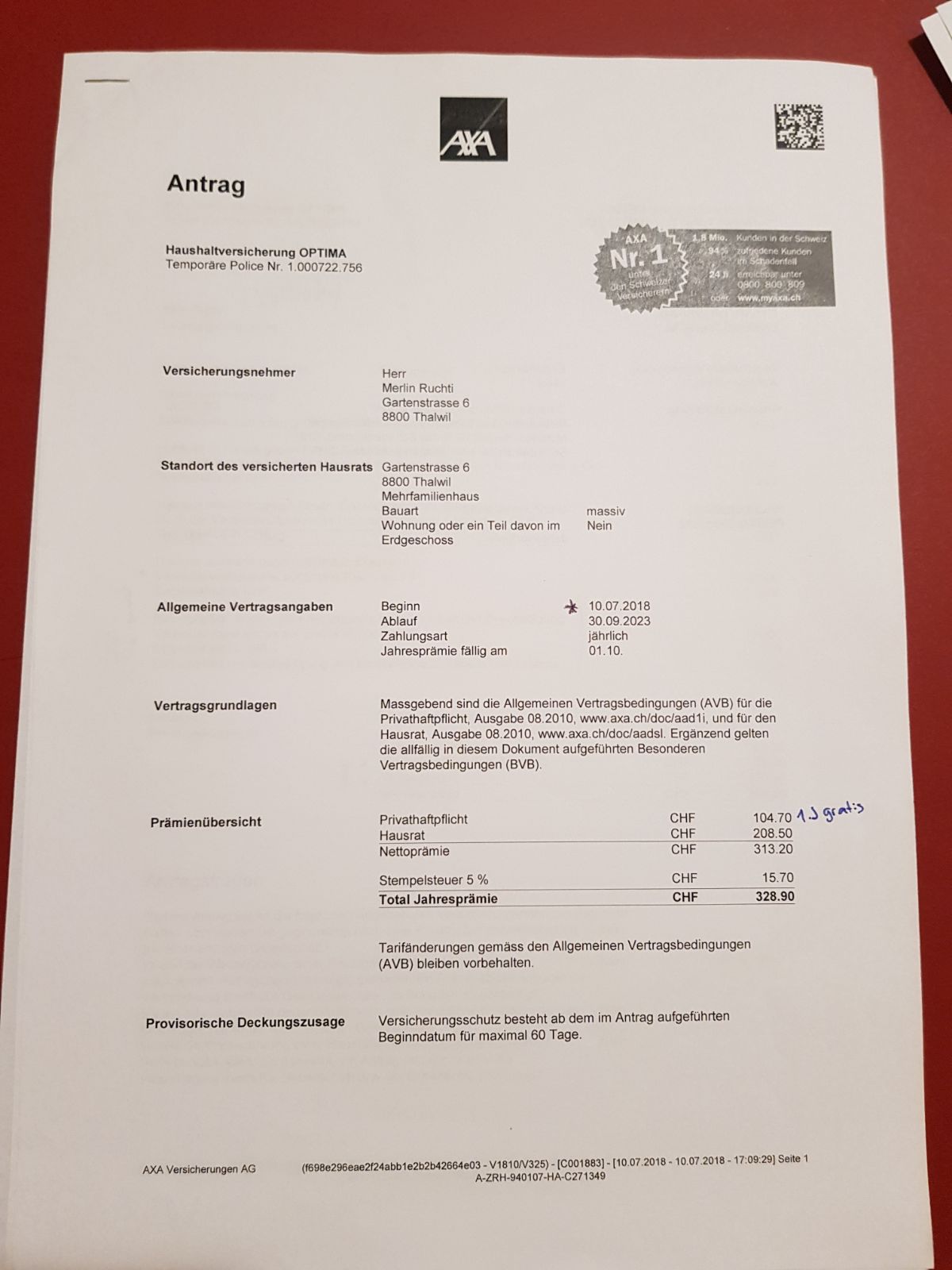

I moved out of my parents’ home and got my first offer for a Hausrat and Privathaftpflicht. The total is CHF 328.- yearly. I live in a rented flat where I have no own furniture and my most valuable belongs in the home are a notebook, smartphone and keys to the car.

