I wont wait for “the ultimate correction”, but gradually reduce the cash position to buy more stocks.

I cannot imagine a huge drop before central banks step in and open the gates again

I wont wait for “the ultimate correction”, but gradually reduce the cash position to buy more stocks.

I cannot imagine a huge drop before central banks step in and open the gates again

I can imagine a short recovery after CB step in only to be followed by further large falls.

Some of the stocks I bought on Friday are already down double digits! ![]()

Like we discussed last week, there is no point of timing the purchases or sales.

Asset allocation is key. Whatever your desired EQ/BOND/GOLD/BTC allocation is, try to stick to it and hopefully it would be all good in few years.

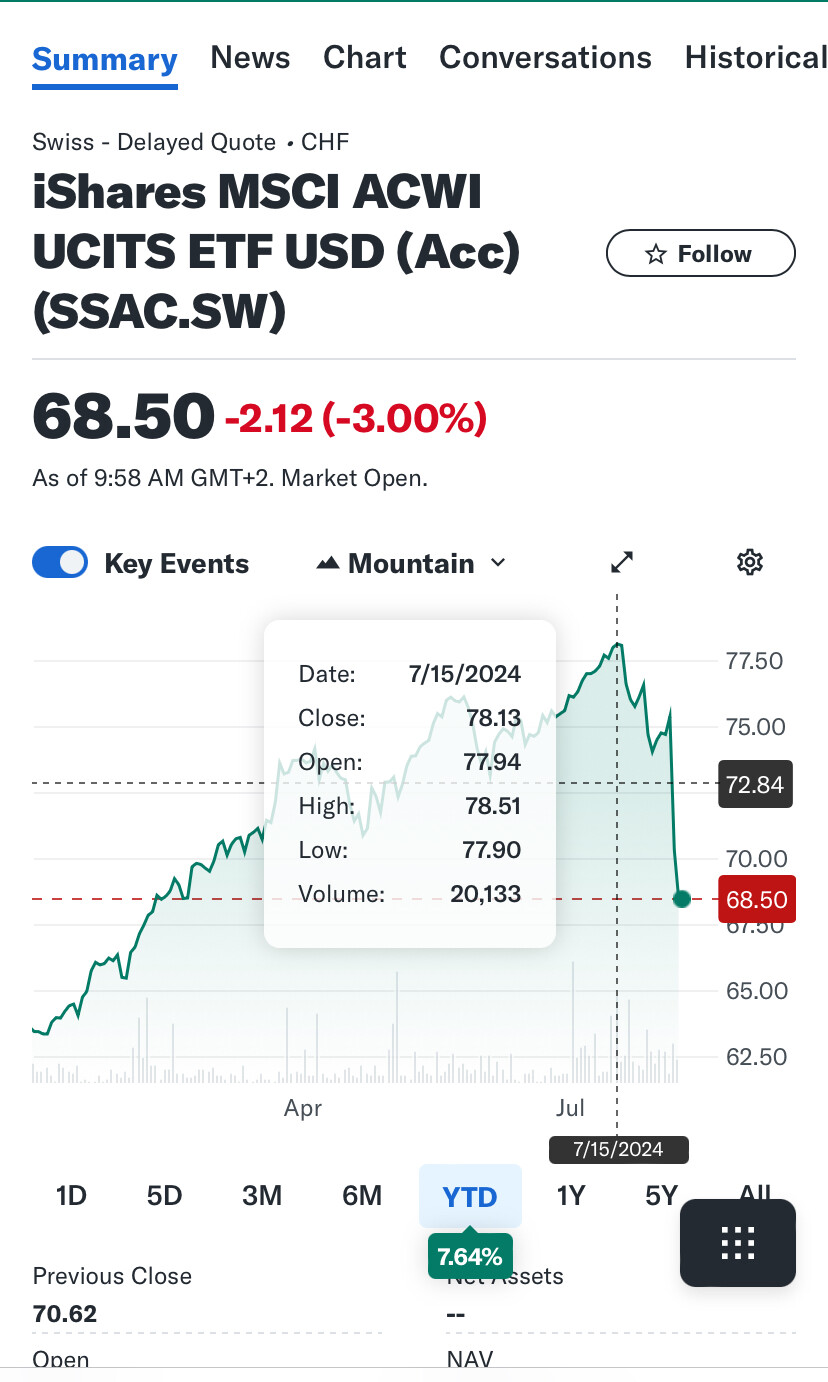

By end of the day today, Europe, Japan,China, CH all have negative YTD for their respective indices. US is still up though.

