It can be assumed to be “equal” if all other things would be equal. Which is quite a stretch to assume.

There are many of long-running, solid and stable companies that have been paying dividends for ages. Many of them have in face been growing dividend payouts for long times. Nestlé, Unilever… Procter & Gamble has raised their dividends each year for 63 years, I read the other day. They have certainly proven great investments. And as I said: Dividends (usually) come out of profits, not losses.

On the other hand, there are tons of non-dividend paying companies that aren’t profitable, that aren’t stable, that aren’t profitable, that don’t survive, let alone grow their businesses over the long term.

Not every non dividend payer is an Alphabet/Google. In fact, I wouldn’t be surprised if for every Google there are multiple defunct/broke companies that haven’t paid much or any dividend during their lifetime.

Avoiding dividends “as much as possible” is, I believe, a pretty surefire way to load up on bad eggs and crappy investments (if based on equity (ETFs)) in your portfolio - and in the end, to me, just not good investment advice.

Minimising dividend taxation should rightly be one consideration. But it should be a means to an end (maximising returns from good investments), not an end in itself (minimising dividend taxation on dividends).

But neither should maximising dividends be the goal. Companies - or equity funds - with dividend yields that seem too good to be true should considered carefully. Because if it sounds too good to be true, it often is - and there will be a catch. That’s why “high dividend” yield stocks or a selection of such that goes “only” by the dividend criterion might a questionable investment.

I’d rather pay taxes on a good investment - than avoid them on a crap one.

Well, „as much as possible“ suggests you leave them out of your portfolio entirely …unless you couldn’t replicate certain regions or sectors …at all, in order to maintain diversification.

In any case, you must a certain idea or definition of „what‘s possible“ (while maintaining „ample diversification“) and „what’s impossible“ in this context.

So how, in practical terms, would you „avoid them as much as possible“?

You stated above:

How would you go about that? Invest in a „growth“ fund? I can imagine this would have a considerably different risk profile than a fund that full of steady and proven dividend payers.

In this thread @investorn00b was looking to invest in a high dividend yield fund…

I would suggest avoiding those for one.

I don’t believe I have ever suggested anything else, you just seem to enjoy interpreting my posts however you like rather than reading them in full.

If you really believe that all companies that pay dividends are “steady” and “proven” then by all means, go overweight them in your portfolio.

But when the $GEs with long paying dividends lose 70% of their stock price, or the $Ts stop being able to finance their dividends with excessive corporate debt you will not only be eating their losses but will have gained less from their upside as the Swiss government took a larger cut from it.

I’m hesitant to give recommendations to underweight dividend stocks. Especially as most retail investors end up worse off from trying to complicate their portfolio. Keeping something simple you can stick to in the long run is usually the best advice.

But if you really want some strategies; sure some may alter your risk profile but would you not take a 10->11 standard deviation for 6%->7% return as a long-run investor? Tbh some strategies will keep your risk profile the same or even reduce it depending on your current allocations.

You could:

Bias equities more than your mean-variance weighting in a long term portfolio as the diversifying retail asset classes are very tax inefficient (REITs or Bonds)

Bias US equities slightly more than US v International weightings due to lower current dividends in the US

Go partly in BRKA/B in place of US equities

Actively seek out high quality low/non dividend paying funds

There is a trade off in near everything with portfolio management. But if you want to build a portfolio on the efficient frontier as a Swiss investor you can’t ignore the unequal tax drag we have here compared to investors from other parts of the world. Overweighting dividend stocks is a sure way to not get there…

precious tips here but what I don’t get is the following:

Everyone advises to minimize dividends (while not screwing with one’s strategy too much) but in the end, it will be a VT or some other Vanguard ETF anyway. And every ETF pays some kind of dividends (both accumulating and distributing).

So is it worth in CH to invest passively by using ETFs like in other EU countries? Or is everyone holding 20+ different stocks in order to minimize dividends?

Noone’s doing that. The general advice I can give is just to not to focus too much on dividends because that is tax counterproductive especially in Switzerland.

20 stocks is not enough for diversification, it was not even when that famous paper which said otherwise was published in the 70s.

You could perhaps try tilting your portfolio towards growth companies (generally paying less dividends) with growth/value funds.

I think the confusing part regarding dividends is also that some ppl refers to stocks while others to ETF when talking about tax efficiency.

Imho, generally speaking in CH dividends are not tax efficient, true, however, both strategies “focus on dividend” as well as “totally avoid dividends” are probably wrong because you should not base your strategy on that, dividend distribution is only one component.

On the efficiency part, it’s true dividends are taxed in CH but:

you can find stocks that do not distribute dividends,

ETFs that track indexes/stocks without any dividend at all is hard to find.

