I have my third pillar invested with VIAC, chose the Global 100 strategy and it´s performing superb so far (2021).

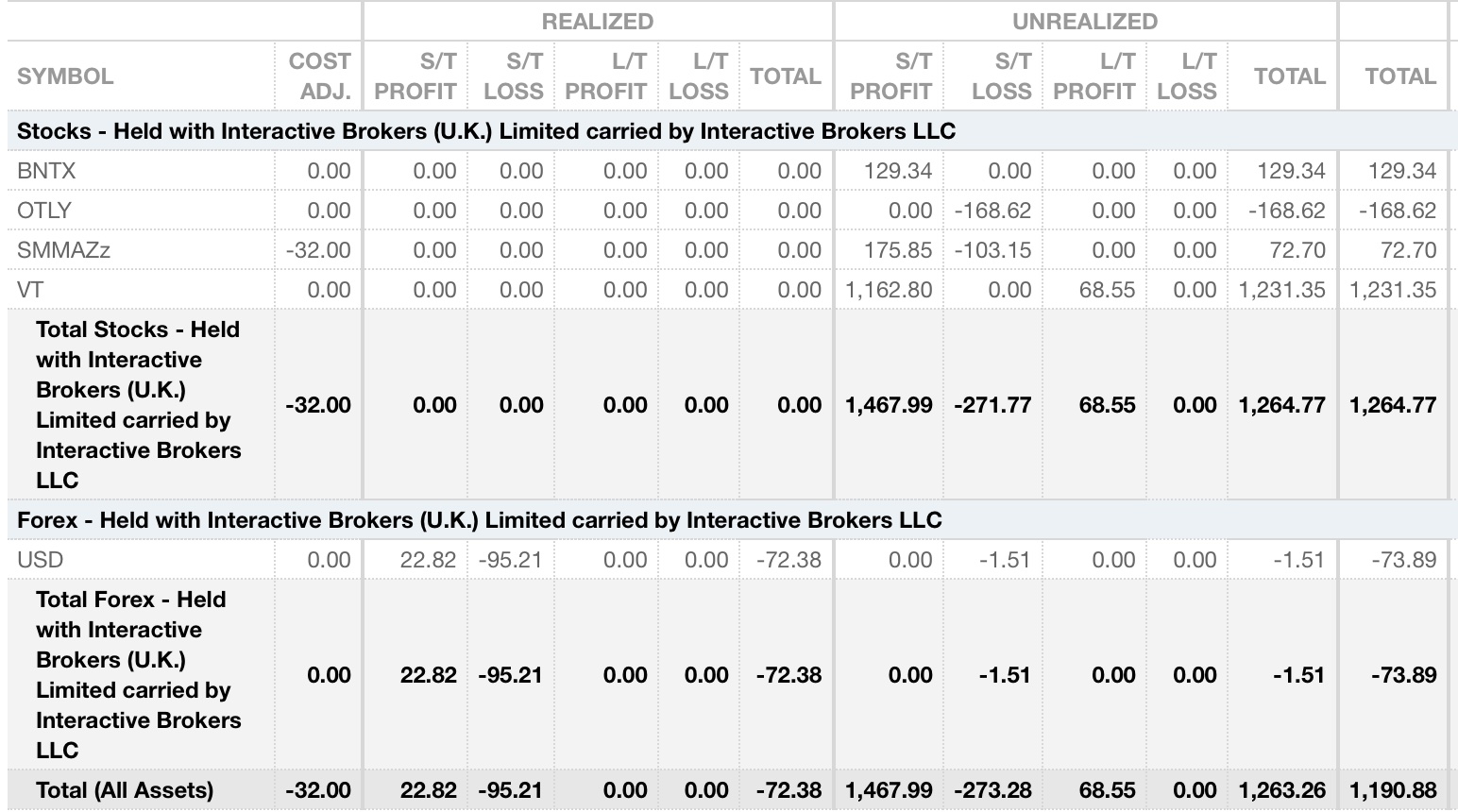

My excess savings are invested via Interactive Brokers in ETFs (VT and SMMCHA, exactly like in the mustachian portfolio described on the website) and the performance is … okay I would say.

Now the question:

VIAC actually states exactly how they compose the portfolio for the Global 100 strategy so there´s a tiny temptation building up to just copy that portfolio in my IKBR account to match that superior performance. The principle of risk diversification tells me that this is a bad idea.

