They are higher and will increase. Depending on your health state in higher age you might want to consider going for the 300.- franchise as well. So cost on health will rise with age.

Thank you. My take away is that once you stop having a salary the compulsory AVS contribution is approx 0.2 - 0.3 % of taxable wealth until you reach retirement age. I will think of it as an addition to wealth tax.

You’re welcome! Switzerland seems trickier than other countries for early retirement for the reasons you have said. The wealth tax and AHV on wealth can make the effective tax rate on income look high if you have lots of dosh. On the other hand, absence of capital gains tax is a plus.

For the AHV, you could arrange some form of employment in early retirement which could take you above the minimum contribution. After all, the authorities are mostly interested in people continuing to pay tax and social insurance so they are not a burden on society. Employment would also qualify you for family allowance if you have dependents (Familienzulagen).

I wonder if anyone else on here has experience of this stuff? I’m sure there are people who’ve perhaps been made redundant and are debating whether to pull the plug completely.

Yes. This sucks! The declared concept is “Ein Kind, eine Zulagen”, unless you are unemployed or RE. It’s very unfair, let’s hope it changes in future.

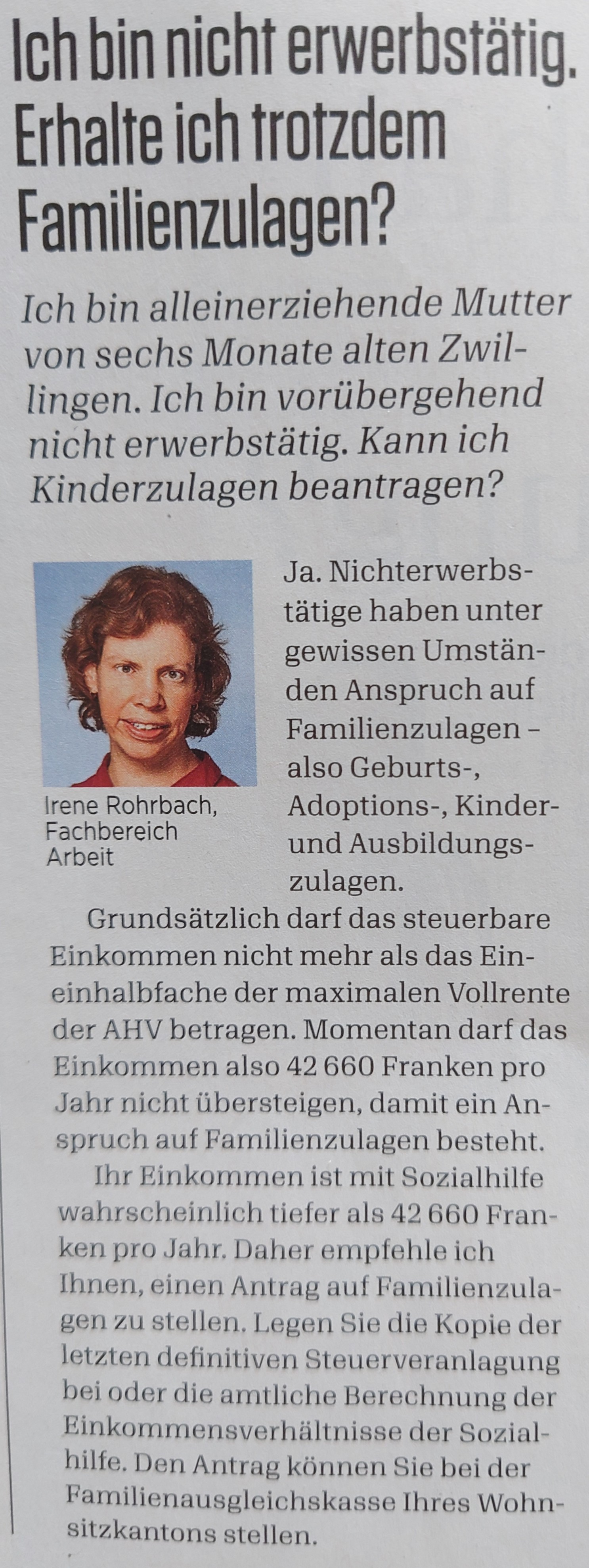

RE with dividend income of <43000 may mean you qualify for Kinderzulagen as a low-income person though. I don’t know if the Vermögen somehow gets included in the calculation, for a “low-income” but “high NW” person (such as a RE person may be).

I also thought about this but I think the following paragraph combined with minimum wage plus the fact that at early retirement you will have significant assets rule this out. What do you think?:

“Anyone with no income or only a low income is regarded as

non-employed. This includes in particular:

…

Insured persons who are not in permanent full-time work and whose contributions from gainful employment, including employer’s contributions, amount to less than half of what they would have to contribute as a non-employed person. Anyone who works for less than nine months a year or works less than 50 % of normal working hours is regarded as not being in permanent full-time employment.”

That is a good point. The idea of that seems to be to prevent people from taking a part time job to take them over the threshold for AHV. So the conclusion may be that our theoretical early retiree would need a full time contract paying a halfway decent whack. (Which turns FIRE into FI.) Hmm.

Tangent question:

What if you RE while having children going to the kindergarten?

No (tax) subsidies for those costs then I suppose (without income)?

(Assuming you don’t keep them with you at home 100% of time)

I think FatherDougal’s cunning idea was to take a small job after Retire Early so that you can say you are employed and paying some AVS from your salary. The 2nd part of the paragraph kills this off because if you work <9 months by their definition you are non-employed. They will therefore make you pay AVS based on your wealth. You will however get a credit for whatever you paid based on your salary.

A condition of using the state subsidized creches in Geneva is that the parents are in employment or on unemployment support looking for a job. I don’t know about other cantons.

You say you have to pay because the definition “non-employed” = has to pay according to his wealth.

Correct?

I didn’t get that. I thought it was just another label without being really connected to that. My bad.

Anyway the contribution shouldn’t be that different from those you already have, probably lower. As long as you don’t fatFIRE

Yes, that was the idea. At first glance, I thought you’d need a full time contract, so a part-time job isn’t enough. On the other hand, maybe 50% employment is enough, judging by the extract you posted.

See what I mean about ER being tricky in Switzerland?!

Section 9 and 17 seem interesting. It looks like any contributions from a part time job count towards the AHV and then you pay the difference to what you would pay based on your assets.

They seem to do a comparison calculation in these cases.

You probably mean Kita/day-care 0-4 yo.

Kindergarten is compulsory & free (only half day though).

Tax & subsidy is two different things.

No subsidies if you are not employed, i.e. capable of looking after them yourself. If you are employed 60% for example you can only bring your child to a 60% spot at a subsidised day-care.

Tax reduction I imagine should be possible though. You are allowed to subtract day-care costs (up to a limit) from your taxable income. So I imagine even if you only have dividend income, you can still deduct the day-care costs. I’ve never seen a limitation to that, like only if you work you are allowed to deduct that. IMO one child = one actual day-care costs paid can be deducted from your income.

I am keeping it simple in my mind: based on what I read so far after RE you have to pay AVS of 0.2-0.3% of your taxable wealth until retirement age. The maximum is 25,150 CHF per year (if you have 8.55 Million francs taxable wealth)

Can one maybe create a company (share capital of the company = your RE capital), become employee of that company and manage/invest your funds. You get a minimum salary paid-out (taxable) and/or dividends (taxable)…

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.