The Bundesrat have sent their proposal to Vernehmlassung (to get voted on by parliament), for new tax regime for 3rd pillar withdrawals.

(it is not clear to me from the text as to whether this proposal also covers the 2nd pillar withdrawals)

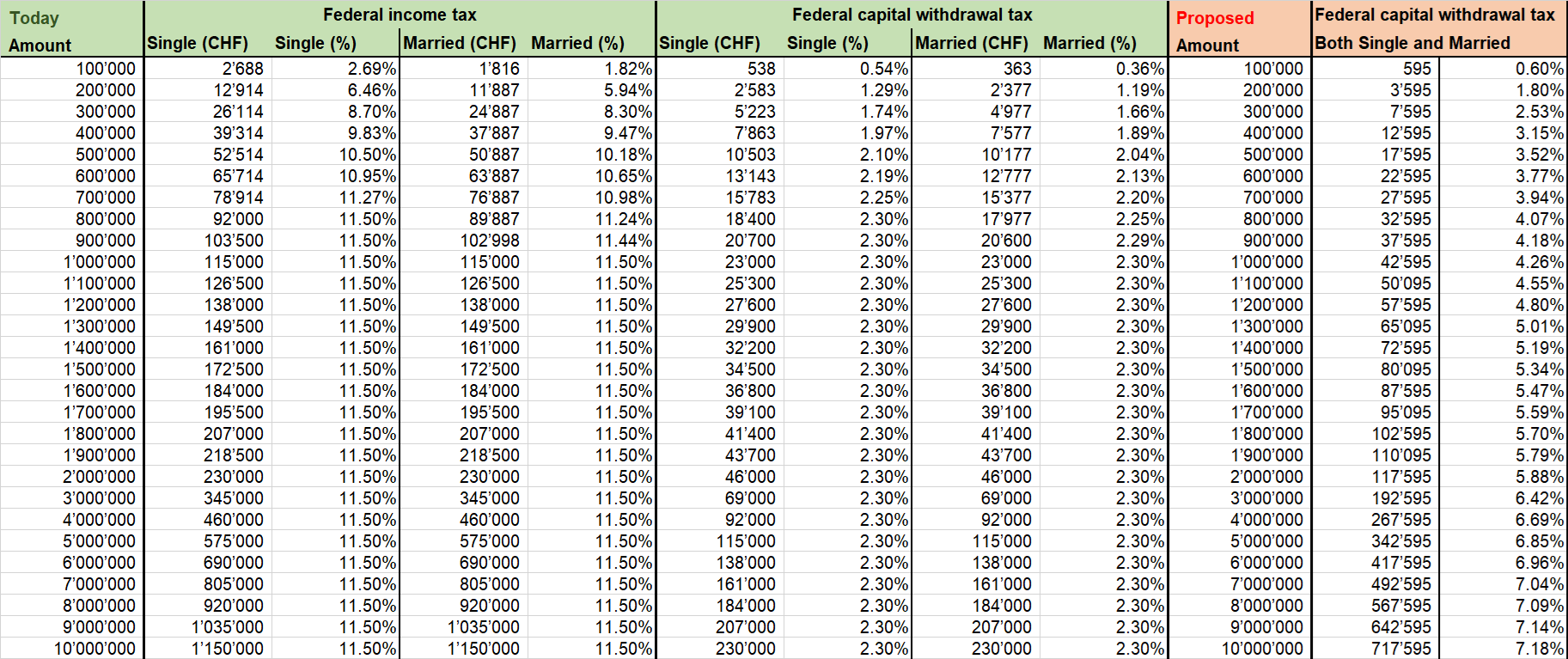

Up to 100k 0.1 to 1%

Till 250k = 3%, then climbs more steeply than before.

The gestaffelter Bezug still is allowed, so that I suppose middle-class Bezüge of 3a, gestaffelt, would not be taxed above 1%.

source https://www.blick.ch/politik/bundesrat-gibt-ein-wenig-nach-doch-nicht-so-hohe-steuern-beim-bezug-der-3-saeule-id20539769.html

Am Mittwoch hat der Bundesrat seine definitiven Sparpläne in die Vernehmlassung geschickt. Und er ist nochmals über die Bücher gegangen. Zwar sollen die Kapitalbezüge höher besteuert werden. Der Bundesrat will damit immer noch pro Jahr 200 Millionen Franken mehr einnehmen, aber nicht 280 wie zuvor angekündigt. Das Alterssparen während des Erwerbslebens soll nämlich wie bisher durch Steuerprivilegien gefördert werden. Insbesondere tiefe Bezüge, wie sie für die Säule 3a typisch sind, werden weiterhin zu sehr gemässigten Sätzen besteuert. Umgesetzt werden soll dies über einen neuen progressiven Spezialtarif, der die bisherigen Tarife ablöst.

Mildere Steuersätze

Die Grenzsteuersätze sollen mit Sätzen von 0,1 bis 1,0 Prozent bis zu einem Kapitalleistungsbetrag von 100’000 Franken milde ausgestaltet sein, schreibt der Bund. Oberhalb dieser Schwelle sollen sie zunächst auf 3 Prozent, oberhalb von 250’000 Franken auf 5 Prozent zunehmen, oberhalb von 1 Million Franken auf 7,5 Prozent und oberhalb von 10 Millionen Franken auf 11,5 Prozent.

Das Beispiel: Ein Ehepaar, bei dem ein Ehepartner 100’000 Franken Kapital bezieht, würde statt heute 372 künftig 595 Franken bezahlen. Eine alleinstehende Person, die 1 Millionen Franken bezieht, würde rund 42’600 statt 23’000 Franken zahlen.

«Diese Tarifgestaltung hat zur Folge, dass die typischerweise tieferen Bezüge aus der Säule 3a weiterhin zu sehr gemässigten Sätzen besteuert werden. Dies gilt selbst für grössere Guthaben, sofern diese gestaffelt auf mehrere Jahre verteilt bezogen werden können», schreibt der Bundesrat. Somit trifft die Reform vor allem grössere Kapitalbezüge aus der 2. Säule und in einem deutlich geringeren Ausmass Kapitalbezüge von Selbständigerwerbenden ohne Pensionskasse, bei denen die Säule 3a Ersatz für die fehlende 2. Säule ist.