That’s a pretty bad idea, esp. over such a small data point. It’s like buying TSLA in 2021 because of the 2020 performance.

Why should things that overperform over a short period of time continue overperforming? Maybe over 10 or 20y (including a bear market) you could make that call, but even then it’s just basing your allocation based on past performance.

Pension funds have taxation privileges that apply to the US and now to Japan, for VIAC (Finpension had Japan already included). I would try to maximize that and, considering all my assets (taxable, 3a, 2nd pillar) as a single portfolio, would use my 3a for the part invested in the US and/or Japan as much as I can.

All in all, I’d focus on a target global allocation for the whole portfolio, then use VIAC for the tax advantaged funds (CSIF US - PF, CSIF Japan - PF and/or CSIF World ex CH - PF Plus and/or CSIF World ex CH Small Cap - PF). Since I like simplicity, I’m using mainly the CSIF World ex CH - PF+ and CSIF World ex CH hedged - PF+ funds in VIAC.

Of course, the TER of the funds you would then use in your taxable account should also be taken into account.

Good point. But isn’t there also some inefficient exchange of currency going on at VIAC? I remember lengthy discussions about it here on the forum which led me to use VIAC mainly for CHF-denominated funds, but I might have to revise that choice.

There probably is. Some funds have built-in hedging which often isn’t advised for equity funds. Most have higher TER than you’d find by searching for low fees funds and brokers in a taxable account. I haven’t made the comparison myself.

