I was half joking with some contradictions, but some ETF have to be chasing these criteria…

Maybe in 25 years there would be a research paper, 99% of passive investors underperformed US bonds ![]()

P.S -: I am also passive investor

2 Likes

Exactly, you read it here first.

Which looks like a safe double bet when looking for safe haven asset class.

I am sure soon we will have a product called

Make your own ETF -: just like make your own pizza

That is exactly what I do since over a decade.

Care to specify?

I was almost serious. ETF (passive) and active investments only work if they use at least one mechanical element: money and probably position management. What happened to the clients of Peter Lynch: they lost money with a fund that made 28% CAGR over a long period of time by buying high and selling low. They were not passive at the moments that count.

4 Likes

So you meant active approach. Maybe

OK, I see. Sorry for my English, it is a bit rusty. This sentence makes no sense. Probably “… do not make money if they do not use a passive approach when it really counts”.

4 Likes

TBH you have various dividend ETFs, value ETFs, quality ETFs, yield ETFs, ETFs using joint metrics etc.

e.g. Avantis/Dimensional have some well published value+profitability ETFs, and Cambria has a total Yield ETF.

You may not like the mechanism or TER of these but there are definitely mechanical ETFs out there.

5 Likes

Yes there are, thanks for mentioning that. If you use one of those that fulfill your requirements you don’t need to build your own ETF like I do.

But still, you need a “mechanical” approach to position and money management. Otherwise you are in danger of losing a lot due to behavioral errors in key moments (buying high and selling low).

The industry term is “Systematic ETF” or “Fully-systematic ETF”.

