Actually FP generally have very low TER funds in their offering for 3a. So yes 0.39% includes everything

For Truewealth- it appears they don’t charge anything on top of TERs. But yes the TER cost is important in that case

For emerging markets -: I think it doesn’t matter if you have ETFs or funds, they would all have similar issues of Indian capital gains tax and hence would be tough for them to track their benchmark indices. If you look specifically for India exposure, you can clearly see this for ishares NDIA or Franklin FLXI where both cannot match their benchmarks. In simple words, there is no way for any ETF/fund to match their benchmark for Indian exposure because of the assumption of capital gains tax (short term and long term)

To compare fund performance , I think best way is to use UBS quotes (if you have UBS account) and you can add multiple funds for comparison. They have all funds in general. In reality 3a fund is still a fund

P.S -: I tried to look into the Indian ETF matter in detail because I wanted to decide which ETF to buy. It looks like the portfolio turnover drives a lot the final performance due to capital gains in bull market. In bear markets this can change

The measure of performance that matters to me for passive ETFs is how good the fund managers are at tracking their benchmark index so, for comparison between funds tracking the same index, I’d use tracking difference as my metric.

The fund litterature and https://www.trackingdifferences.com can help. Unfortunately, local pension funds are less analyzed than global widely available ones and their metrics are harder to find in a fully comparable form (using the same methodology).

For the choice of the indexes I want tracked in my portfolio, I’d rely on fundamentals (methodology, including country coverage). Past performance isn’t a factor that enters my reflection, what enters it are if the conditions to nurture good future performance are met or if I’m doubtful that they are.

