I’m recently flirting with the idea of getting a Lombard loan of 100k CHF. The expected rate is around 1-1.5% (I am planning to schedule a consultation to get an accurate rate)

The idea is to invest this amount through crowdhouse with an expected return 4-5%. Basically I will be getting a yearly ~3% return on this 100k CHF and probably some tax benefits because of the interest rate.

Of course a much riskier endeavor would be to get the lombard loan and invest it in the markets as a leverage but I don’t think that I would be able to sleep during a market crash in that case.

Do you think its a good idea? What are the hidden risks that I may be completely missing? I have enough cash reserve to increase my portfolio in case of a market crash and support the Lombard loan.

What makes it a good idea or a bad idea are the terms of the Lombard loan. Under which conditions is it callable? Is the interest rate fixed? Are you amortizing it?

If it’s simply an Interactive Brokers loan, it’s callable if the value of the shares falls by a certain amount. If you have 1 milion invested, then there are very small chances that you’ll reach the threshold for a 100k loan; therefore it’s rather safe. But if you have 200k invested, it becomes more dangerous. For the interest rates, IB can change them at will. EDIT: IB can also change the conditions under which loans are callable. In case of large market volatility, it might make its lending conditions more stringent and trigger a margin call at the worst possible time for you. If the money is invested in Crowdhouse, then it’s not very liquid so you won’t be able to cover in time.

To me, that’s a lot of risks for only getting 3000 CHF per year. Does this money really make a difference for you? Does it significantly speed up your “getting retired” process? I mean, if you’re already saving and investing 30k per year, you will get there soon enough so why take the additional risk?

But if the loan provider offers different conditions, then it might be worth considering.

I think the deciding factor is the ratio of the lombard loan against your total collateral. If you have 300k worth of stocks and you use say, 135,000 of that to collateralize a 100k lombard loan, I would personally consider that a very low risk. Even more so if you have additional cash/assets. Doing this could also possibly save you some taxes AFAIK.

I just scanned Crowdhouse website - you would own a partial share of a property and not control it? I have done this before and it was a lot of hassle and stress and was happy to get out. Be very careful / avoid. Watch outs:

How do the experts selling you this make their money and do they have any skin in the game? Often they get a commission on the sale and % of rent management fee so guaranteed income, you carry all the risk.

How realistic is the rental forecast and costs, and estimate of vacancies? Real estate agents tend to make pretty optimisitic forecasts as it is in their interest to do so

What is your exit strategy if the property is not managed well or doesn’t perform? The market for buying a % of a building is not big, you will probably be limited to other clients of Crowdhouse

I’m curious about this statement. If you have significant cash reserves, why not invest those? If they are meant as emergency fund, why not draw on a margin loan if/when it is necessary and only pay the loan interest for that time?

Ultimately it is about risk management & tolerance, isn’t it. I’m not sure if it makes sense to maintain cash/bonds to reduce risk on one side, and then pay interest for a loan and leverage on the other. Some cash for immediate liquidity is a good thing of course, but transferring money back from IB (if that is where you are) doesn’t take all that long either. The one time I transferred money back from IB it was available in the CH account the next day - but of course your mileage may vary, especially when transferring large sums or falling foul on some due diligence algo tripping up.

Is the rate fixed ? if not you also face the risk of a sudden increase in interest rates thereby reducing the profit on this deal.

It’s important to note that Crowdhouse deals are themselves already leveraged as the deal includes a fixed rate mortgage in its structure so if you invest 100k your actual exposure is higher than this, I would say 200 k as in general they borrow for half of the property.

The Crowdhouse business only works as long as the interest rates remain low and the real estate market keeps increasing. If you study their simulation you should try to evaluate the return in case the mortgage interest rate suddenly costs twice what it costs when the deal is closed and some issues arise when it comes to finding tenants because (those properties are usually located in cities in AG, SG or other kantons that are less attractive than ZH). Also one important aspect is that you only own part of the property and that’s for sure less liquid than owning a property on your own, not to mention that you rely on people you do not know to make decisions.

To be honest the only entity earning a lot in this is Crowdhouse itself and that without any exposure:

- They first milk people when the deal is closed as they charge a closure fee of 3% of the property value.

- As the property is rented they take care of the management and also take juicy fees to do that.

If you really want yield through leverage investing in a diversified portfolio (i.e. accross different sectors like residential, medical, logistics etc.) of REITs or SCPI (French product) that yield 4 to 5 % could be a better option I guess.

Disclaimer: I’ve always been skeptical about the crowdhouse model and until now I’ve been proven wrong because of the low interest rate environment but those risks I mention here are real and not to be ignored…

Would you invest 100k of your own cash in Crowdhouse?

I mean, why talk us through all the hoopla of taking out a (low-interest) loan to do it? You’ve basically established yourself that and how you are going to keep that loan above water with your cash reserve. So does the origin of funds matter? Does taking out a loan make it a better - or worse - investment?

Attempting to answer the question:

No, I doesn’t sound that great of an idea to me. I’d fear that investment is illiquid - and since you don’t control the management of the property, I’d fear hidden costs. As described here.

Attempting to pre-empt the inevitable follow-up question on this forum:

Will you be considered a professional investor by taking out a loan to fund investments?

