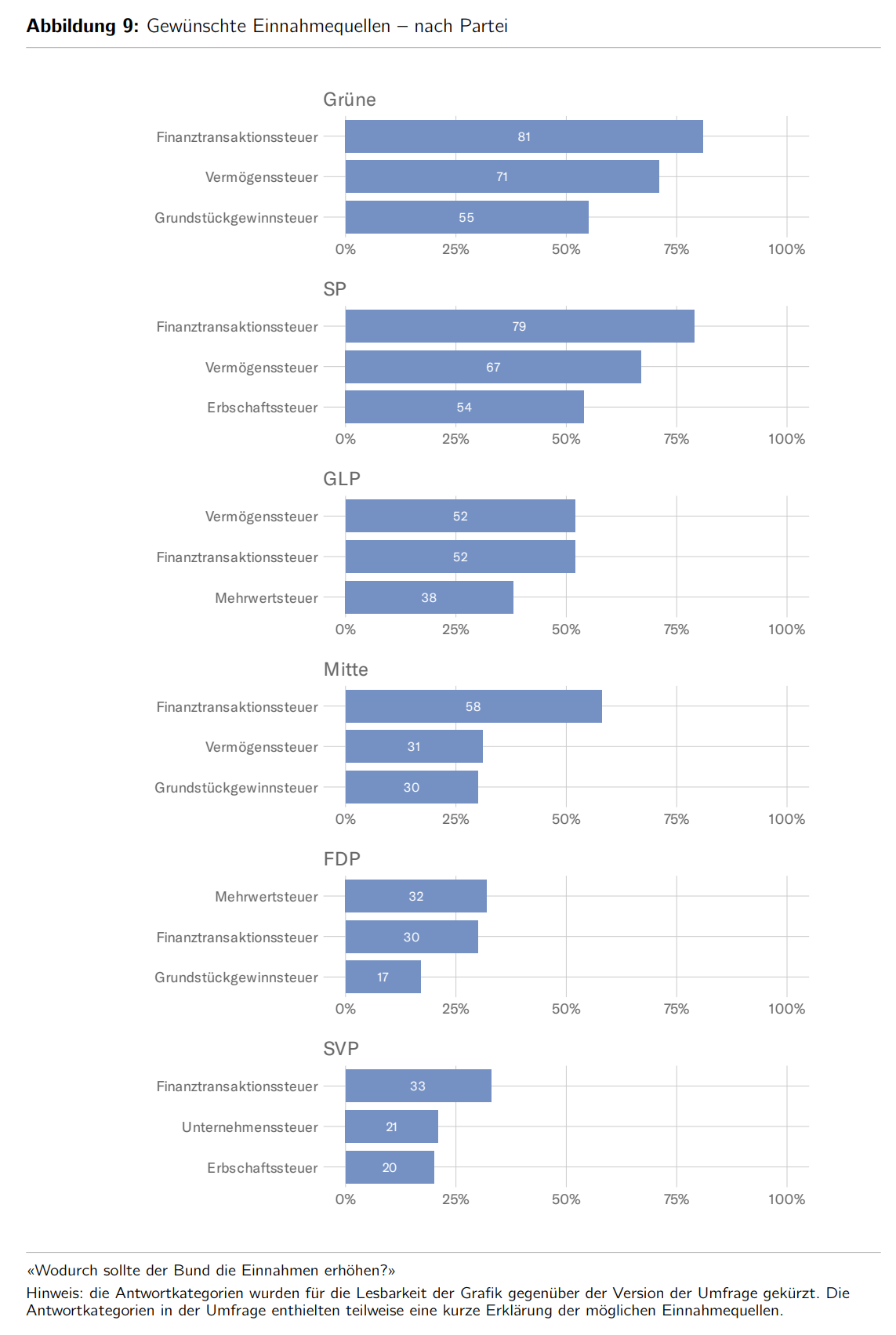

It’s surprising to me that across party lines people have the financial transaction tax in the top three of desired measures to generate more income at the federal level. Again from the sotomo study:

This could tempt say, the SP and the Greens to launch an initiative to introduce such a tax as they could hope for votes even from the SVP.

Just a gut feeling, but I believe “the people” just in general are suspicious of banks, the “finance industry” etc. and recent events like Credit Suisse f-ing up and UBS buying them very cheaply while risks were “externalized” to Switzerland (i.e. tax payers) didn’t help with this.

The people might want to “stick it to the man” without realizing they’re probably taking a shot at their own foot.

This documents the recent decision by the federal council why they don’t want to introduce further financial transaction taxes and lists the ones that were proposed in 2021 by but rejected on Oct 9 2024:

Finanztransaktionssteuern können namentlich auf Wertschriftentransaktionen (Emission und Handel von Wertschriften), auf Kredit- und Einlagetransaktionen im Zinsdifferenzgeschäft der Banken und auf Devisentransaktionen erhoben werden. Die Schweiz kennt mit der Emissions- und der Umsatzabgabe bereits heute zwei Finanztransaktionssteuern

Edit:

I doubt, though, that the average voter will ask your question what the Finanztransaktionssteuer actually is (and I would also claim that the average participant in the referenced sotomo study did not ask the question).