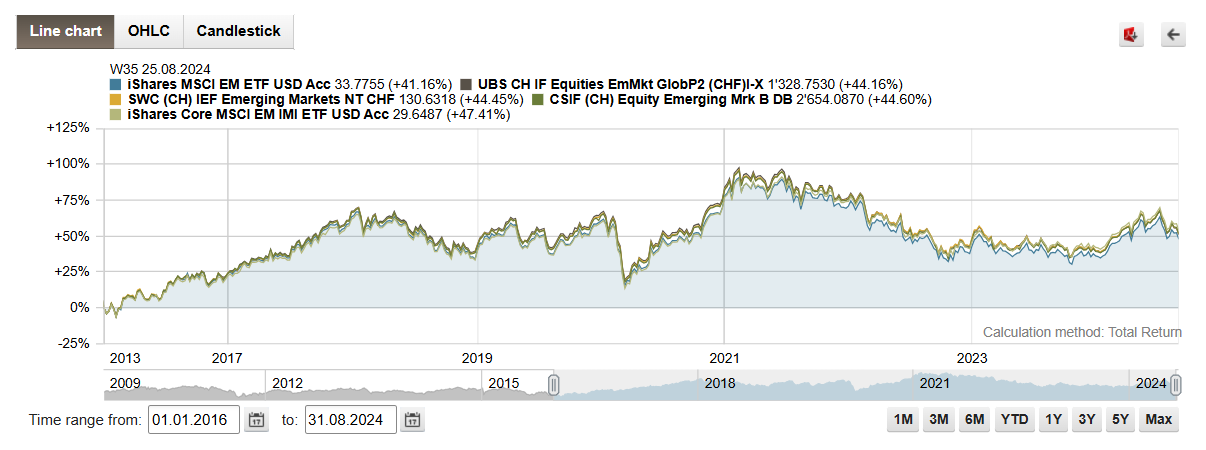

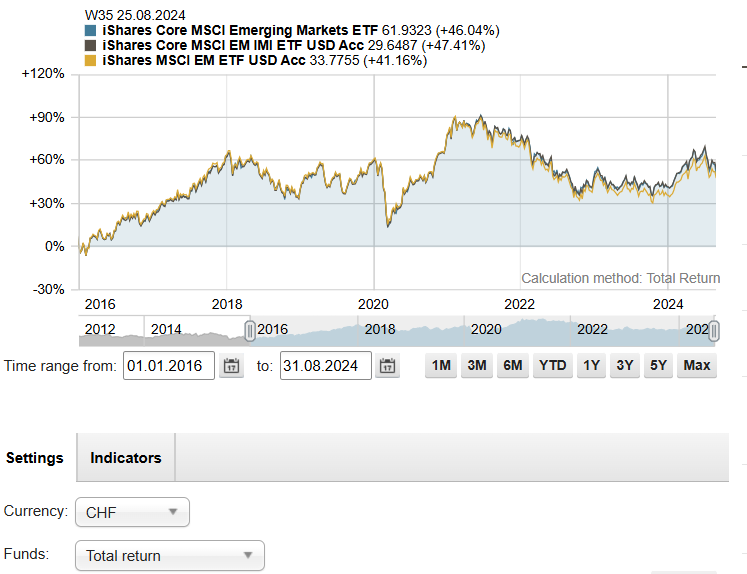

If we do a like to like comparison, Finpension offerings (CS, UBS or SWC) has outperformed ishares MSCI EM ETF. This is illustrated in post. In other words if FP offered ishares ETF IE00B4L5YC18 (41.16%) , then it would have underperformed the current option of CH domiciled funds (44.6%).

The difference in historical performance you are quoting is not because of use of CH domiciled funds vs. ishares ETF. It is due to underlying stocks. MSCI EM IMI (IE00BKM4GZ66), 47.4% has outperformed MSCI EM IE00B4L5YC18 , 41.16% over the period we downloaded the data most likely because small caps stocks in EM outperformed large caps. But this does not always mean that this would continue in future. This has nothing to do with ETF vs fund, it is simply the conviction on small caps vs. large caps.

Hence if investor seeks to invest in MSCI EM IMI via 3a, then only choice would be Truewealth. But the same outcome can be achieved by continuing to use FP and invest a small amount in MSCI EM Small caps in IBKR.

P.S -: I understand that CS funds have this high redemption fee, but I cannot confirm if this is good or bad for current fund holders vs UBS fund which provisions already in NAV. In general I tend to not over-optimize 3a offerings from Finpension. I just use the standard Global 60 or Global 80.

Another point to think about is that even though factsheet of Credit suisse Fund has redemption fees, it could very well be possible that this fees is not really charged to investor. This would depend who many redemption and purchases are made on the day of redemption at Finpension. I doubt that FP will sell these units unless there is a net outflow on the day of redemption

I would rather assume that you have been lured into it with the promise of a lower interest rate, and you might have not understood the full extend of this decision. (of course we can discuss transparency)

Well, I was a bit dramatic there. I’d like to state that I don’t see myself as a victim.

It was a compromise between me, my wife and the time we were able and willing to invest.

Also a lack of experience as first time home buyers made us take certain shortcuts that proved shortsighted.

With hindsight:

To do a full cost analysis of a mortgage offer, you need to take into account the funds you will be able to invest in for amortization. If they’re expensive bank funds, as they are in the case of UBS, the opportunity cost can be massive over an amortization period of 15 years.

