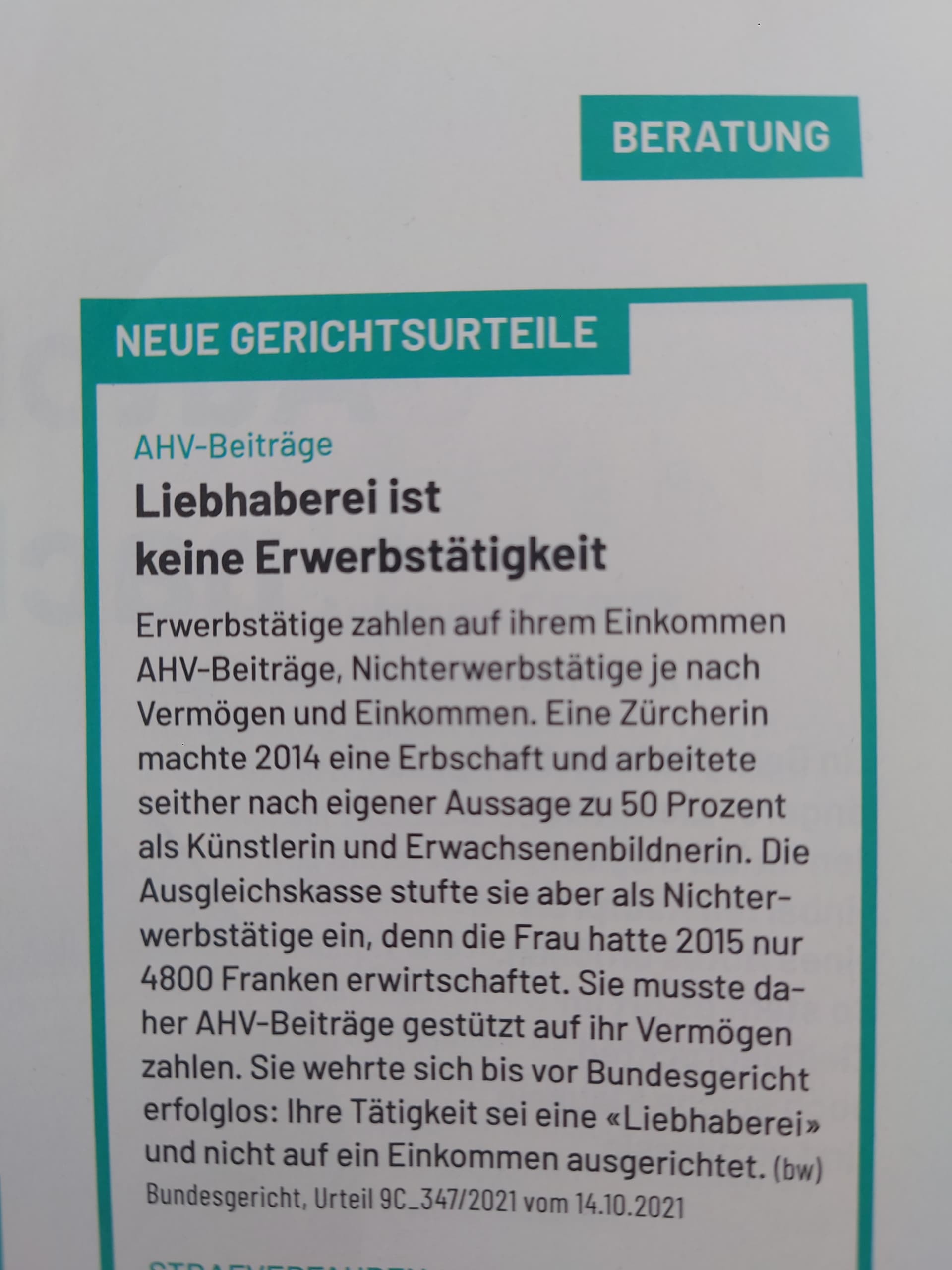

Please continue on the other thread mentioned by Barto

IMHO, AHV is like a tax. I won’t lose sleep on it AND also it’s relative to your worth, unlike health costs that are balooing and they won’t go down if you become poor.

Please continue on the other thread mentioned by Barto

IMHO, AHV is like a tax. I won’t lose sleep on it AND also it’s relative to your worth, unlike health costs that are balooing and they won’t go down if you become poor.

For 2 adults + 3 kids it is a bit over 20k CHF/yr.

To fund this needs >800k CHF assets to fund it assuming 2.5% SWR.

