Hello all,

I saw this mentioned in a couple of threads, so I wanted to inquire about your experiences.

Crowdhouse

How do you find it, if you used it?

Would you recommend it as a REIT investment option?

Hello all,

I saw this mentioned in a couple of threads, so I wanted to inquire about your experiences.

Crowdhouse

How do you find it, if you used it?

Would you recommend it as a REIT investment option?

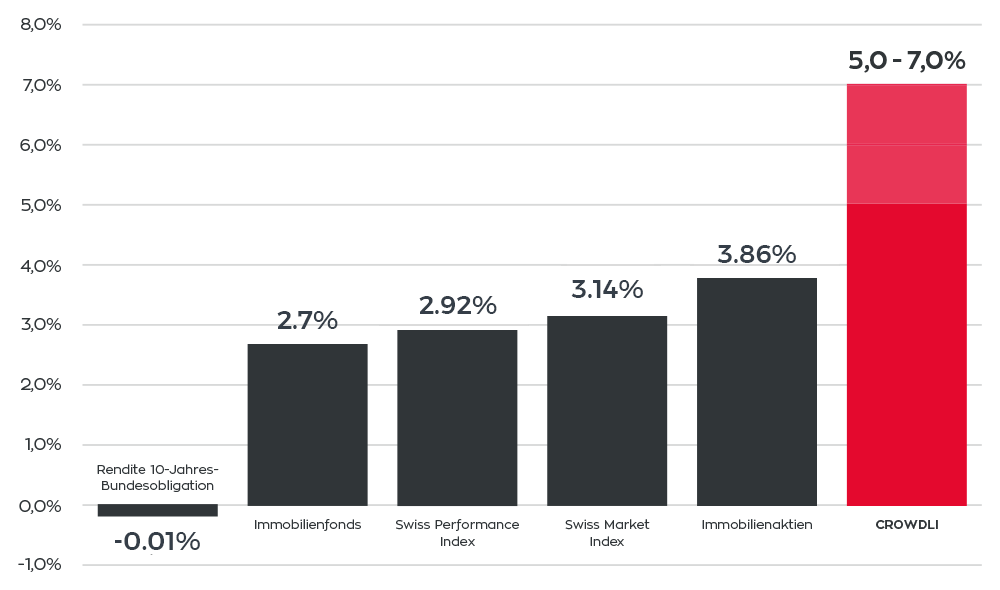

Another option would be https://crowdli.ch – the min. investment sum (25’000 CHF) is smaller than with crowdhouse.

My first feeling is that it seems oversold.

How can you expect 6% return on investment on housing in Switzerland when most immofunds are barely at 4% and even pension founds threw their hardly earned cash in investment with 2% return. (Still better than -0.75% by SNB).

The 6% return on investment (roi) is probably without renovation, insurance, real estate tax, administration fees and depreciation due to ageing of the building.

The picture they give is only for the dividend paid but not for increase in value.

The last point is the legal frame which seems a bit undefined to me. I refuse to invest in collective investment not approved by the FINMA or which are not compliant with the ucits rules of the EU.

2-3x leverage with the mortgage that’s how

Yeah, even focusing on dividends alone, it’s also dishonest to compare their leveraged return with stocks’ unleveraged yields.

Direct ownership in land registry, no?

They’re just a commission-driven real estate salesmen and managing company, not a fund.

There’s yet another option here in Suisse Romande called Foxtone.

The thing is that I am convinced by the arguments put forward, contacted them, asked questions and was ready to invest. Then I saw that the minimum contribution was 50K and that is was is preventing me from “investing” with them.

On the other side, I’m irrationally convinced that there is something wrong and that these people need Swiss salaries, that they have very few projects and that therefore something’s off.

What’s your take on all this?

Yes I can confirm that this is the case with Foxstone because I asked this very same question.

I’m a big fan from crowdhose. I have started following them since 2017 and have been to one of their initial seminars.

I have seen the other options in Switzerland but still belive Croudhouse is the best. They do not get involved on the construction of the property or in the deal, they make money by managing the property and organising the deal.

By investing, yes you get you name on the land registry and you are not investing on the platform. If Croudhouse goes bust you can assign another property manager to the property.

I have not invested so far as we decided to purchase a small apartment for Buy-to-let. Main reason for this is that the small apartment belongs 100% us. There is no potential problems and discussions with co-owners. Also it is easier to divest (sell) if needed. Crowdhouse has a secondary marked since about a year but it was never used, nobody sold yet. So it is untested.

Also, by Crowdhouse it is uncertain what will happen with the property after the 5-7 years investment timeframe. The plan is to sell it but owners can always oppose it.

Another point which I am not clear about is the liability of the loan, if it is only on the property or also on the investors.

In summary, I give Crowdhouse thumbs up and think it is an amazing vehicle. However I prefer to do the first deal (buy to let) on my own. The next may be through them.

Here a potentially interesting review on Crowdhouse (et al.): Crowdhouse: Critical Review, Risks, and 5 Alternatives - Le Bijou Invest.

It certainly explained some of the details to me (noob), such as risks; and also confirms what @hedgehog mentioned above, on incomes “leveraged through mortgage loan”.

p.s. Do not like the oversight of index funds / ETFs at the start, listing the investment options. ![]()

Long story short - based on this article and its summary, now I don’t think I will dip my toes into this instrument. ![]()

In the best case, we will receive about 6% per annum; the income is not guaranteed, and we have our money locked in real estate for 5-10 years without the real opportunity to pull them out. The model is capital intense and also you take a mortgage, that doubles your risks.