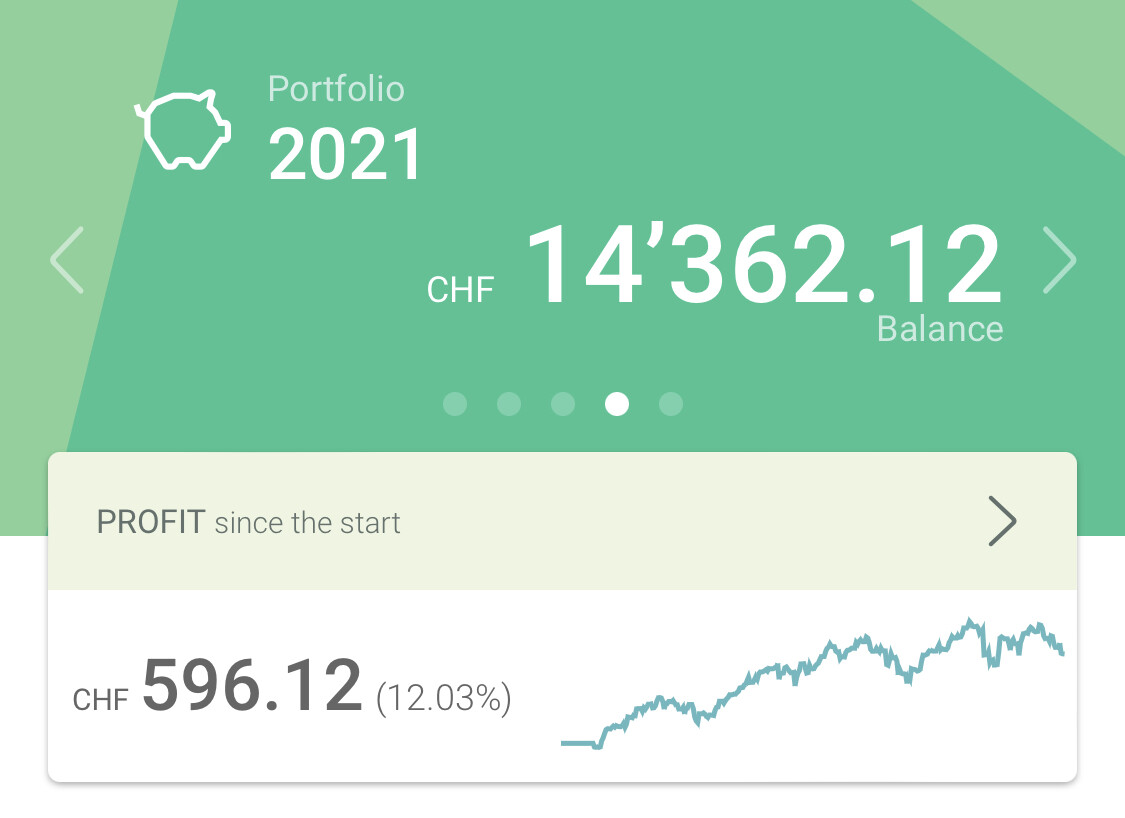

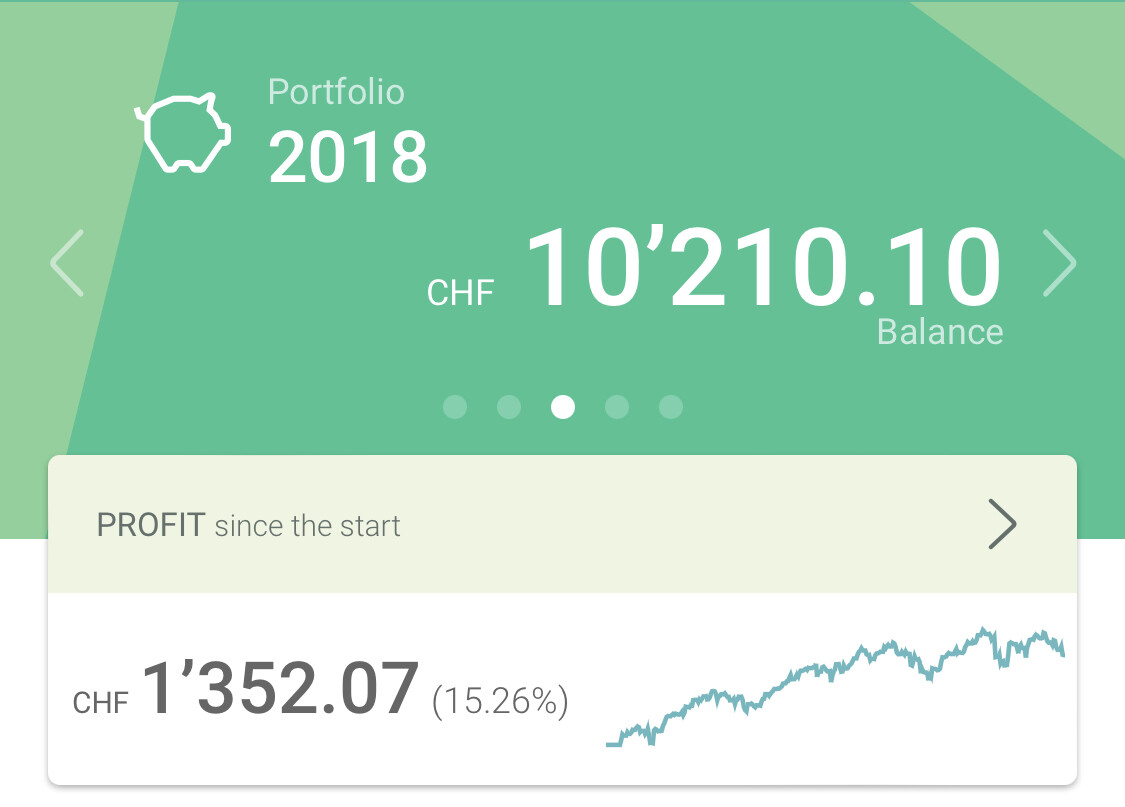

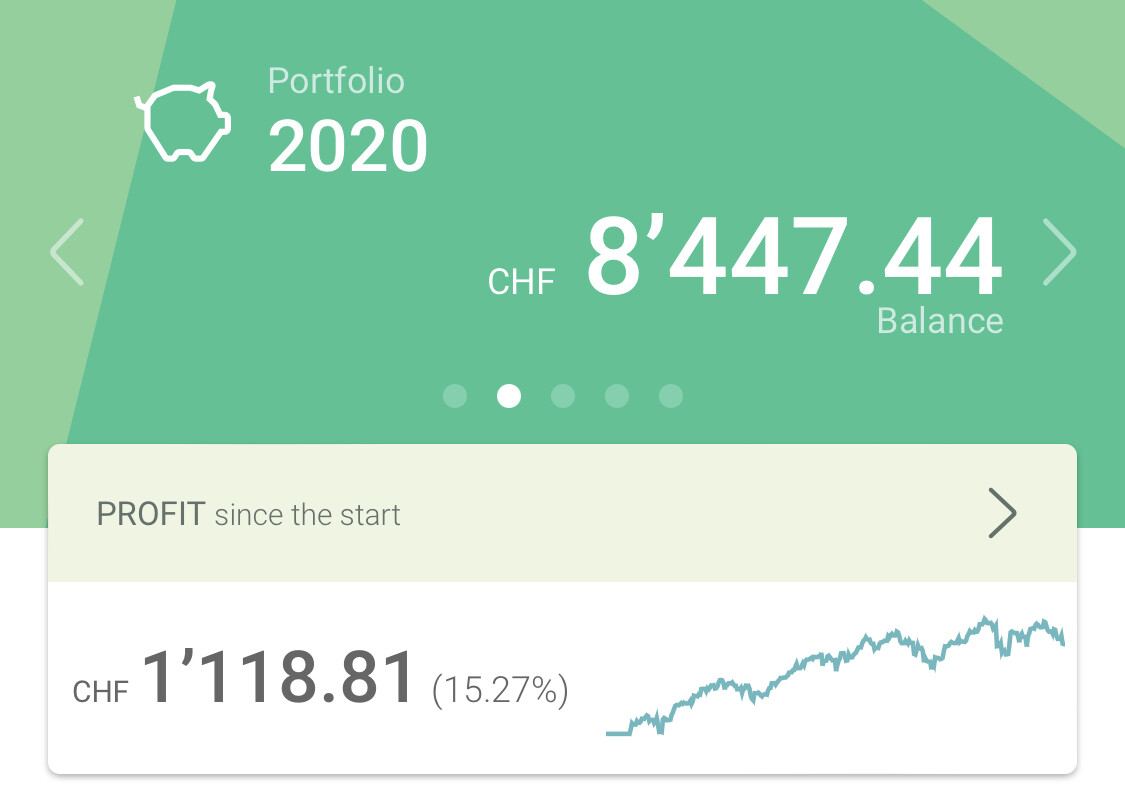

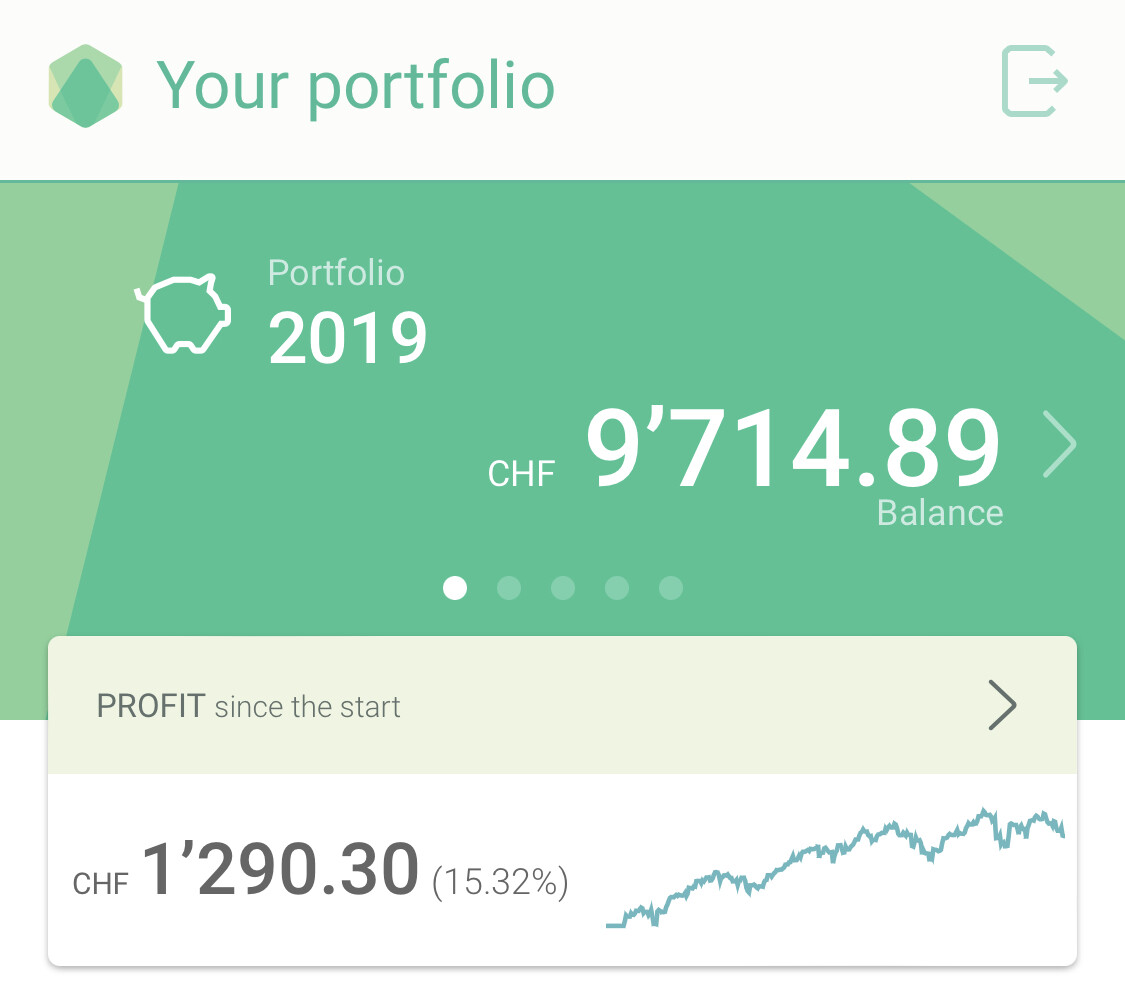