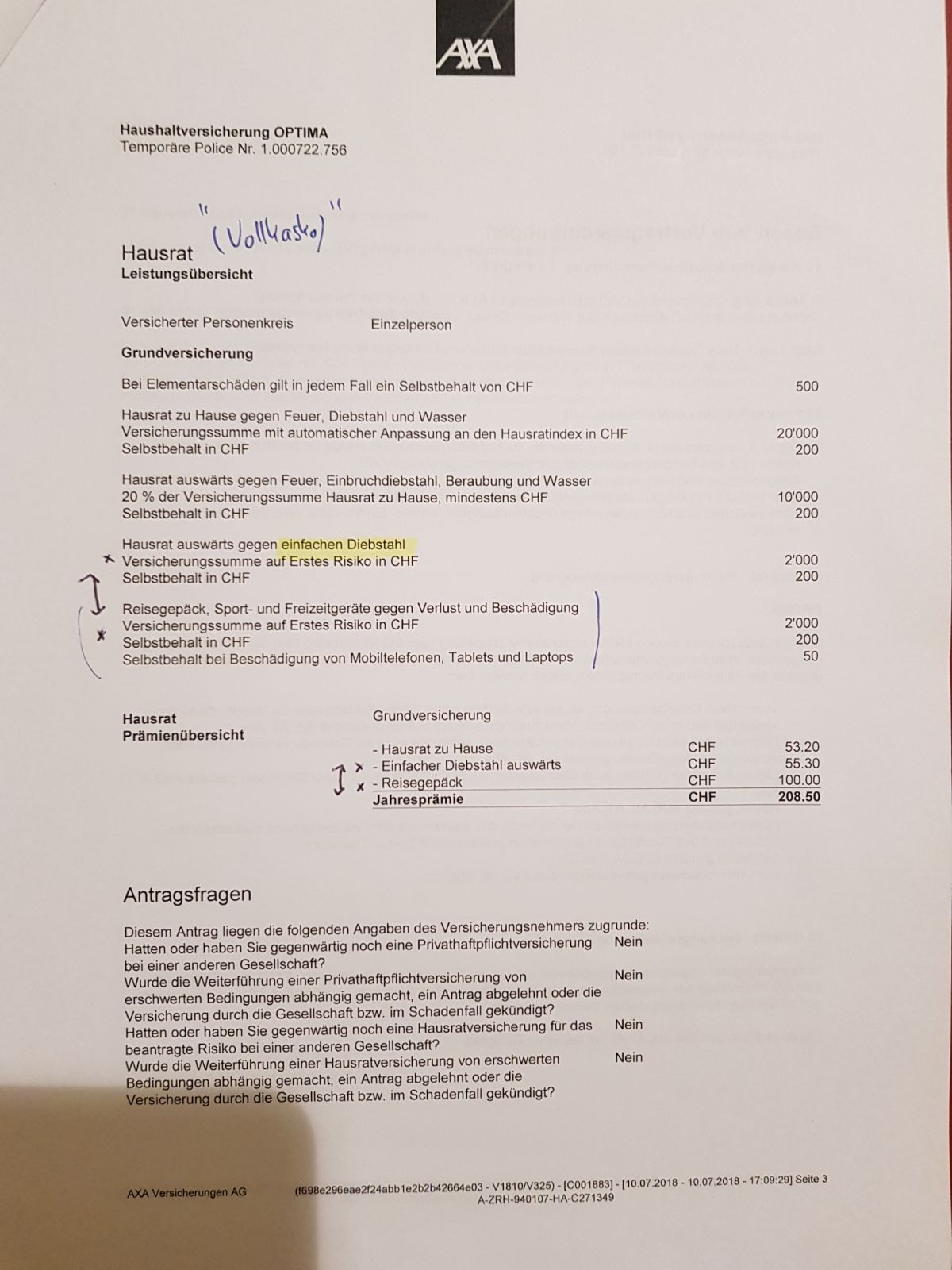

What do you think of it? One option is to remove CHF 100.- by removing the “Reisegepäck” option where my equipment (notebook, phone, camera) is insured for damage (e.g. handy falls down) and loss (theft?)

Did you try comparis? https://www.comparis.ch/hausrat-versicherung/default

Also it’s a baad idea to show your address online like that…

The contents insurance might get useful once you have something. Also you should read it well, because it might cover stuff that you thought they were covered elsewhere.