Personally, I came to the conclusion that investment in Crowdhouse and similar services don’t provide a fair reward for the risk. During my career, I have been setting up deals that would yield 7% fixed returns (bonds), and also other deals without even buying the real estate but rather leasing it, that would give me up to 21%, and 13% – 18% in average.

Thx for the link, interesting review!

I think the main issue is not Crowdhouse or not, it’s shared-ownership or not. In that sense I extract from the review more it’s generic critique.

And the generic critique I tend to share. For me one big questionmark is how could you exit such a deal. In good times that might be somewhat easy. In bad times perhaps not so much. In any case that’s a very small market we’re talking about then. It’s not as if you’re selling an apartment or house which is actually of use (you can live in it) - it’s only a fraction of an asset and thus only interesting to other people willing to invest in co-ownership… a small market I think…

Hey @Rod !

Great job! Could you tell us more about Crowdhouse? What has been your experience? What are the fees? How are decisions with the other owners taken?

I’ve been considering that option to invest in real estate but I’m just worried that

I invested with Crowdhouse for the first time in June this year after tracking regularly their real estate opportunities for about one year. I set myself clear conditions on what I was looking for in terms of building and I only invested after finding the ideal opportunity. Some of these conditions were that the building needed to be new, the total gross return of the rents excluding mortgage should be at least 4.5% and that it should be fully rented. At the end I took a share on a 2016 building that is estimated to return 7.1% per year.

Experience: My experience with Crowdhouse has been positive, I’m receiving my share of the distributed return on the monthly basis (6.1% is distributed and 1% stays in a fund for unexpected expenses). The communication, the support and the paper work handling from Crowdhouse has been good.

Fees: They clearly mention their fees on each real estate opportunity. I didn’t encounter any hidden fee during the process. If they decide to change their fees unexpectedly they will scare their regular investors (the trust factor is very important here) and consequently they will slow down their business.There is more and more competition in Switzerland for crowdfunding real estate so I would be very surprise if they do it.

Decisions: So far I didn’t had to make any decision with any other owner. We’re about 40 owners in this building. There is a few co-owners that have significant shares on the building (500k) so ultimately the decisions are made by those larger owners. With that amount invested I would expect that their only interest is to return as much cash as possible so their decisions should be aligned with my interest.

Real estate collapses: With a return of 7.1% per year I should double my investment in 10 year (72 rule). Even if that property collapses 20% in 10 year I would have returned 80% of my investment. Normally the real estate collapses when interest rate go up and in Switzerland rents increase when interest go up so I’m expecting to have a higher rental return to compensate the lost of value of the real estate. My only concern for the future is that there isn’t enough demand to rent all the apartments. There is a few large companies in the area where this building is located, if some collapse in an economical downturn then my annual return will decrease because the tenants will leave.

Large renovations: The building is 3 years old so large expenses aren’t expected, if you invest in an older building than for sure this is a real concern. In case large expenses occur it will first consume the funds that each owner is setting aside (1% per year) and it may also reduce the distributed returns. Only in a very bad scenario you would be asked to invest some of your money.

Overall the experience with crowdfunding real estate has been good. I also own a long term rental, an airbnb and some REIT’s so this is a very good fit on my real estate portfolio for diversification.

Wow I didn’t think it could be this high. You can appeal against your rent if it is “abusive” in crowded cantons, and abusive means the return is only 0.5% above reference rate so at the moment 2%.

Regulations for rent do not apply to “luxury” housing, hence the boom in luxury apartment developments in recent years. Btw single family homes with 6 bedrooms or more automatically fall into the luxury housing category. Rod, is the property in question a luxury property? Or how is that return realised?

The main principle that makes crowdfunding real estate so attractive is that a large portion of the property is funded by a mortgage at a fix low interest rate. In reality my 100k investment are leveraged with another 100k loaned by the bank. Without leverage the return of my investment would be ~3.6% instead of the 7.1%. Check out the Crowdhouse website for more details or any of the other crowdfunding platforms in Switzerland.

C.f. this post and the one after: Crowdhouse experiences

@dbu, @Daniel, @gesk, @rod, @triviamaster guys you are hijacking the introduce yourselves thread. this discussion should be moved into it’s own thread.

@Julianek what would you propose ?

Agreed. Sorry about that.

I merged the topic. Thanks for the notification ![]()

EDIT: and sorry if there were some mess during the merge, but i think it is fixed now.

A friend in the UK buys flats and rent them out in the UK. He is actually multiplying his rental properties x2 every year. Partly by renting and partly by flipping and buying new cheaper flats/houses. He actually was willing to give +10% to people who would invest with him. He created a Ltd company and pays himself a salary. So that in case of a bubble burst or other black swan situation, that he doesn’t go bankrupt but the company will go insolvent.

It’s hard to get a mortgage for a company. AFAIK banks want almost 50% downpayment in that case so you be won’t be able to offload much risk to the banks here

Now Foxtone permit min investment of 25.000 Chf (5% per year)

I did my firt operation and for the moment all good!!

If someone is interested I can help? There are to referal program

regards