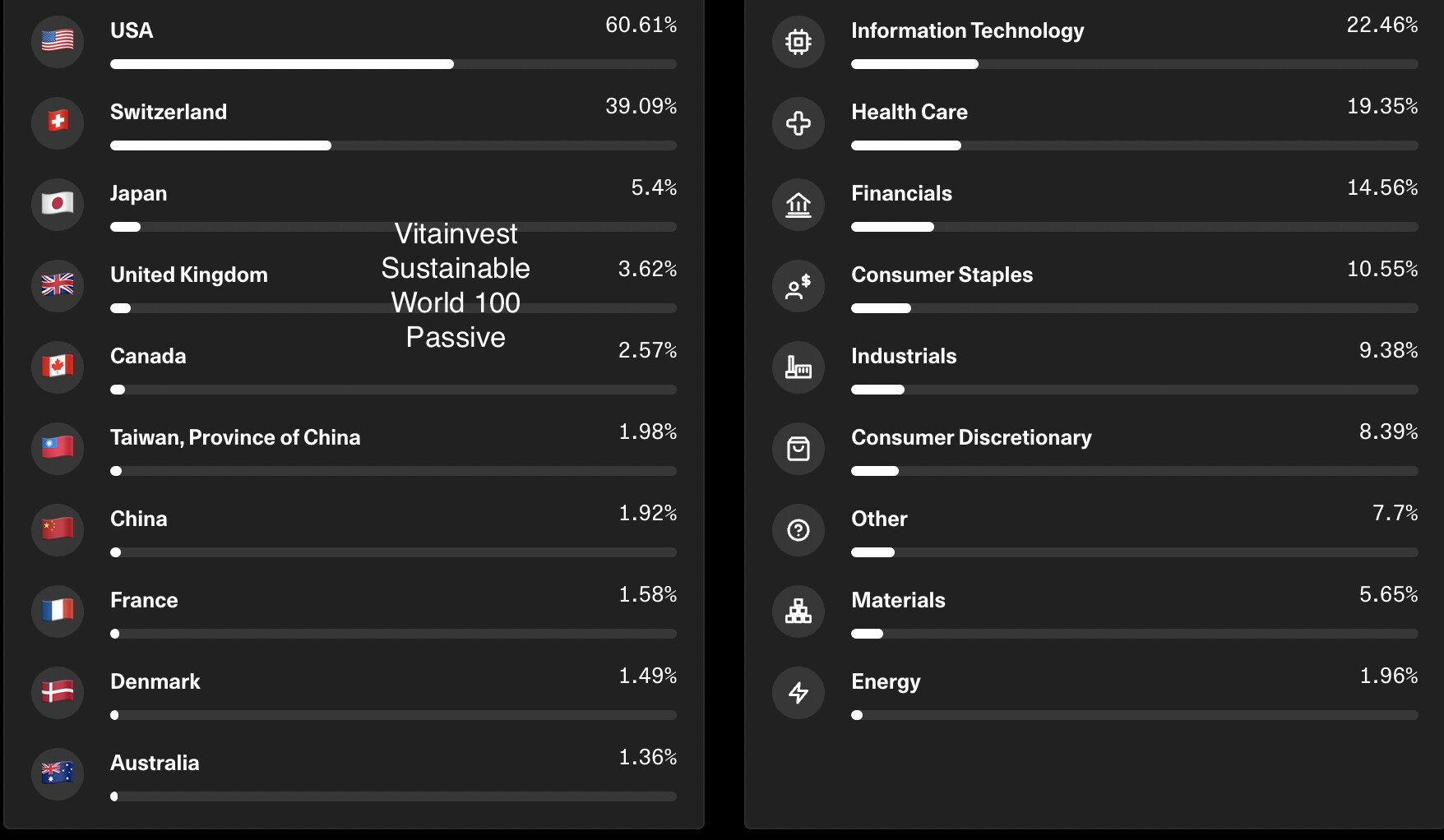

In the case of UBS, my back of the envelope calculations between the Quality Fund at Finpension and the UBS Vitainvest World 100 Passive suggest a performance difference of 1.5-2% a year. With the Active 100 World, it would be around 3 %.

With a 3a capital that currently stands at more than 60’000 CHF, that’s an implied cost of currently around 1000 CHF per year which only increases over time. Plus the lost future returns.

I will call our UBS account manager to request a reduction of the amortization requirement and to see if there is anything else we can do.

Can you help me understand the breakdown for this difference?

TER %

Other factors

I think you are overestimating the returns of Quality fund. The TER% of UBS passive fund is higher. I think net-net UBS is 0.5% more expensive than Finpension. But where is the rest coming from?

Active fund is not really relevant because you would normally use passive.

I’m in the process of setting up 3a account at Finpension. Also want to change my current vested benefits account strategy (all CS funds). Are the Swisscanto funds the best option?

