I don’t know if we should start a new thread or continue on this one. In general, I have a few questions about the options going forward (not directly related to real estate).

We currently see a high rise in inflation world-wide. I know there’s no consensus about if this is just a supply-chain shock or if we have a general problem. Central banks still treat it as a supply-chain shock for now.

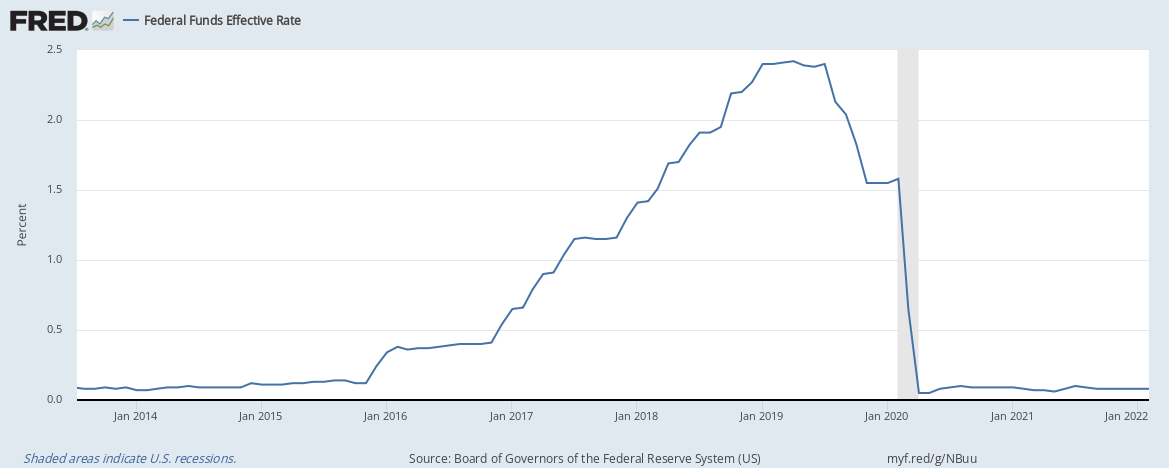

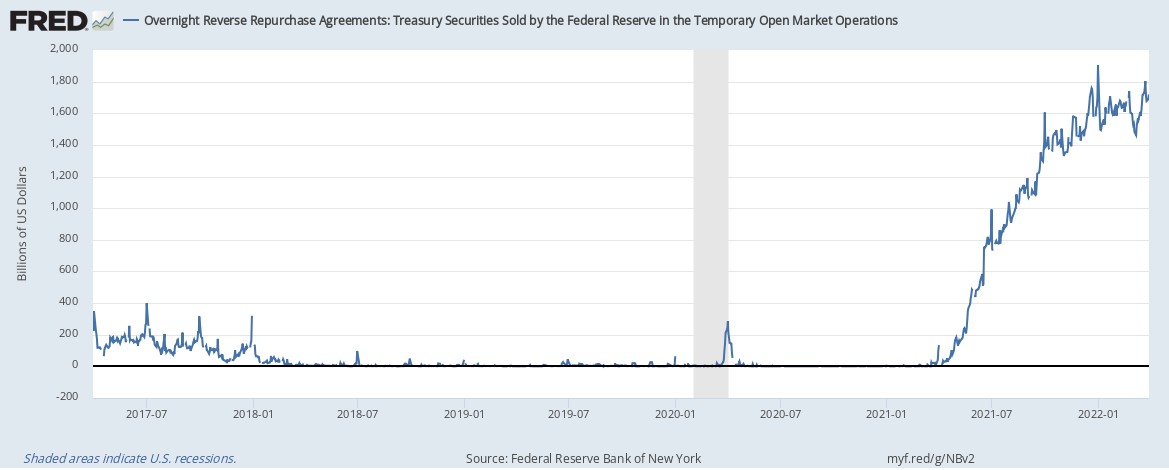

What we have seen in the last years are huge increases money supply. Already after the financial crisis in 2007-09, and especially from March 2020. We have seen a race to the bottom in terms of interest rates of EUR, CHF and USD. If you check macroeconomic literature, the central banks should be able to fight inflation by raising interest rates again. That’s the theory according to books. Reality might look different.