I have recently made some researches in this regard, Baloise is the cheapest one by far for people under 30. Furthermore, they offer a very good coverage.

I checked myself and I pay about half of the quoted price with a value of the furniture three time higher. Civil responsability is also included. Some extra in the offer are questionable as they are not compulsory and offer only limited coverage (Einfachen Diebstahl, Tablet, smartphone, Sportgerät). All these objects are covered with an amount than anyone in this forum should be able to cover quickly but make the price of the insurance much higher as claims are probably frequent.

I decided against having Hausrat for now as I’ll move back to my parents home in six months when I start university. For the future, I will keep the Baloise package in mind, it seems to be the best for young folks.

According to Comparis, the cheapest Privathaftflicht that covers “Fremdlenker” (driving other people’s cars) is from Helvetia and costs CHF 78.- compared to the CHF 104.-. My family is insured with the AXA guy and he is an aquaintant, so it might make sense to do it with him. The Mustachian spirit would be to take the cheapest though…

I know it’s a bit late if you already signed, but since you want to go with AXA did you check their website? There is also a BASIC product which is not really worse in Private liability - just cheaper.

By the way this is a 5 year contract - did you notice?

I disagree here. I very occasionally borrow my Mom’s car to move some stuff & find the 10 or so francs per year that this option costs worth it. Any damage to a third party wud spoil my Mom’s bonus level that she “earned” and is all happy to be on. I would feel very bad about that. Also I drive a car rarely these days and have noticed slipping up a bit re attention span etc when driving from being so used to only cycling moat of the time. I wud say my risk is higher per km than a regular driver.

PS I’m also with AXA for a relatively simple Hausrat & Privathaftpficht. Prices very similar adjusting for my conditions. Definitely forget the Reise-Gepäckversicherung.

Huge deductible = less Prämie.

Like with Krankenkasse and other insurances only insure the big risks which could break your back.

(Unless u know you are sick regularly or have your house broken into twice a year.)

I am aware of that, I was just wondering that in case you ever need to make use of the hausrat, you would have a major event, eg. a fire and you loose everything.

Thats the reason I have Hausrat. having a huge deductible here doesn’t make sense, if the premiums are only 50-100chf cheaper

I believe that exactly in the big events is where the deductible does not matter. Take the case you described. Your sum insured is 100’000 (Costs of all the contents of your households) and everything gets burned. Then you receive “only” 95’000. Are the missing 5’000 really a problem? If they are, then you can put voluntarily you sum insured to 105’000 (will heave nearly no effect to the premium) and in case you have a 100% damage you receive 100’000.

Where you are right is that in case you have a damage of 10’000 you will receive only 5’000. This could be a problem. But on the other side you save a lot of the yearly premium.

I believe what is more important is to have a realistic sum insured of you household contents. Because here you could underestimate your stuff by a lot! You could think you have only 100’000 when in reality you have 150’000. And the missing 50’000 could be a problem.

Also a wrong sum insured has an impact if you have smaller damages. Take the example from before (Sum insurend 100’000. Real household sum 150’000): if you have a damage of 15’000 the insurer will cover only the 10’000 because of the wrong sum insured (if he founs out). And on the 10’000 will also be reduced with the deductible.

Thank you to everyone who chimed in, I’m very grateful for learning so much here.

I know it’s a bit late if you already signed, but since you want to go with AXA did you check their website? There is also a BASIC product which is not really worse in Private liability - just cheaper.

By the way this is a 5 year contract - did you notice?

Haven’t signed yet

I went on the AXA website, I didn’t notice that it is a 5 year contract. Are these problematic?

From the AXA website: 5 years, can be terminated each year (during the first year, personal liability coverage is free for persons up to the age of 30)

I want to include the third party vehicles, hence I’ll take the optima version.

I’m moving back in to my parents in January 2019, so I have to change the policy again then. Is this problematic? I’ll call our insurance guy to ask him this as well.

Regarding deductible: The deductible is 500.- for 3rd party cars and 200.- for other private liability claims. If I were to move the deductible to 500.- for other private liability claims, the yearly policy would be reduced by around 20.-. I guess it doesn’t matter in the first year as it’s free but afterwards it might be important.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.