First of all thanks a lot everyone for taking the time to reply and provide such good arguments and many food for thought and further research.

I’m working and investing (it’s mandatory) with one of the big banks in Switzerland so no IB for me. The advantage with that is that I can get some good staff benefits like 1% less in the Lombard loan compared to a regular client.

You all raised some very good points about the specific conditions, duration and rate that I can’t answer. I will schedule a consultation for the Lombard loan to get some more concrete facts on that.

I have currently a cash reserve of around 90k that I want to push in the market but the current valuations make me uncomfortable to do it. Therefore if the market crashes and I need to further support the Lombard loan I will buy in the market, something that I would have done anyway. If I invest those, I won’t have enough cash on the side to buy in any sudden market drop. I know this brings us to another big topic that has already been discussed extensively in this forum and in the end for me it’s just about psychology and emotions, I simply don’t feel comfortable dropping that amount in the market with the current valuation.

The way I ended up with this amount of cash is by not investing at all during my first year in Switzerland (2016) and the later years investing only about 3k per month while I had savings of around 5k per month. I pushed some amounts during the flash crash last year (I know I should have invested all of them), but cash has accumulated again…

The way I see it (or at least did in the past, lots of food for thought in this topic) is that the Crowdhouse investment is a safe one and the only risk is on the Lombard loan that I would have covered with cash anyway in a case of market drop.

Thanks a lot for the post it is very illuminating! Of course I would expect to have some of these fees as a part of the deal, since essentially it’s about completely outsourcing the hassle of owning and managing real estate but still get a piece of the real estate returns in Switzerland. Some of the fees seem kind of absurd, thanks again for the article

That was and still remains my biggest concern with the whole idea. The crowdhouse investment seems quite illiquid, they have a secondary market but I don’t think it has enough participants.

I did not know about the SCPI, I will definitely research it more it seems like a good alternative to crowdhouse.

Regarding REITs my only experience so far is quite mixed with the APLE Reit (hotels and US based). I got some at ~15$ and watched it drop to 5$ during March last year, fortunately bought some more at the bottom having an average price of 9.8$ with current price back to 15.55$. But in my experience so far it’s just too volatile. I suppose other REITs that focus on residential properties would be much more stable.

My point would be to avoid REITS for residential property only. Best to diversify.

Also in downturn period I expect non-commercial properties to do better. If you are renting space for manufacturing or cultivating, tenants will not leave until force to or going bankruptcy

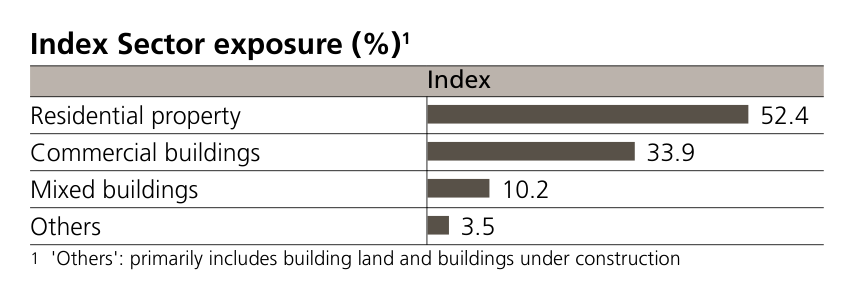

I think swiss real estate funds are a good investment, but I would not buy the index. Some funds are way too expensive. I would select the funds individually, so that it would match the percentage of commercial properties I want and so that I would not overpay for a fund. What’s more, the tax treatments of the fund is different if it holds the buildings directly or indirectly and one might want to only buy funds with a special tax treatments depending on his situation.

Just be careful and not too trusting. My experience with real estate transactions in CH is caveat emptor is assumed by all parties in the chain and it is the place in business which is least transparent and where most “helping buddies” occurs. Don’t assume that because you are in CH Crowdhouse or even the bank will behave “correctly” or with respect of your best interests.

CrowdHouse does for you what you couldn’t do yourself. Picks the property out of an ocean of overpriced ones, does a perfectly transparent job with the paperwork and pays everything on time (so far, it might be a ponzi scheme fwiw).

Having notary etc. fees while buying a property is not something you can avoid. Also having an agency manage your property is not something you can avoid. They might skim 1-2% off the top for a fire-and-forget investment and I’d say let them have it. They manage the tenants, the rental contracts, and all the paperwork for this fee so you can sleep relaxed. Also they let you diversify your portfolio in a way you like it with less money than what you would need otherwise.

You are running the same risk/benefit scope with real estate as everyone else who has bought property. All of those people are also leveraged by nature of these things.

That said, I’m positive for CrowdHouse (and co-own some properties through them), but I’d probably not mix this with a lombard loan which has stocks as collateral - sounds like a deal made in hell. Has the high risk of a market crash but the low payout rate of real estate… And you need to constantly pay to finance it with no interest lock-in like with property.

Is that really worth 3% extra income?

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.

Would you invest 100k of your own cash in Crowdhouse?

Would you invest 100k of your own cash in Crowdhouse? by taking out a loan to fund investments?

by taking out a loan to fund investments?