Even considering that theory is true, there’s a catch 22. No central bank wants to raise the interest rates first, due to public debt. FED might be the first central bank who’s going to raise interest rates, but if they do this will have a huge impact on the stock market and other assets (real estate, crypto market). They already tried that after 2015 and it had an influence on the stock market.

My question: what’s the way out of this catch 22? Is there any way out?

@mods: might be a new thread, if no such thread exists yet.

I’m curious to hear more about this. Do you have some more links about 1/3 of Swiss banks going bankrupt? Also, did people who were customers of those banks lose the cash on those accounts, or was it the ones who had real estate? That’s an important one for me to know, because I don’t own real estate but I have accounts with different banks (both as a private person as well as with companies).

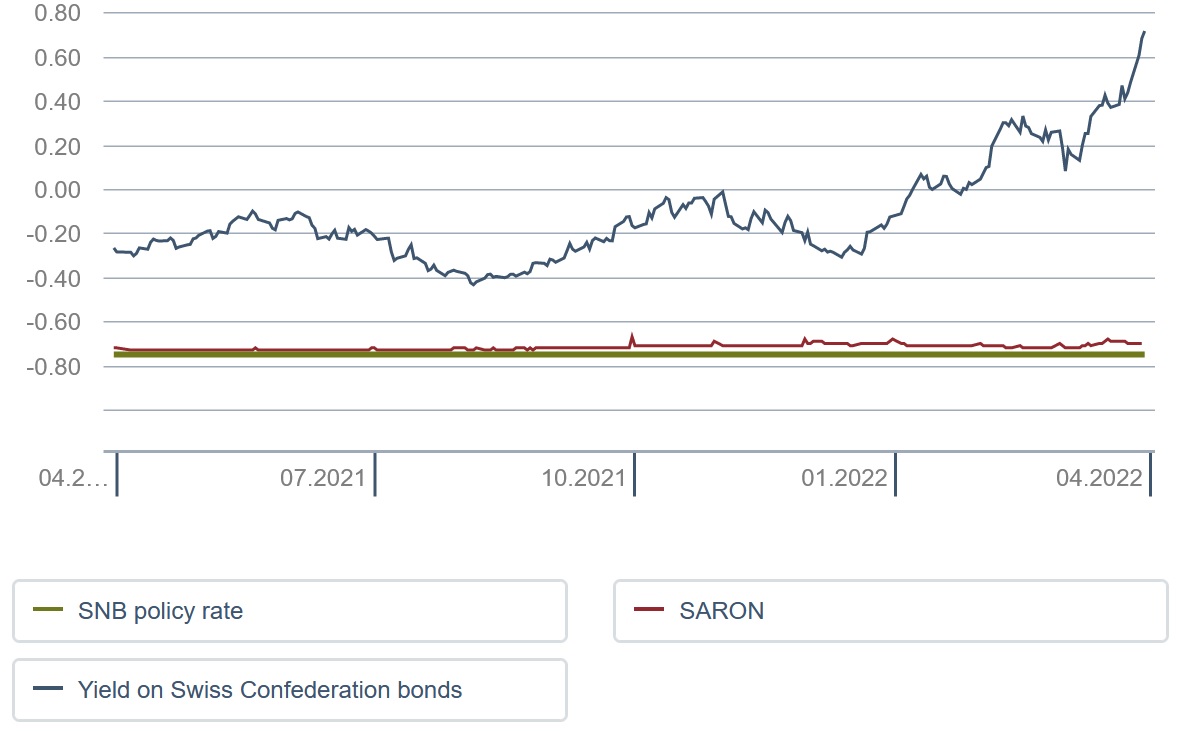

The quote “this time it’s different” is quite famous. In hindsight, we know it was not. One thing which is different this time is the negative interest rate for CHF. And SNB can’t simply raise the rates, unless it wants the CHF to appreciate even more. Back in the 80s and 90s, there were more national currencies than we have today. So the times are a little bit different.

I’m not a full-time economist, but at least I would expect SNB to try to keep interest rates as low as possible. Unless interest rates for USD and EUR also increase again, which would kill the idea of a central currency for EU (southern countries would go to default, bye bye Euro).