I think in the average voters mind it’s a tax “that financial institutions and the bankers making the big money” will pay. Hence the broad support across party lines to introduce such a tax.

It’s interesting how everyone goes after banks and financial institutions without thinking too much in detail.

Anyways thanks for sharing the data

It’s interesting how people react to various things and how difficult the job of politicians actually is to make reforms

The Swiss Federal Council is planning to increase taxes on withdrawals from pension funds and private retirement accounts (Pillar 3a), sparking significant debate. Experts and financial planners are advocating for a reform in how pension funds are taxed, proposing a unified, one-time taxation system for pension capital.

Key Points:

Proposed Tax Changes: Currently, pension withdrawals are taxed at a lower, privileged rate separate from regular income. The Federal Council’s proposal would eliminate this advantage, potentially discouraging savings in Pillar 3a and pension funds.

Rising Capital Withdrawals: Many retirees prefer withdrawing their pension funds as a lump sum rather than receiving a lifetime annuity, partly due to tax benefits. Capital withdrawals rose from CHF 6.3 billion in 2015 to CHF 14.8 billion in 2023.

Expert Proposal: Specialists Reto Spring and Reto Leibundgut suggest a one-time, flat tax on pension capital (e.g., 10%) upon retirement. This tax would simplify the system, eliminate regional differences, and prevent loopholes for high earners.

Simplification Benefits: Under this system, remaining funds would be tax-free, whether taken as a lump sum, annuity, or a combination. This would level the playing field, reduce tax-related mismanagement, and lower retirees’ tax burdens.

Challenges: Critics argue that the transition could lead to a rush to exploit the old system’s benefits. Additionally, low-tax cantons might lose out under the proposed changes.

Potential Impacts: The reform could make lifetime annuities more attractive again, ensuring retirees have stable, lifelong income. It also aligns with constitutional requirements to provide adequate retirement income.

Supporters of the reform believe it would simplify taxation, promote fair treatment across income groups, and reduce the risk of retirees exhausting their savings prematurely. However, opposition may arise from financial advisors whose business models rely on promoting capital withdrawals over annuities.

A flat tax would be beneficial for people with a big pillar 2/3a, no?

I don’t understand the “simplification benefits”: what exactly would be tax-free? No wealth tax for withdrawn pillar 3a and pilla 2 lump-sum? No income tax on pillar 2 pensions?

Yes, no progressive tax on capital withdrawal is how I read the proposal. Once withdrawn, it would be taxed as wealth – I don’t see anything stated that says otherwise. And yes, no income tax on pillar 2 pension.

They really are continuing to try to sabotage the pillars.

I will continue to not pay into 3a and limit 2nd pillar as much s possible. Really annoying that my company doubled our minimum plan and I now have to pay a lot more into 2nd pillar….

remaining funds would be tax-free, whether taken as a lump sum, annuity, or a combination

Say I take pillar 2 as lump sum, like they describe here. What exactly is tax-free then?

After reading multiple times I think what this means is following

it doesn’t matter how much you withdraw and how long you keep withdrawing, the tax would be same rate , let’s say X%

let’s assume withdrawal amount is Y CHF. Person would pay X% to government and then Y(1-X%) wouldn’t attract any income tax for that financial year. Currently annuity attract income tax.

Above points would nullify the advantage of capital withdrawals (at least from federal tax perspective)

Assuming X% only refers to Federal. Most likely this is average of currently applied Federal income tax on annuities & Federal lump sum tax on capital withdrawals

However if X% includes cantonal then it cannot be 10% for sure. It would be higher number

The way I understand it: you have a million in your pillar 2.

You withdraw it, 10% is taken away as tax. You’re left with 900’000.

You decide to take the annuity, let’s say 50’000 per year. You pay 10% of the 50’000 as tax, i.e. 5’000.

It’s probably important to understand that this proposal is only input into the discussion of what should get implemented which will ultimately be discussed and decided by parliament.

Other lobbying proposals will likely take place, both publicly and privately. The article hints at this as e.g. some financial advisors might be overly interested in keeping the capital withdrawal option as favorable as possible (regardless of whether it makes sense for the newly minted pensioner) as they might get to manage the withdrawn lumpsum with nice fees … and the risk of that capital not being sufficient until the pensioner’s exit is nicely externalized to society.

Anyhow, let’s not get too political …

Some mild confusion here - taking a step back to see a bit better (maybe😉).

It hasn’t been highlighted enough IMO, that this proposal discussed in the NZZ yesterday by “Specialists Reto Spring and Reto Leibundgut suggest a one-time, flat tax on pension capital (e.g., 10%) upon retirement.”, comes from the Finanzplaner Verband, exactly the lobbyists who want to prevent Kapitalbezüge becoming less attractive!

Also a progressive tax is not in their “rich clients” interest.

NZZ a pro-capitalist newspaper of course likes to present this side.

It has nothing to do with what the government experts and Bundesrat wants.

IIRC, the Expertenkommission, whose proposal was more complicated and discussed further up in this thread (if I may put it very simply = % tax based on your current salary at time of Kapitalbezug) on the other hand was led by Serge Gaillard, who was a member of the Marxist League in his student days. Us older folk know that our opinions can change from the opinions we had way back at Uni, but still this can give an indication of the direction the Expertenkommission went for their proposal.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.