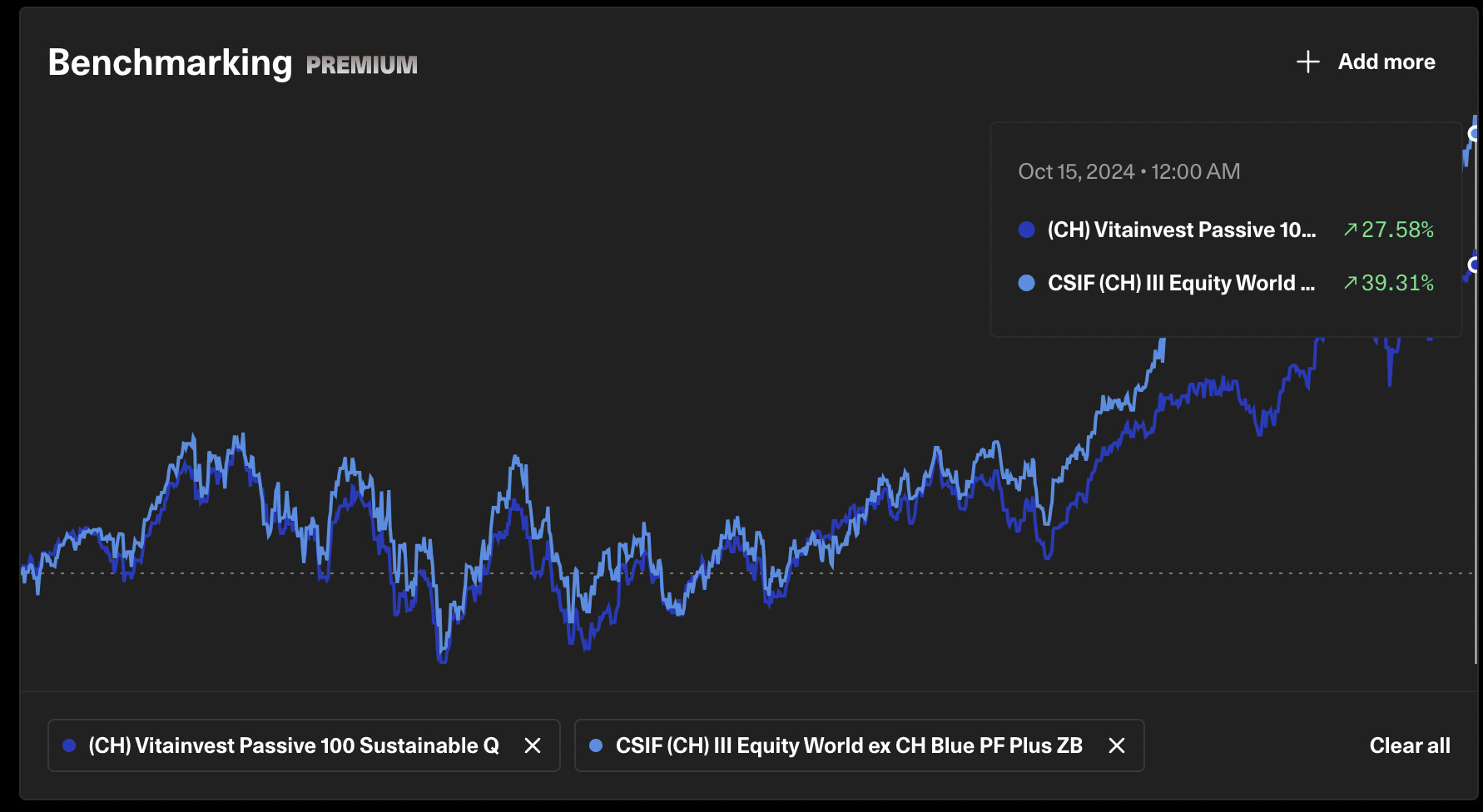

The following comparison is based on the fund performance, not portfolio.

