haha gives great incentitive to quickly save the remaining 30k ![]()

but yes, its it seriously that cheap? minimum is 0.35$, up to 100 shares?

haha gives great incentitive to quickly save the remaining 30k ![]()

but yes, its it seriously that cheap? minimum is 0.35$, up to 100 shares?

Yes it’s that cheap in the US. You’re missing exchange’s fees which will vary depending on exactly how the order gets executed, but they are a similarly small amount, sometimes even negative, e.g. BATS pays you for removing liquidity. And 2-3 bucks per currency conversion

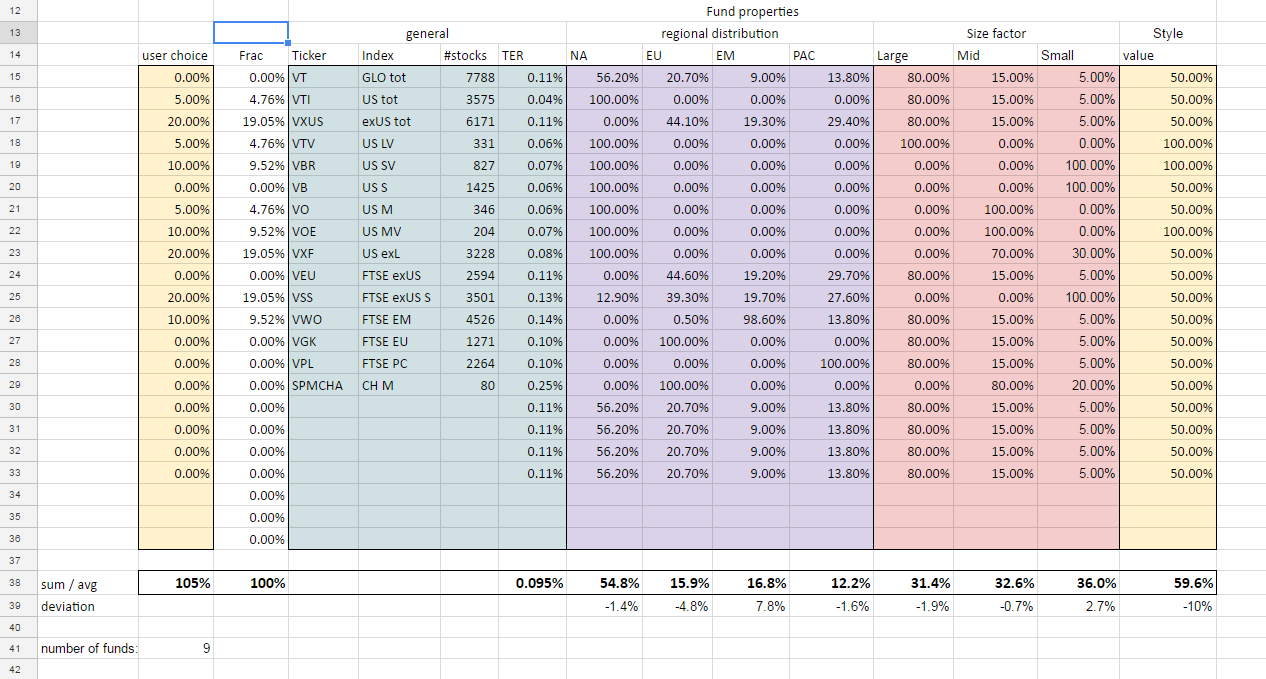

in case i move to IB soon, i made myself a stock portfolio selector to cope with the freedom of purchasing low cost vanguard funds.

Its main purpose is to find a portfolio that suits my idea of

go ahead an make yourself a copy of the sheet ![]()

the current numbers are only my first guess, i might refin it later. comments & ideas for extension welcome ![]()

flaws:

Why go into so much trouble with a dozen of funds? Simplicity is best. I’d focus the rest of energy on asset allocation for other asset classes - equity is not everything, or maybe stock picking for higher return or polishing defensive characteristics of portfolio

I’m perfectly happy at the moment with just two funds for global passively indexed equity: VTI for US and VEA for exUS developed. You can throw in VWO into the mix for EM if you really want (or just go with VT as a one fund solution). Low cost, a bit even cheaper than VT, and highly liquid. You can swap into IE based funds for ex-US portion anytime if you find a reason to do it (such as maybe due to being strictly taxed at sourced only).

Totally agree. Simplicity + diversification = VT.

because i can. i dont regard it as trouble. simplicity is good but no hard reason in this regard.

The IE vs. US domicilation is something i need to get into, indeed. or stuff like VEU vs VXUS. or VWO. if i find the time i will write a guide about it and post it here… which i again recommend to anybody contributing to this forum in the past months. all that valuable information posted is pretty much lost to later users unless systematically summarized, as hardly anybody will crawl old threads.

I’m also planning to diversify more against more ETF funds (and more asset classes) - but not during accumulation phase of my life, but rather later - during preservation of capital phase of my life. I don’t want to slow down my race to FI.

i did, and the resul is this post

summarizing: funds containing mostly US domiciled assets are better bough in their US domiciled version (vanguard…) and funds with more ex-US assets (EM-funds, exUS funds) in their IE domiciled version. at least from taxation point of view, wich should always be only one out of several aspects to guide decision.