FX losses equate to the Delta of interest rates and there is no point to hedge shares.

If this is not given however, you shall hedge the shares into a currency without financial repression. What does this mean in practical terms?

EUR and JPY Yen domiciled shares shall be hedged (whether against USD or CHF dosnt make a big difference

EUR or JPY domiciled Investors shall still hedge a decent part of their shares against a non repressed currency (e.g. USD or CHF)

Make it make sense. You hold internationally diversified stock, most of it with equally diversified international economic activity. You want to speculate on FX, go buy futures. You can even lever them as high as it lets you sleep soundly (or even more if you enjoy that, up to a maximum of the broker margin calling and liquidating you).

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.