While I’m not a portfolio manager I work for an asset manager that manages institutional money (which, you would think, is about as long term as it gets). The investments are done mostly with a factor approach and (what I would call) closet indexing (small deviations from your index are allowed/desired, occasional tracking errors may occur for a limited time, going into cash is a no-no).

If you underperform (your benchmark) for a year, you’ll have a serious meeting with your investor(s), and you better have some good explanations ready that can (seemingly) explain things.

Two years? Now you’re most likely on notice …

Three years? You’ve probably lost that investor.

Luckily, due to the index hugging, you won’t trail the benchmark by much, which (probably) delays getting fired a bit.

We know that is only your side-gig though, so my question pertains to that family office fund you manage on a full-time basis - what kind of benchmark are you comparing performance to for that? Or do you disregard comparisons with the more typical benchmarks (indices) and only look at cash flow increases etc.?

I mean, I loosely compare “my performance” to the following:

VWRL

SMI (since I have a significant home bias)

and last but not least a kind of weighted performance i.e. (my CH alloc. x perf. SMI) + (my US alloc. x perf. VTI) + (my Europe alloc. x perf. stoxx 50) + some minor others. (adjusted for currency)

2024 and 2025 have been difficult performance-comparison-wise, so I guess I’m now on notice…

Maybe ask AI for help? Upload your portfolio to Chat-GPT Gemini … actually, wait, Grok! (see above) … and ask it to explain why your active strategy underperformed only temporarily and I’m sure you’ll get a sympathizing explanation that’s well balanced, thoughtfully worded and … well, probably easy to debunk. Maybe your client(s) won’t notice.

Despite different objectives – me: steady&growing cash flow, index: Total Return (TR) – my main benchmark is still the S&P 500 TR. I used to compare to MSCI ACWI as well, but haven’t updated it in a while since I lapped it probably since the 2022 correction and I feel it won’t ever catch up again unless I have an engine failure or a tire blowing up (like 25 of my about 100 tires on my race car).

It has been a very close race with S&P 500 until April this year. Ever since the S&P 500 has left me in the dust. Well, let’s say I’m a close second in its slipstream.

If Once the AI valuations correct I expect to be passing the S&P 500 again … if not, I’ll also go to Grok and ask for a presentation why I underperformed.

I’ll then humbly appear in front of my investment committee, fresh haircut (no pun intended), freshly shaved, and will explain things as necessary …

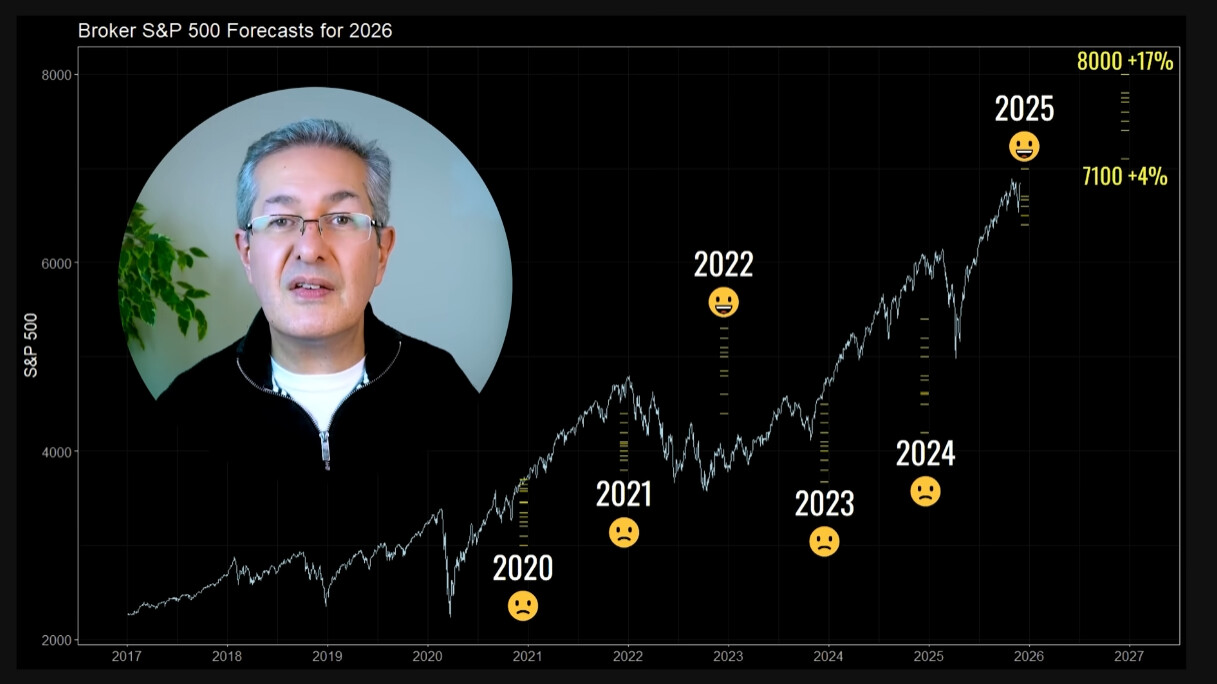

Lot of fund houses publish there long term capital market assumptions. You can read what they predict and most say that investors should expect lower returns from US stocks

Well, looking at that Chart, i would say holding cash has the same expected return over 10 years (i.e. 0%) while coming without any of the volatility of stocks. But i still cant get my head around that this correlation is as strong as portrayed in the Chart - usually nothing is that simple in the real world and for sure not in capital markets;)

It’s more or less a simple consequence of buying low vs buying high. With 10 years, you have some smoothing. When people look at the noisy days, weeks, months, you lose sight of the basic relationships.

While things are precarious, there are still potential gains left. The fact that people are still worried and thinking about a turn in the market maybe shows that we are still climbing a wall of worry. It wouldn’t surprise me if we still get 2 more good bull years.

is this with or without dividends? real or nominal? there is a big difference between 0% vs 2% vs -2% real total annualized returns over the next 10 years

I think this graph is telling different story than high PE = low future returns. It’s telling the story of the last decades of the gradual mutation of the US economy from capital intensive industries to capital light, IP based economy. (Think about outsourcing, rise of software, knowledge economy, etc..) In this new economy companies need less capital for greater profits. That’s what causing ever higher PEs. It’s unlikely that we’re going back to a world where added-value is in capital intensive industries. Demande for capital will remain low on the long-term, yet people will keep pouring money into equities because what’s the alternative ?

TLDR: We live in a world where capital is too abundant

This is almost word for word what I have seen in a video just yesterday of finance people talking about the economy/stocks in 99/2000, right just before the Dotcom bubble burst and the arguments vanished, as the stocks got pulled back down to earth.

Same arguments, “more tech, less capital requirements justify higher valuations in general going forward etc etc”

I‘ll try to find it again.

Also AI and the massive massive CAPEX spending increases happening currently, on Data Centers/GPUs, is turning these companies more and more capital intensive again.

After missing it it for 5 years in a row it seems they got it right (for the wrong reasons, as nobody could have predicted what a convicted sex offender would do) for 2025.

Prediction by your goofiest predictor? BRK will bottom the day Mr. Buffett will die. Or therearound.

As morbid as is sounds, that’d the day I’ll buy into Birkshire for my son’s portfolio.

Personally, I’d buy into BRK as soon as they’d pay out a meaningful dividend.

Want to take this to the stockpickers’ thread? BRK gets a pass for what should be considered speculation and disrespect (not paying a dividend) because of the Buffett factor premium. What are their other stats (ie FAST numbers) like?

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.