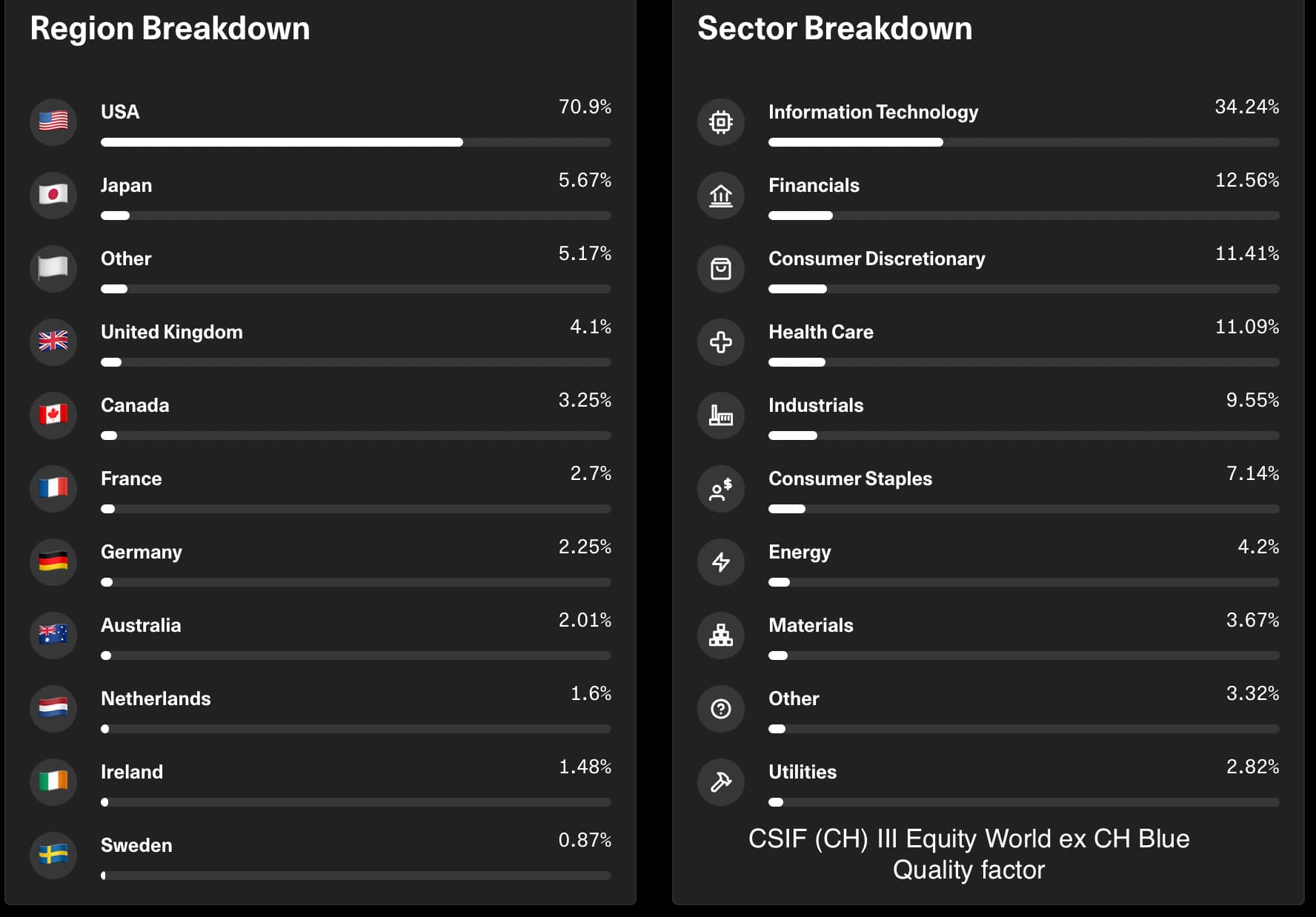

Fund Finpension: CSIF (CH) III Equity World ex CH Blue (CH0429081620)

Fund UBS: Vitainvest Passive 100 Sustainable Q (CH1110134157)

I am chosing these 2 funds because I’m invested in them, not for any other reason.

1. TER is lower

CSIF (CH) III Equity World ex CH Blue: 0.0038 %

Vitainvest Passive 100 Sustainable Q: 0.25 %

2. Allocation is different Vitainvest 100 is more conservative: Lots of Switzerland, less tech, hedged for CHF.

It is heavy on ESG which limits the choice of shares (for better or worse).

As far as I could glean from the factsheet, no benchmark is given.

3. Performance

So, I can’t be bothered to get a correct Total Return because UBS is distributing and Finpension is accumulating. So I looked up the dividends and made a guesstimate.

Dividends for Vitainvest Passive 100 were

2022: 0.32 CHF

2023: 0.72 CHF

2024: 1.25 CHF.

It increases total returns by a bit more than 2 %.

In any case, the graphs for a hypothetical investment on July 6, 2021 (launch date of Vitainvest Passive 100 fund) look like this:

Adding the fee difference of 0.26 % difference in fees,

the opportunity cost of holding the UBS fund is 2.2 % + 0.26 % = 2.46 % (approx.)

Some musings and caveats:

I was surprised by this big difference. It’s not why I picked this example. A typical 3a solution is more diversified and would make for a smaller difference between portfolio performance.

Past returns ≠ future returns

3 years and 3 months is not a long time for a comparison.

The recent rally has basically shown the huge difference the asset alllocations makes. The FP fund’s exposure to Tech/US has tipped the scale massively.

Given the more conservative setup of Vitainvest 100 Passive, a significant difference in performance is likely to persist. Maybe not to the tune of 2 %, but 1-1.5 certainly, and more so after the fees.

Thanks for sharing

I think in principle having flexibility to invest is always better . So I would also prefer Finpension or Viac.

And obviously custody fees would also be lower

The point I am trying to make it that if you do get a better mortgage because of your 3a, then this difference might get compensated

Regarding past performance of US or Tech vs . Switzerland, that’s not a guarantee for future. Right?

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.