I have to come back to my initial question and want to back it up now with all of my numbers (which confuse me):

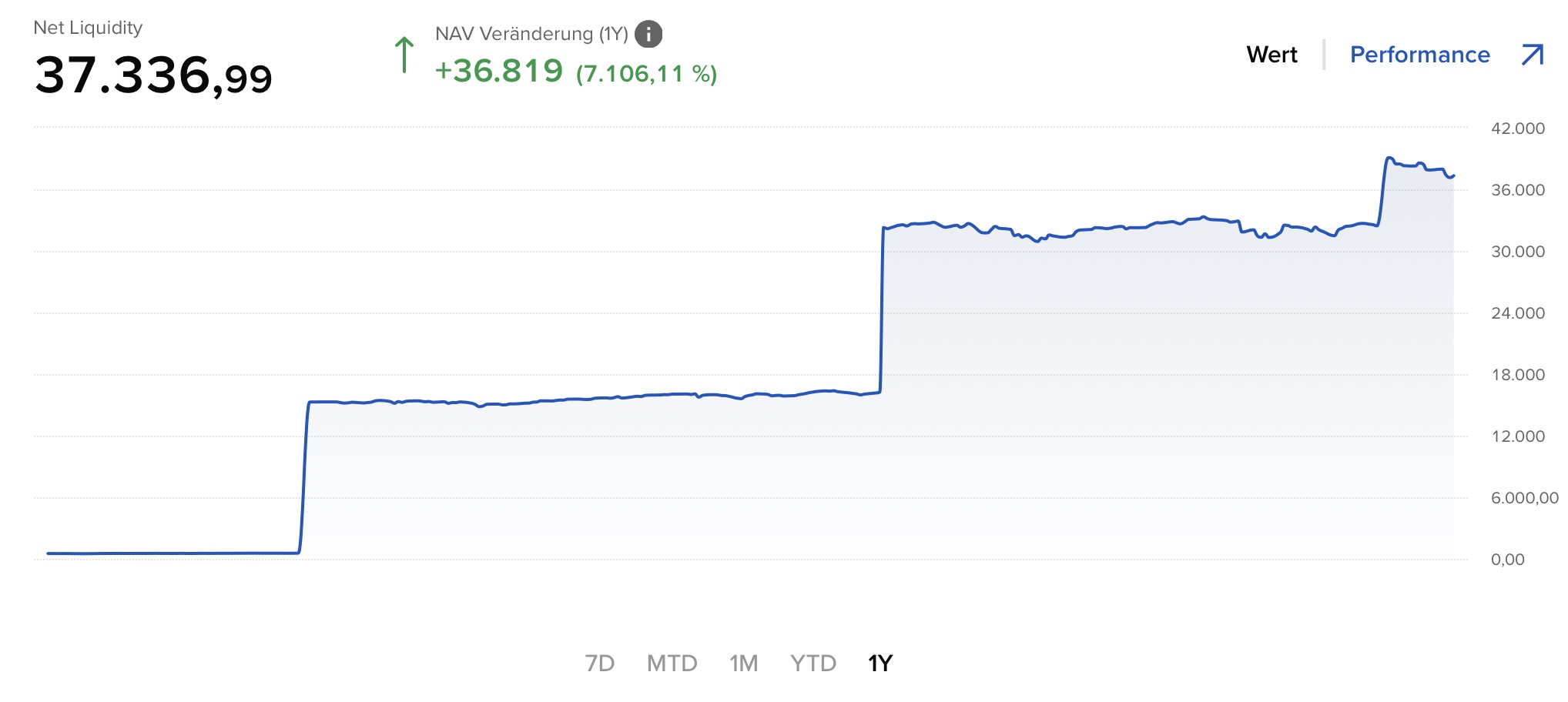

All of my VIAC accounts with the stated profit as CHF and in % (“since start” in my case means from 19.01.2021, that is when I opened the VIAC account):