2 Likes

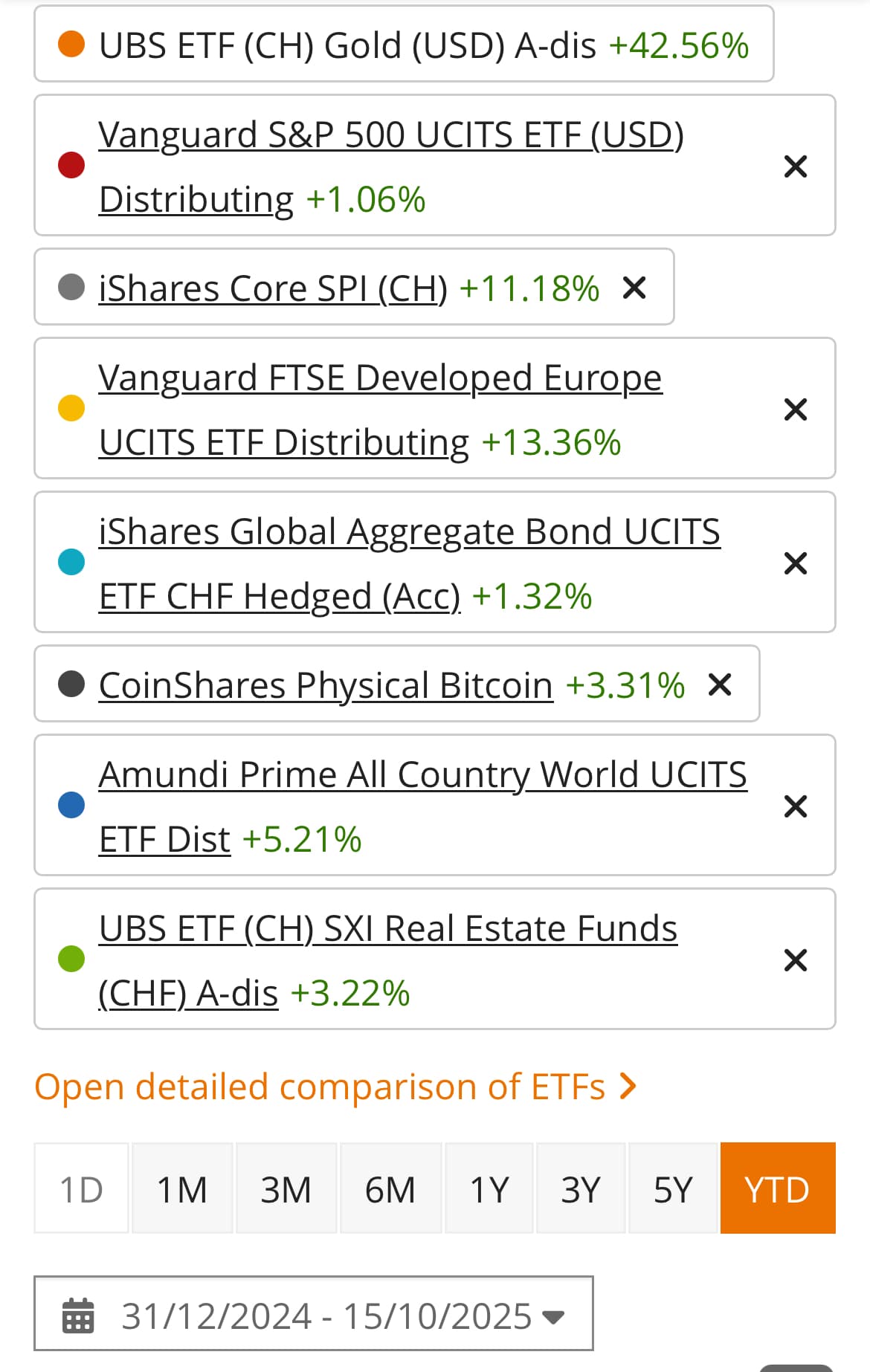

oh yes, my 3a MSCI Quality portfolio is in ±0% YTD this year, the value hedged + gold hedged + BTC + RE “crash course” portfolio is up 80% YTD - crazy.

4 Likes

Normal, so don’t act on it. But if you do 60-90% in one of your strategies, the others should do just fine. Don’t get excited, don’t get scared!

1 Like

it’s a 3a, so I’m not worried, it can run a lot more years ![]()

1 Like

Just contributing to 2025 chronicles

Swiss investor‘s perspective this year for favourite assets on this forum. Some are just proxies as multiple instruments exist for same idea

9 Likes

The Rapper 50 Cent, Adjusted for Inflation:

(The rapper will be adjusted as soon as you select a different value in the graphic.)