Therefore, if you invest in individual stocks (not arguing here why you shouldn’t) it may make sense trying to avoid dividends, but if we are talking about ETF you will almost always have dividends coming out from your ETF, whether distributing or accumulating, but that does not make a difference in CH from tax perspective (e.g. same amount of dividend will result in the same taxation whether is distributed or accumulated), so look at the overall performance of the ETF, its costs, its composition, etc.

I read the stuff but starting loosing energy of reading the same thing multiply times regarding dividend paying stock vs whatever else for swiss investors, losing the point of the case if the withholding tax was the only and ultimate decision driver of investing.

I believe this question can be answered based on individual circumstances. But more important would be to know the Holi Grail of other questions such as:

Why you absolutely must invest in stocks if you are aiming for wealth building and a predictable passive income stream.

How you should limit the universe of stocks from tens of thousands, to a few hundred candidates which have the characteristics that are proven to drive superior performance.

How to tell which of these top quality candidates are available on the cheap, thus offering a turbo boost to your returns (aka the double-dip benefit).

What absolute threshold criteria you should set before putting your money into any investment.

How to rank the stocks (or else) that seem to have it all: both top quality and attractive valuation.

What other aspects to examine before committing your capital to a promising investment candidate.

I hope I am provoking enough but not hearting anyone’s ego

Oh, I get it then people just do not follow those smart and famous ones otherwise I dont understand.

“By a continuing process of inflation, governments can confiscate, secretly and unobserved, an important part of the wealth of their citizens. […]

The process engages all the hidden forces of economic law on the side of destruction, and does it in a manner which not one man in a million is able to diagnose.” John Maynard Keynes

So not the tax but the inflation will eat up your welth

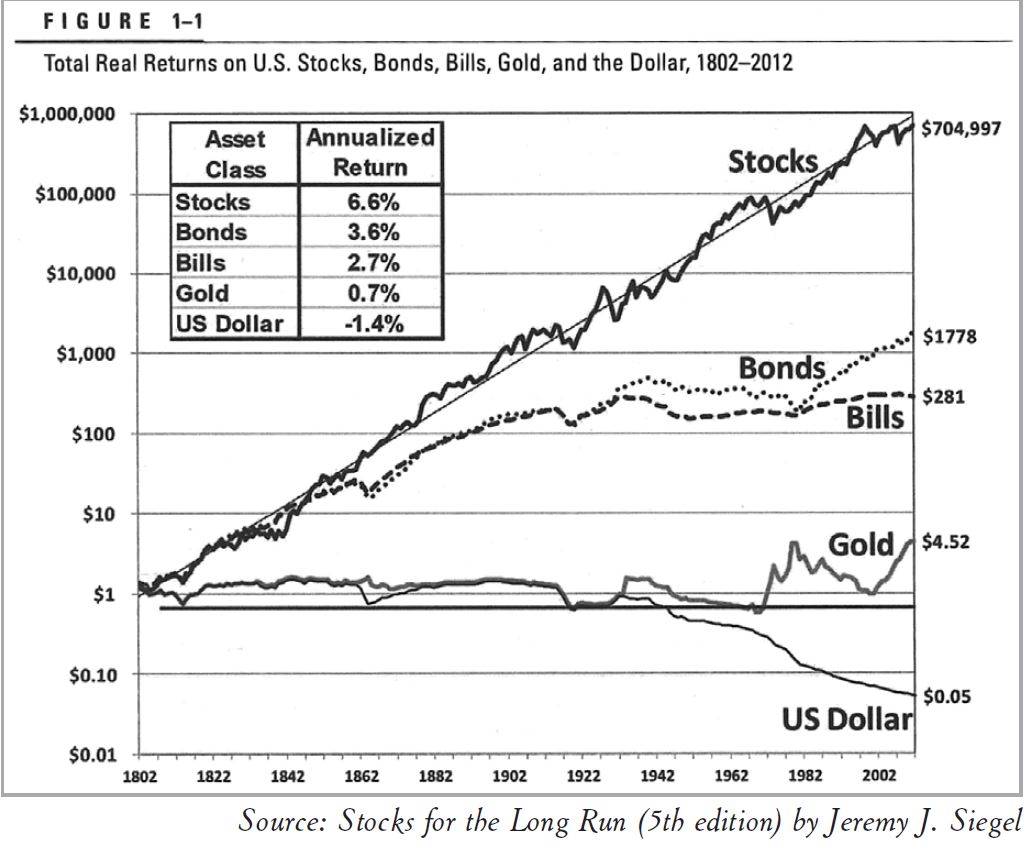

According to another smart guy, Professor Jeremy Siegel, The ranking of the world investments are the following:

In between 1802 and 2012 (including the latest recession dip 2008)

1 Stocks

2 Bonds

3 Bills

4 Gold

5 USD and this one gives out a negative result

Note that investing 1 dollar in the stock market multiplied your purchasing power by almost 705,000 between 1802 and 2012, while the second best asset (Bond) only had a multiple of 1778. A huge gap indeed!)

