I’d be interested in getting my 3a closer to VT (right now, I have Global 100 in Viac with its heavy Swiss bias meaning 40%) as simply as possible.

From the 1h I just spent reading the forum to get up-to-date info regarding the best 3a, given the comments above about FP and whether it’s better than Viac, it seems that:

there might be some differences in mortgage / insurance possibilities

Regarding strategies:

it’s possible to invest in a single “Quality” ETF via FP which one could consider reasonably close to VT, but fundamentally it’s still different

it’s possible to customize the allocations in Viac and FP but then you need to rebalance that from time to time if you want to approximate VT this way

If I rule out 3. for some reason (see the debate in the thread linked above, I don’t want to rehash that here), then it seems that 4. should be my favored approach? And given 1. and that I don’t care about 2. (at least for now), FP or Viac should be the same for me? Does that make sense? Is there an ETF available in FP 3a that’s closer to VT?

Short answer is there is not much difference except for currency conversion (and insurance + mortgage possibilities)

There is no single fund to get VT on either.

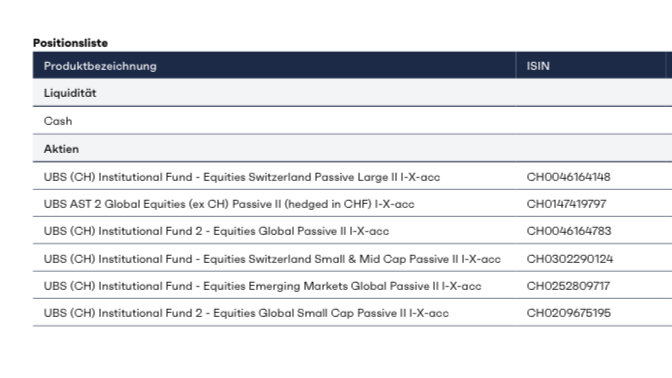

You have to do MSCI world ex CH + CH + EM to come close to VT. maybe consider MSCI world small cap too.

The major difference between VIAC and Finpension is that FP has CHf denominated funds while VIAC has USD denominated funds ( same underlying funds) . So there will be currency conversion when buying selling and a bit at rebalancing in VIAC.

It shouldn’t matter much. The performances are about the same, although the benchmark varies, probably because some fund houses don’t include the returned WHT from US/JP in the benchmark values, even though they receive the WHT.

I would choose UBS. They have the best spread and explicitly state that they get WHT back from US and JP.

Yes they do, but e.g. Swisscanto apparently doesn’t include the reclaimed WHT in the benchmark, so it looks like the fund is significantly outperforming the index every year. Whereas the others have about the same performance, but adjusted benchmark values, so the (smaller) tracking difference is much more honest.

Did they specify what tax optimized™ means?

Any chance you get a comment on whether 3a/VB type of funds can generally be considered as “pension funds” in DTAs and thus exempt from WHT (where applicable)?

For which index is that? For EM, aren’t net return (NR) and total return net (TR net) the same thing?

The few I checked, both Swisscanto and UBS sometimes us NR, sometimes TR.

To simplify further: if I want to somewhat replicate VT, I think I could consider the Swiss market as negligible (2.10% in VT).

Then it’s a matter of opinion, but maybe getting rid of small caps and EM to end up with just MSCI world ex CH wouldn’t be too bad. And that should minimize fees, since there wouldn’t be any rebalancing necessary, right? So less transaction fees, less currency fees (in the case of Viac)?

I haven’t really checked yet whether this would make sense to bet that much on developing countries high and mid caps vs small caps and EM (and I wouldn’t if I could just get VT or equivalent), but maybe the simplicity of the setup would be worth it in my case.

Actually I asked them if I need to figure out which fund to use because all the suffixes and prefixes are confusing. My question was mainly for WHt. They said that all their funds in 3a accounts are optimised for withholding taxes in foreign jurisdictions (wherever applicable)

Ah you’re right. Swisscanto uses MSCI World ex CH “TR Net”, ex-CS “TR” and UBS “div. reinv. US gross, others net” (even though a few lines above they explicitly state that they get back WHT from Japan as well).

Still, they all have almost exactly the same performance. I’d prefer they used the appropriate index to be able to judge the respective tracking error.

With unrecoverable WHT, NR is a good benchmark. It’s as much as you can hope for

With no or fully reclaimable taxes, it’s TR = NR

US gross, others net is creative, but even makes sense if you assume the average investor manages to reclaim US WHT by herself, but doesn’t bother about JP or CA.

Of course they did

It’s not answering my question, but I guess that’s as good as you’ll get from a customer rep. or a fund’s homepage.

What part of your overall equity assets is your 3a? If it is 10-20%, then the 10% of that is 1-2% difference in overall equity allocation. Then decide how much time should you spend on this decision.

In the factsheets of the respective funds you do get the total returns. They are not helpful if you want to compare performance from a starting date like the launching date of a fund.

The Vitainvest performance shown in Getquin does not show total total return because it does not take reinvested dividends into account.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.