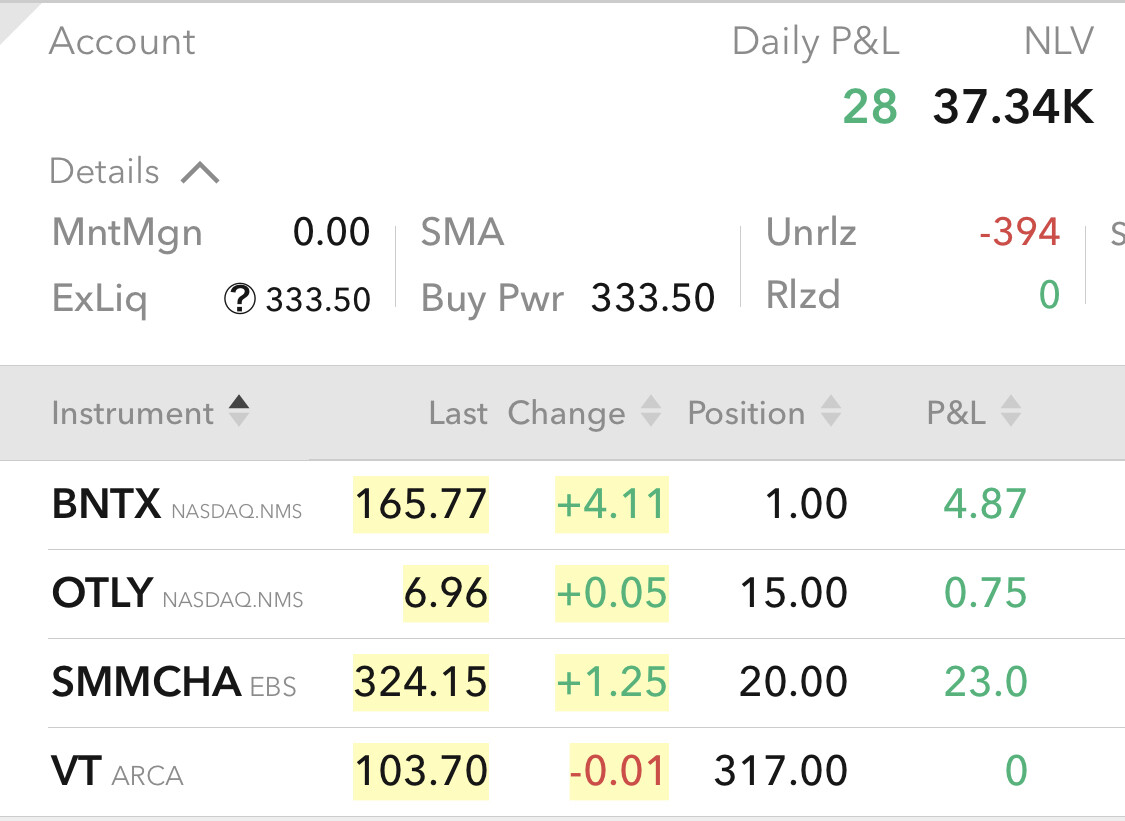

My problem still remains that I don´t understand why the absolute gain in worth (in CHF in VIAC and also CHF in Interactive Brokers) is so different:

While VIAC gains and gains and gains in absolute worth, my portfolio in Interactive Brokers just gains through cash inflow (I added 3 times since start) and otherwise rather remains the same or even looses (in the current screenshot it states -394 CHF, which I interpret as the overall gain/loss since start of investing).

I totally understand that that is what can happen if you invest ion the stock market but I don´t quite understand why VIAC and my portfolio perform so differently.

it looks to me like you went all-in @VIAC in Jan 2021, but only went in in 3 steps spread over 2021 @IB, 2 of those payments were in the second half?

All the gains (for example VT) were in first half 2021, second half was flat.

@rolandinho

That´s correct, I transferred all my existing 3a money in January 2021 to VIAC. In March 2021 I transferred all my “excess savings” for the first time to IB and added up in August and December.

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.