Any source for this change in fees? I did not receive any communication.

I am on the family package which is also free for everyone

Any source for this change in fees? I did not receive any communication.

I am on the family package which is also free for everyone

Having a look at their website, I was able to find the new october 2021 conditions, available here. I only found the french documentation, as the english one is dated to july 2021, but the two versions can be used to check the exact term differences.

Here are the updated terms (in french, sorry) :

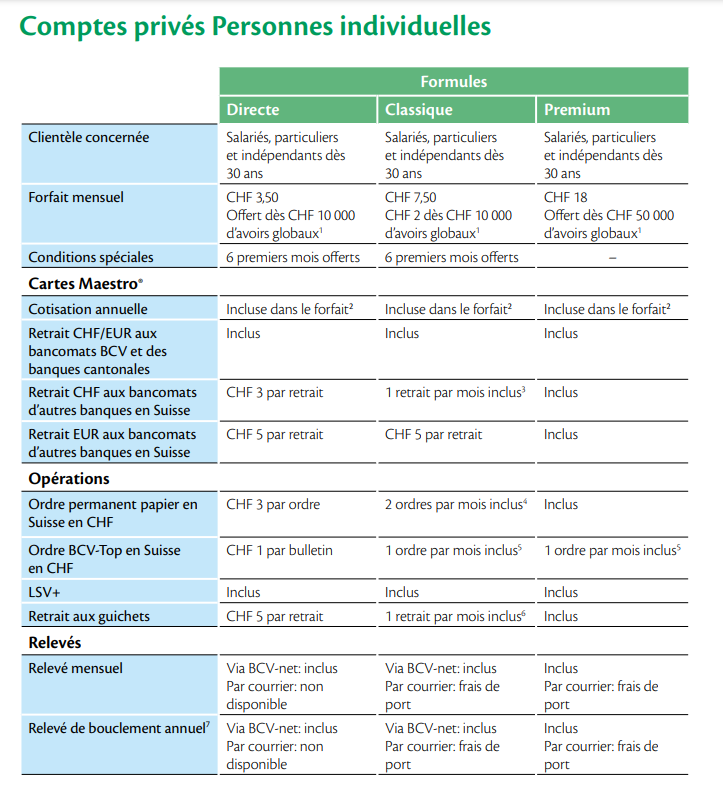

If you take a look at the 6th page, you can see that there are 3 formulas, the first two with monthly fee reductions starting at 10’000 chf, and the last one at 50’000 chf.

What’s interesting is that the major difference between the first two formulas lie on the fact that the first one is free with the reduction, whereas the second one costs those 2.- chf monthly as stated throughout the thread.

Their differences in services are also not that significative, for the 2.- chf per month, you get a free CHF withdrawal at any swiss ATM, a couple of free fancy order types, as well as a free in-person withdrawal at any branch.

To me, those benefits are pretty much useless, as such, I would end up with first formula if I didn’t already held a youth campus account, with waives the fees regardless.

If you are looking at parking 50’000 chf in BCV for any reason, and care about the fancy benefits of the second formula, I guess it could make sense to go with the third formula if the costs of the fancy benefits outweigh the potential opportunity cost of parking 50’000 chf in a bank account.

Regarding family packages, there were no differences, with the fees still being waived if above 15’000 in assets with the Direct package, and still 10 chf for the Classic package

As such, to answer the thread question “Free alternative to BCV”… my answer will be BCV, but with the Direct formula, rather than the Classic.

NB : it seems like the active youth formula in page 10 got the same treatment, with 2.- chf monthly fee if above 10’000 in assets held, rather than a waived fee

I asked BCV about negative interest rates. They told me they would apply negative interest above CHF 100k if I dont invest this money (Just parking cssh).

I don’t think that’s too far fetched. My wife and me with our dog come close to this, but only if we go on vacation (which we don’t do at the moment, only some short, cheap trips in Switzerland).

It depends heavily on what you can pay with the credit card. The only items we can’t pay with credit card are rent, utility bills, car service and insurances. We can even pay the vet bills with credit card.

Ok, you are right, I just checked our spendings with credit card for 2021, and the average per month is only 1’600 incl. flight to and hotel in Italy for 1 week (2’000). I totally understimated how much of our total spending is coming from rent, utility bills and insurances.

And we are not that mustachian to be honest.

Little and late feedback for those of you who are interested : I actually changed my account to the “formule directe” (thanks, Capito27!), and at the price of not being able to withdraw from all swiss ATM (actually I don’t care), my account will be free again, forever until the next BCV decision

Very interesting and philosophical discussion, anyways

Do TradeDirect assets qualify for the fee waiver on their current account products?

They should, shouldn’t they?

Zuger Kantonalbank seems to have a new product, also completely free. However you do not get a real debit card, only virtual: https://www.zugerkb.ch/private/zahlen-und-sparen/konto-sets/konto-set-fix

What languages are supported by ZugerKB as well as in their applications?

I assume German, but what about English and French?

I don‘t know but I‘d advise against getting this „offer“ from Zuger KB.

Their eBanking and mobile banking apps are from the stone age! AFAIK outgoing payments need to be verified in another app (Cronto Sign) - not sure if you can sign payments in the mobile app.

I called their customer service and they have not planned any noteworthy modernisation except for decoupling their mobile banking from their ebanking somewhen in 2023. Just check the ratings in the App Store — Zuger KB doesn‘t even bother replying to valid criticism.

So Zuger KB launched a digital only offering while not being digitally competent. ![]()

If you are masochistic or you want to time travel back to 2012, sure, go for it. ![]()

So do they need to be with, for example, UBS.

I‘ve used Crontosign with other banks, and it seems a solid and reasonably secure 2nd-factor authentication method. Not saying that ZGKB‘s online/app banking is any good (I don‘t know) - but I wouldn’t blame CrontoSign for it.

Edit: couldn’t open ZGKB online fix because my passport is too new ![]()

Agree. I would be more worried if they would not use it… If you use eBanking on PC that’s the only reasonable way to have a good and easy 2FA (just take a photo of that fancy QR code).

And on your smartphone (which you can secure with biometrics) it’s not required or even possible… because how do you take a photo of your own screen, and what sense would that have since it’s on the same device?

Thank you for sharing this.

People are nowadays not willing to pay for a service; imagine not being paid for your work.

I tried BCV once as well (was looking as well for a „free“ alternative). Their e-banking is very bad in my opinion, compared to to one from UBS or Zürcher Kantonalbank.

I switched back and will happily contribute to very good service. Not everyting can be replaced with free alternative. And if it‘s fee, they make money on another way (higher spreads when trading, selling your data, higher marks on FX changes, etc.).

I totally support this opinion. Free rarely rhymes with quality. And on the other hand, the situation can change much more quickly in an unfavorable way when something is free, with a significant increase in rates or a drastic decrease in benefits (wink to the Crypto.com card).

Banks earn money with your money, and affiliated services as you mention… this especially also in these days when interest rates are rising again. This by the way is the reason why normally bank accounts in Switzerland have been free of charge already since a long time (at least). So, I don’t think there is the need to critizise people who are not willing to pay for a bank account.

And by the way: I don’t complain about a bad e-banking if it’s free.

Agree on your point of view