Following Mr. Mustachian Post advice, as a total beginner, I opened a broker account in CornerTrader. I started investing in two ETFs in USDs. In the meantime I realised that for every 10’000 CHF I transfer there, CornerTrader will take about 50 CHF for exchanging it into USD. Do you know any better alternative for online currency exchange?

+1 with Hedgehog.

After my research, these fees are not that easy to escape, it seems that at our retail investor level, only Interactive Brokers does not charge a lot for currency conversion.

-Most brokers will charge a 0.5% fee (ex : SaxoBank, CornerTrader as you say)

-Online solutions like Transferwise and assimilate seem to also charge around 0.5%

-And don’t get me started with normal retail banks. Last time i tried with Raiffeisen (a long time ago), it costed me 2% fees.

This issue is really what a lot of articles don’t talk about. But if you buy/sell foreign assets, then with most brokers you are already down 1% (0.5% at buy and 0.5% at sell). Then looking for the cheapest ETFs is not the most determinant factor.

I just went through that process a couple of weeks ago. After holding a CT account for half a year, I moved my assets to IB and don’t regret it at all (even if the user interface isn’t as easy at the beginning).

Good to know I’m not alone! Man, I wish I read Mustachian Post forum before I opened a CT account.

I’m not sure if it’s worth to move the assets as selling in CT and buying back in IB will cost a bit. On the other hand, the CT account is free, so I think I’ll just leave it there and I’ll start investing next savings on IB account.

Don’t worry, you don’t have to sell and buy again. I just transferred my VWRL ETF to IB last week without any costs. Just initiate the process in IB and then tell your account manager at CT, they are helpful with the process.For now I’ll keep my CT account open and unfunded.

an alternative would be to buy only assets that are quoted in CHF. You may incur in other hidden costs though like higher bid/ask spread or currency hedging.

Yeah, most of my portfolio’s ETFs can be bought on SIX hedged in CHF, but I guess this is more costly strategy rather than buying ones in USD via Interactive Brokers. I’m not really sure what is the exact difference though.

That’s not hedging, you’d just be buying the same paper on SIX at a price quoted to you in CHF, most likely with a higher bid-ask spread to make some profit for the market maker. You can sell it on any other exchange where it trades in respective currency, so long as your broker allows it

It has even in its name “CHF hedged”. Although I don’t exactly understand how does this work and what’s the exact difference. Friend of mine, who’s investment strategist in a private bank that I work in, just told me that if I have a choice to buy one in USD, I should get that one.

Ok, but these are not quite the same ETFs, these are different products. The way they work is they buy the same stocks plus some positions to cancel out currency effects. The net performance that you should get from it in its source currency is the performance of the target index in its target currency +/- hedging costs - TER.

AFAIK, hedged ETF usually use 1-month forward currency contracts. The cost theoretically should be more or less the difference in 1-month risk-free interest rates (like LIBOR or government bonds), plus some minor transaction costs. Let’s look at LIBOR rates, it’s easy to lookup: CHF libor has been glued to about -0.7%, USD libor increased from 0.4% early last year to 1% as of recently => CHF/USD hedge used to be free or even earned you a little bit, but now it’s definitely gonna cost you. Are you ready to pay extra to hold, what your central bank openly believes, an overvalued currency?

A problem with hedging for equities is that it still doesn’t completely eliminate currency risks. S&P 500 has, like, half of revenues from abroad in various currencies. Strong dollar => lower revenues from abroad => weak S&P => your loss with hedging. Revenue is not 100% predictable, and what complicates it even further is that companies may themselves have hedged some of it in various ways that nobody else will have a clue about, so your ETF fund manager will just do the simplest thing possible: hedge their stock prices. This problem doesn’t exist for bonds however, there the cash flows are predicable and hedging actually makes perfect sense, but you need to consider its full costs and whether they’re worth it to you.

Edit: sorry calculated wrong, negatives rates are hard. 1% - (-0.7%) = 1.7% in favor of USD, so hedging was and is still batshit expensive, you’re trading currency risk for guaranteed fixed loss

By the way, transacting Swiss exchange products in IB is more advantageous, as you don’t seem to pay Swiss stamp tax (at least I wasn’t charged for it today). That easily reduces your costs by half.

Hey Guys, one more question about the transaction costs. How to check the cheapest exchange to buy iShares MSCI World ETF in USD using IB? Before I opened IB, I bought it on SIX using CT. But I can see on justetf.com, that it’s listed in USD also on London Stock Exchange. Which one is cheaper?

Update:

It’s even more crazy. If I search for SWDA ticker, I got this:

American exchanges are the cheapest. European ones tend to be 1-2 orders of magnitude more expensive, and some (like LSE) will also hit you with a hefty stamp duty, although it seems to be now charged only for plain vanilla stocks, not ETFs.