9 Likes

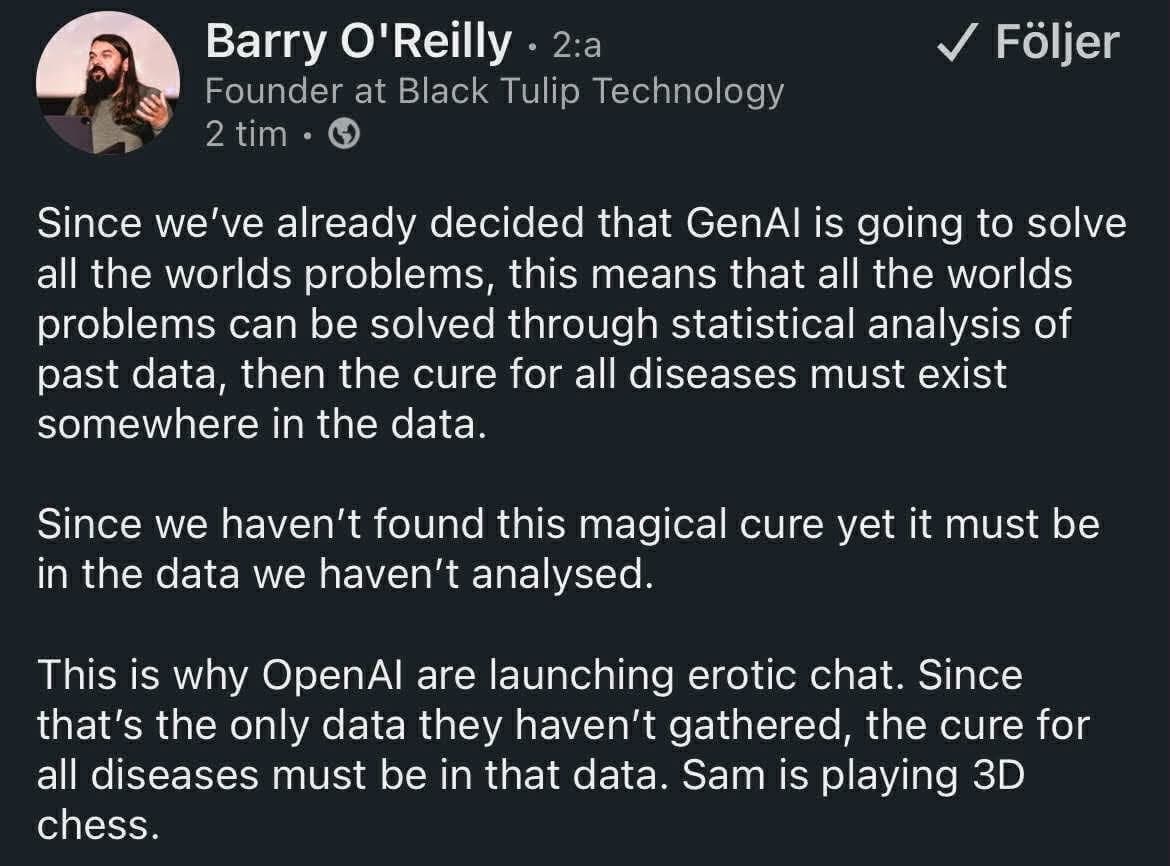

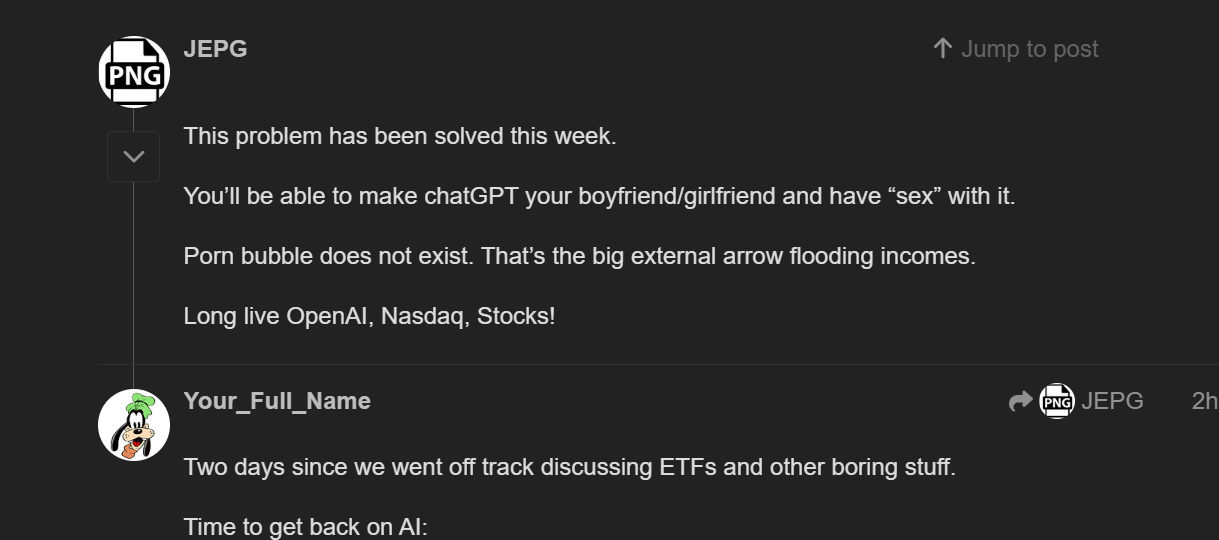

Two days since we went off track discussing ETFs and other boring stuff.

Time to get back on AI:

(via Twitter)

5 Likes

Of course the problem is solved, this time is different!

You read it here first and even liked it @Your_Full_Name!

1 Like

I did indeed which is why I replied to your post from two days ago in the first place?

The deeper sense of your new reply now escapes me, though. Please accept my apologies.

I’m such a noob. ![]()

1 Like