Food, rent and health are the no-miss items for me

[Edit: of course once 3 kids leave the nest cost decreases, and above assumes payment of full deductible every year in reality I only ever reached the deductible once in 20 years… but I get older…]

If/when you reach a point where you frequently have to pay the full deductible, you can and should switch to the minimum CHF 300 deductible, of course. This obviously increases the premiums but by less than the maximum deductible.

I.e., for the long term worst case / SWR, I think it makes more sense to use the scenario with the minimum deductible as basis for the calculation.

Probably mostly because at a 50% occupation the tax office probably still expects some 20k+ CHF of income.

Paying into AHV isn’t a bad thing.

28k/year AHV is potentially a big difference longterm. You’ll reduce your portfolio withdraws from 100k down to 72k per year (assuming 4% rule and 2.5M networth) and thus down to 2.9%. Or down from 80k to 52k (assuming 4% rule and 2M networth) and thus down to 2.6%.

This will ensure that you’ll never run out of money.

Edit: Plus it’s inflation-adjusted!

IMHO 7k is a really small social contribution if you sit on 3m chf and is IMHO not worth for all the part time hassle and (pseudo) work not even mentioning the swr offset the ahv generates after reaching the official retirement age.

Also keep in mind that it presumably only applies to taxable wealth. If e.g. 1 Mio. out of your total 3 Mio. net worth is in pillars 2 and 3a, you only pay AHV on the 2 Mio.

There is also a minimum wage in some cantons, you would need to earn at least 50% of that for this argument to hold. That’s assuming the work inspection authorities don’t ask for a statement of hours worked from your employer which I expect they would

You also pay AVS if you work so you are not really avoiding it

Ultimately I’ve accepted this and budgeted for this is an additional wealth tax

Once I no longer have a salary and my investments are my main source of income I will be more careful about margin loan, options, and to avoid too frequent buying and selling

Can I kind soul share what salary the spouse should have in order to end up paying 2x the minimum AHV?

I am a bit confused:

What am I missing/doing wrong?

Isn’t it 1’006 / 5.3% = CHF 18’981.

I also thought it was around 5% but I just checked and it is 8.7% for the employee and 8.7% for the employer.

In any case, 19K/year is a joke salary in CH, who earns that little? I am pretty sure one would not be paying 2x the minimum contribution with such salary? Anyway, I’d be very happy to be wrong cause that would mean my wife’s contribution would pay my AVH once I quit working.

AHV contribution for regular employment is 8.7% in total. Combined with IV and EO it’s 10.6%. 5.3% paid by the employee and 5.3% paid by the employer. 10.6% gets you to the CHF 9’494 minimum AHV income for the spouse, which has already been mentioned in this thread:

Hi all,

As I understand, one needs to pay AHV „Nichterwerbsbeiträge“ if one has no AHV-relevant source of income (and spouse neither). These are computed taking into account wealth. Do you know how these contributions translate to AHV payments in retirement (which I understand are rather linked to gross income)? As an example, consider a couple (A) married, both retired early, 3mn CHF wealth. I believe both need to pay around CHF 3000 per year AHV contributions. Also consider couple (B), same situation but 5mn wealth, hence paying each CHF 6000 per year. Does couple (B) receive higher AHV payments in retirement assuming (A) and (B) paid the exact same contributions prior to their retirement (ie same gross income)?

Thanks ![]()

But only minimally. The number of years you contributed is more important. For a man you need 44 years of contribution to get max ahv rente, and having an income larger than 86k

Thanks, actually I found the information here. The contribution is converted to a fictitious income via the following formula (see the end of the document): contribution/0.084 +0.5. Not sure what the 0.5 is for, I presume it is just for rounding. Hence if you paid 5000 into AHV as non-employed, this is converted to a fictitious income of around 60k.

One more question: as noted, the maximum AHV kicks in if you earn 86k on average. Does someone know whether the average is really computed as such or whether there is a cap applied on the annual salary? Say if you earn 100k half of the time and 70k the other half is your average income indeed 85k? Or is a cap applied to the income in years where you earned 100k?

Thanks, that makes sense!

I guess what Grog is saying is that number of years also matter, often more than the amount paid in. Take someone that comes to CH at the age of 45 and pays the maximum of ~24k/year into AHV for 20 years. That person will still only get AHV of 1,086 per month, even though in total paying in close to 500k. Someone having always lived in CH and paying the minimum contribution of around 500/year for 44 years will receive more (1,195 per month), even though overall only paying in 22k.

(Not sure whether all the figures are 100% correct but the point remains valid)

Well it’s meant to prevent retirement poverty and cover basic needs. So I like the system.