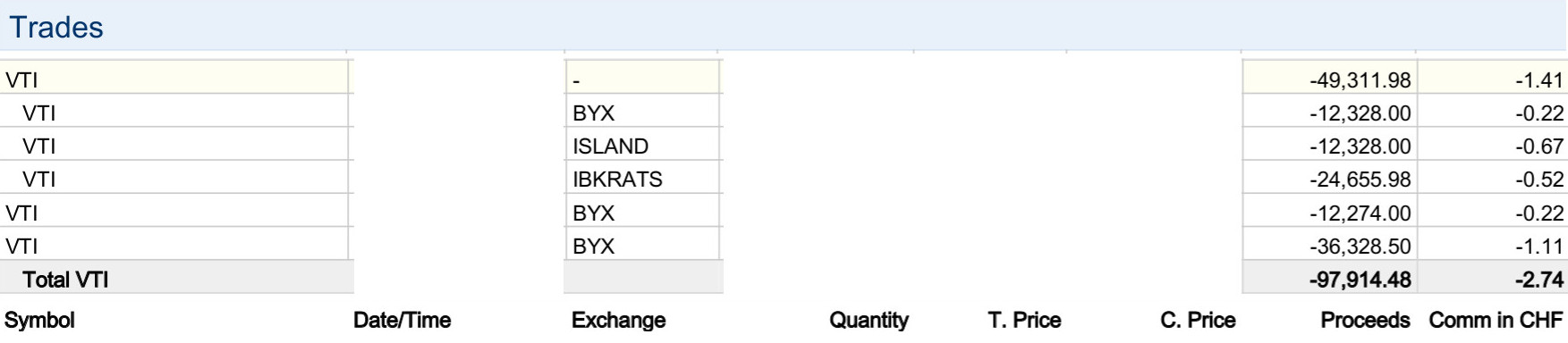

I bought $100k worth of VTI paying less than $3 in fees in total. On BYX + ISLAND + IBKRATS according to my brokerage statement. BYX (BATS) is especially cheap, they reward you for removing liquidity, i.e. if you place an order that can be immediately matched with someone from the order book, like buying at market price.

Here (some details photoshopped out, but the rest are real numbers):

SWDA/IWDA are European UCITS-style ETFs, not traded in US. An example of a US-based MSCI World index tracking ETF you can buy is URTH, but I’d rather buy a much more liquid and lower cost VT. It’s from Vanguard, which is IMHO a bit more reputable and generally less greedy than Blackrock (iShares). Here’s a list of some global funds: http://etfdb.com/etfdb-category/global-equities/. Look out for most liquid (high AUM) and low cost (TER) funds. Note that they are not all the same and track different indexes. Small caps and EM are often the main differentiators. MSCI excludes EM for example, MSCI World + EM would be MSCI All Country World.

Buying a US-based fund instead of EU is also beneficial from US dividend taxation perspective. A disadvantage could be US inheritance taxes, but for swiss residents that’s a concern starting from a net worth of several millions thanks to US-CH estate tax treaty.

Also, in the above dialogue IB is actually asking you not for exchange (it’s “SMART” - auto selection), but rather for exact product type. AMB:IWDA is traded in EUR, and LSE:IWDA is in USD, LSE:SWDA in GBP, that’s the difference. IB should route your order to cheapest exchange(s) automatically, but can’t make the decision for you which of these three currencies you want. Look at Products, Exchanges and Contracts Search | Interactive Brokers LLC or https://pennies.interactivebrokers.com/cstools/contract_info/ for details on specific IB symbols

Thanks @hedgehog for help. Now I understand. Investing in US-based ETF is really tempting, I’m only wondering what are the tax implications of that. Mr. @_MP says that you shouldn’t invest more than $60k in VT:

“I will invest up to CHF 60’000 maximum into this ETF because afterwards, the US estate law makes your heirs lose 40% of the amount invested into this fund. I will then switch to the Ireland based ETF Vanguard FTSE All-World UCITS (another option could be iShares Core MSCI World UCITS with its larger fund volume, but I prefer Vanguard that tracks the FTSE index, as it includes emerging markets).”

This is only a concern for your next of kin if you die before you manage to get rid of the US assets. Which in case of stocks you can do, like, every business day.

Then as I already said, US and Switzerland have an estate tax treaty which lifts the exemption for swiss residents from $60k to the exemption limit for american citizens, which is about $5M at the moment. We had a thread on this forum with some more details. So I’m fairly certain there’s no need to worry about it until your total wealth approaches a few millions, and then you can afford lawyers to ask about it and how to avoid it (through trusts maybe)

Also, no next of kin that you care about - no problem

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.