Tasty …

Japan Tobacco has been on my watchlist for a while, but due to my already big Tobacco exposure I’ve restrained myself so far … that’s just become a little harder. ![]()

Good to see this figure (131 trades only). The intent behind the “wait for 3 days after things have stabilized” is exactly to prevent the number of “buy-the-dip trades”. Logic is that buying the dip was generally bad for your performance. With this logic, you sstill have the illusion of doing something, but you don’t do much aka don’t cause much harm.

You’re holding it wrong.

Most of these rectangles are in fact green:

(Source: Starke Kursverluste an Tokioter Börse – auch andere asiatische Märkte fallen (nzz.ch))

How do we define what are sensible prices

Gold driven by fear mainly. So not sure how to define right price for Gold.

Stocks -: Japan felt like it was reasonably priced and same for Europe. Now they are even more „reasonably“ priced but no one cares.

Bitcoin -: it’s driven by theory „where else should people park their money because everything else is trash“ . Given the action of last few days, I don’t think cash is moving there. If that theory is not true for few weeks, what should be the right price to buy again? No fundamentals, no fundamentals based price.

If suddenly some central banks would start making comments , markets might settle but then this is not fundamental. It’s sentimental

you bought on day 2 of the drop (Friday) - today is day 3. Given the big losses in Japan, I would not be surprised if there was a drop day 4 tomorrow, and we only find the new equilibrium by Wednesday Morning. Don’t shoot your ammuniation at first sight of the enemy - hold your powder and only use it in small doses that you can keep utilizing for a few months.

Its not a sell-off (yet) and its not intense. Volatility is back. Lets call it a sell-off once we are (in CHF terms) at -15%+. And thereby, I mean broad markets like SPI or MSCI World - not bubbly US Shares or Nasdaq.

I was lucky to have bought in Sept 2022, so still up 46% after a 17% drop.

I was a net seller over Thurs/Fri (buying and selling on Thurs, and buying on Fri).

I hope @assemblyrequired didn’t follow @Helix’ (tongue in cheek) advice to buy on margin … but if so, resist the urge to pick up the phone today, @assemblyrequired.

sure about that? Just had a look at VWRL at Justetf. There, it looks like we lost 9.27% by Friday. Intraday moves don’t matter, so for me - we are currently below 10%.

Ok, when we have a look at intraday moves, we are at 11.7%. Still, I am relaxed so far. This can very well just be volatility. Lets see at month end, if we are in a down market or not.

I think sensible can be defined or at least aligned with long-running P/E or better CAPE ratios. We are two standard deviations overvalued there compared to historic average.

I think a little higher floor than the long-running average is sensible, because of today’s US market‘s high efficiency. But even considering this we are far off from sensible imo.

Confirmed, have a similar view. I do hold a static asset allocation (Stocks vs. Others). I would temporarily and tactically increase the Stocks Allocation, but only once prices are in a sensible level (meaning after at least -30% from where we are now.

I believe justetf uses last close info.

So we can check tomorrow.

It’s not to say, it’s time to sell.

But it is alarming how fast this decline is.

It is a sign that stock markets were priced to perfection. So any hiccup causes big drops

But sometime back there was a narrative that valuation is high because Mega 7 have very high profit growth projection.

I think Cape Schiller might be use as sensible gage. But it doesn’t always work to decide if market will go up or down.

However - agree that for stocks , valuations might be the only gage