Honest question (because I am also considering adding it to my portfolio):

What would you suggest as a good small-cap value ETF?

Getting the world covered (vs. just US) might get expensive.

PS but we get quite offtopic here, this should go to some Value thread.

Value and small caps are factors with a higher expected return. The most probably reason why they are cheap is that an investment in such companies carries a higher risk that compensated with higher returns.

The higher return is usually driven by a very small subset of companies, so diversification is key and the reason why you should have at least a few hundred companies with the desired factor.

Here you find a good whitepaper about factor investing.

I see no compelling reason to overweight small caps, be it growth or value over large caps. As it is, both value AND small cap are currently underperforming.

Changing your allocation does not trigger any tax events comparing to most other countries, so there is no reason sticking to a losing strategy hoping it will once turn around. You can always start doing it once it actually starts working.

If there was an easy recipe for outperformance, it would be the norm.

There have always been periods of time were the market underperformed the risk free rate. The same happens to size and value factors.

Since the release of the fama french 3 factor model in 1991, US small cap value has outperformed US market by 0.33% per month. Here is the paper that looks how the premiums have done since the relase of the 1991 paper.

Well I did link to a comparison of World and Small Cap World indices.

Well, I’m not saying for the first time on this forum… but the U.S. is just one single country.

From that, I think, it’s a pretty sweeping generalisation to say that small caps have underperformed over the last 10 years. Especially in the context of this thread, where runner’s (in his post that you replied to) explicitly brought up the idea of overweighting international small caps.

Very true - my mistake on that - sorry.