And what is n ETF? A random mixture of those above.

And if is so then the stock is ahead by far…

I am not sure about that VT

Yes, you are right, all world and most probably we do not know everything about the whole world at all times. Those VT / ETF call as you like, include everything. But we don’t need everything in order to build wealth, diversified portfolio which delivers passive income. However those ETFs include those investments you probably would not keep if it was you to tell.

Investment possibilities are both many and varied. There are three major categories, however, and it’s important to understand the characteristics of each.

Investments that are denominated in a given currency include money-market funds, bonds, mortgages, bank deposits, and other instruments. Most of these currency-

based investments are thought of as “safe.” In truth,

they are among the most dangerous of assets. Over

the past century these instruments have destroyed the

purchasing power of investors in many countries, even

as the holders continued to receive timely payments of

interest and principal. This ugly result, moreover, will

forever recur. Governments determine the ultimate value

of money, and systemic forces will sometimes cause them

to gravitate to policies that produce inflation. Current

rates, however, do not come close to offsetting the

purchasing-power risk that investors assume. Right now

bonds should come with a warning label.

The second major category of investments involves assets

that will never produce anything, but that are purchased

in the buyer’s hope that someone else – who also

knows that the assets will be forever unproductive – will

pay more for them in the future.

Owners are not inspired by what the asset itself can produce

– it will remain lifeless forever – but rather by the

belief that others will desire it even more avidly in the

future.

Our third category: investment in productive assets, whether

businesses, farms, or real estate. Ideally, these assets

should have the ability in inflationary times to deliver output

that will retain its purchasing-power value while requiring

a minimum of new capital investment.

Whether the currency a century from now is based on

gold, seashells, shark teeth, or a piece of paper (as today),

people will be willing to exchange a couple of minutes

of their daily labor

Our country’s businesses will continue to efficiently deliver

goods and services wanted by our citizens. Metaphorically,

these commercial “cows” will live for centuries

and give ever greater quantities of “milk” to boot.

Their value will be determined not by the medium of

exchange but rather by their capacity to deliver milk.

I believe that over any extended period of time this category

of investing will prove to be the runaway winner

among the three we’ve examined. More important, it will

be by far the safest.

The assets within this third category have the highest probability to preserve and

grow your purchasing power. Risk is the probability of permanent

capital loss and has nothing to do with the price

fluctuations of various investments.

I honestly don’t know what is the message you want to deliver. I do, however believe that you are missing the basic understanding behind index fund investing and using ETFs as a vehicle to do this. A good start would be this article:

Jesus christ are you hard to read.

Please shorten your messages and give them a point.

It is very well known that a vast majority of professional stock pickers cannot beat the whole market altogether.

Why do you think you could? And do you have all the time in the world for all the necessary analyses; and then to still fail with a high probability…

That is why people choose ETFs - because they are simpler and less stressful to manage, and have historically worked better for the common individual investor.

The advice for you is very simple then: ignore the dividends.

Many people focus on dividend paying companies because of the feeling of extra safety that dividend gives. Cash is king, companies being able to pay and grow dividends are better regarded and statistically fared better, so “Dividend Growth” is a common investment theme in the US. But it’s still a form of active stock picking and due to tax differences between US and CH it is counterproductive in CH.

So, simply do not think about the dividends, focus instead on total after-tax return. Or simple broad market index funds if you will.

Ultimately dividend is just money being moved from one pocket to another - to shareholders’ accounts from company accounts and the company belongs to the shareholders. With government taking a cut in the process. Total after tax return is what ultimately matters, not dividend.

I don’t think it’s hard or unlikely to beat the market by stock picking. It’s just very, very hard and unlikely doing it in a well-diversified fashion. Which is what many of the professionals are employed to do: making diversified investments.

Once you let go of the idea of “building a very diversified portfolio” and concentrate on finding the next '09 Apple stock about to take off, you might easily beat the market - though at the same time run a relatively high-severity risk in focusing on just one or a few stocks.

OK, my short message is that “buy dividend paying stock” rather than ETF-s . But if this would be just that easy and symle then a large population of the earth would be already very rich regardless which of the two they follow.

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.