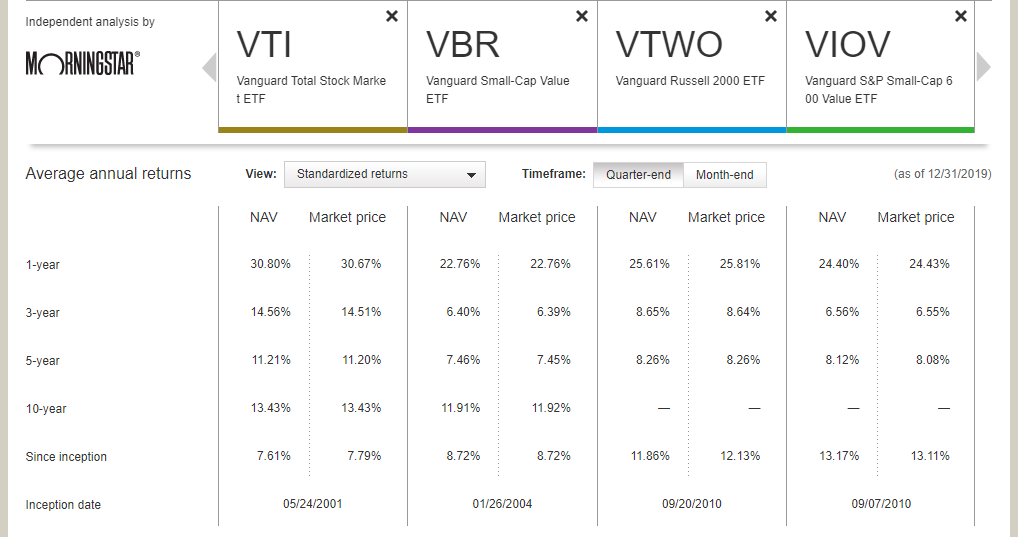

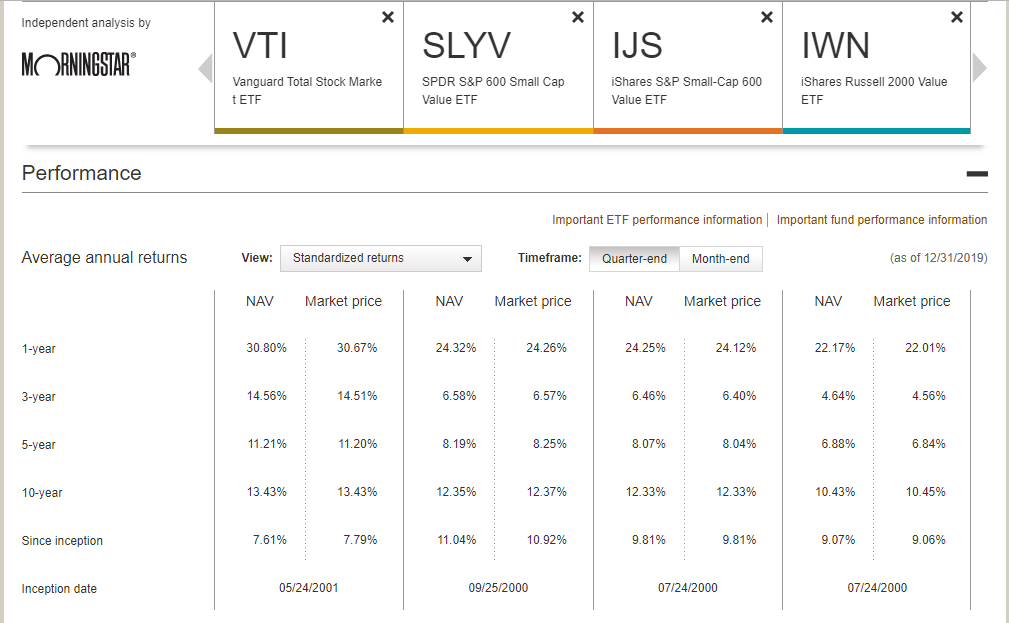

You are right that across the world ex-US, small cap value has outperformed market-cap-weighted index over the longer run (5/10+ yrs).

But you do want to beat the index, don’t you? There is no free lunch.

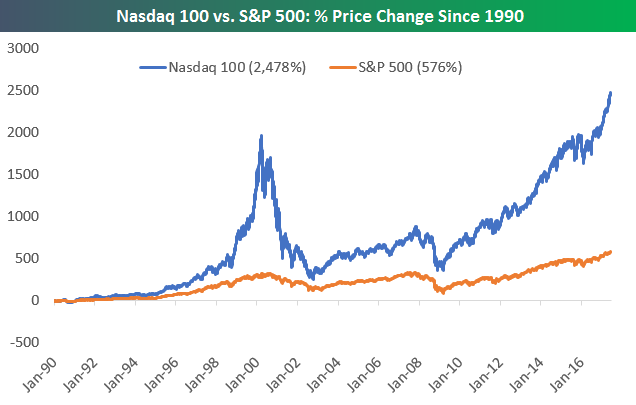

BTW the difference in valuations of Nasdaq 100 vs S&P 500 is nowhere close to where it was during the dotcom bubble. It is only 13% higher as a matter of fact (P/Es are ~29 and ~25 respectively). It was 233% higher (P/E of 80 vs 24) during the dotcom bubble, and the interest rates in the US were around 6% back then.

HML/value and SMB/size are 2 researched and confirmed factors that explain outperformance (with of course increased risk) - in general historically and of a few successful well-known active investors.

Nasdaq100 (or QQQ ETF) is a weird mix picking top 100 largest companies whilst applying filters like excluding nonfinancials and other sectors, market cap reweighting etc. - seems quite arbitrary to me.

I want to have at least some theoretical (with empirical evidence) explanation I agree with behind my decisions.

I agree a one-sweep ETF might not be best to address the above, but there is always a tradeoff between effort/knowledge/time needed - value gained.

But I suggest we fork this “value” discussion elsewhere, doesn’t belong much into “VTI vs VT” topic.

QQQ is indeed very narrow. VGT is far better. You can also go with MSCI World Technology when looking for proof. But is any proof needed really? Growth and development is driven by technology and I don’t see how that could reverse any time soon.

Make up your mind then. If it is priced in, then it could only mean that higher valuations are offset by higher expected growth. No other way around it.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.