On running the numbers maybe I used a number too high here. I see for CHF100k taxable as single person 30% marginal Zurich, 37% Vaud, 38% Geneva, 33% Bern.

Anyway, paying tax at marginal rate on returns is never great compared to paying 0% for capital gains.

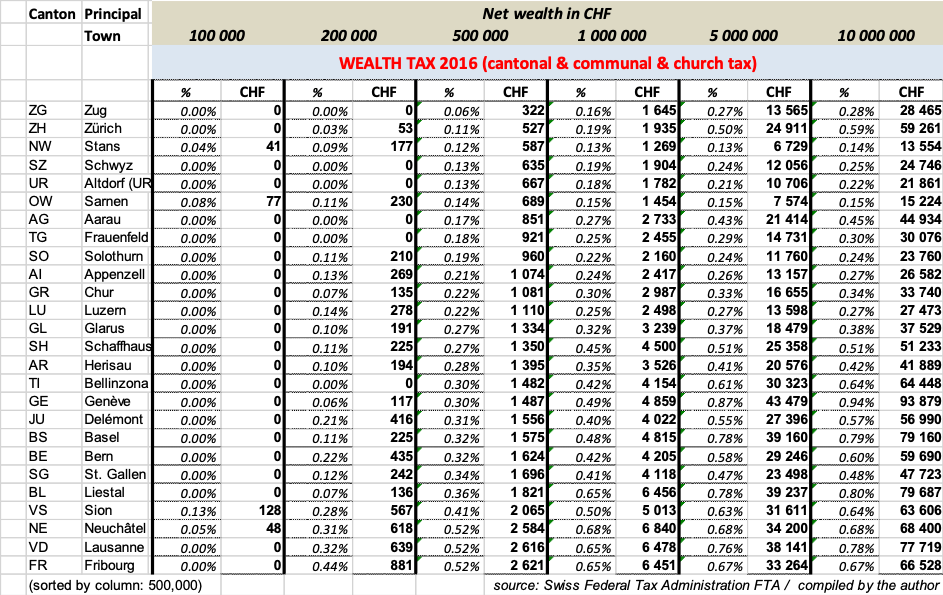

Was a rough approximation because will vary a lot on a case by case basis. But if we assume long run target of CHF2m net worth, take the mid at CHF1m we can see that in 2016 tax rates ranged from 0.16% to 0.65% depending on canton.

VTI includes US small cap.

VXUS includes ex-US small cap.

Adding any additional small-cap specific funds would result in portfolio overweight in small-caps.

This could be a really great solution to effectively diversifying across asset classes as a Swiss investor.

Do you know of any good solutions here? i.e. 3a offering REITs, low TER.

Currently all my 3a is in VIAC equities as everything else seemed pretty abysmal.

Looking at this in a bit more detail - I see with VIAC you can create a custom investment strategy allowing up to 30% real estate exposure. I assume regulations don’t allow higher.

A max of CHF2k investment into a REIT a year won’t be sufficient for most as a portfolio volatility reducer.

I think that’s very good tax advice. Yet very questionable investment advice (in the meaning of the word).

Because yes, from purely a tax perspective, you should avoid dividend distributions. And while I would agree you should take tax considerations into account when investing, that shouldn’t be the only one.

Much of your advices hinges on the assumption of “all returns being equal” - which I think it isn’t. For instance, dividend paying companies are, much more often than not, profitable. Especially if they manage to grow their dividends. Non-distributing companies are… well sometimes, sometimes not.

I’m not getting it!? That table shows wealth tax on wealth tax.

How does that pertain to your original statement regarding dividend taxation (emphasis mine):

Dividends are taxed through income tax.

How are they specifically taxed by wealth tax in a way that capital appreciation is not?

I disagree and it has been demonstrated multiple times that the dividend yield has no impact 8or even negative) on the total return.

One short exemple:

MSCI World high yield has a lower annualized total return that the MSCI world https://www.msci.com/documents/10199/74fe7e16-759e-405c-96aa-8350623fae65

Looking at that chart: Just exclude financials (primarily banks), and I’d bet the dividend-paying stock would be outperforming.

EDIT: On second thought… maybe, maybe not. Maybe it’s just me, but from the looks, it suggests the HDY index does outperform for in upward trending markets - and underperforms at the tail end of them, and in downward trending markets.

Sure - I’m not advocating avoiding dividend paying companies altogether else you miss out on large sectors of the market. My feedback here was based on investorn00b’s portfolio which looks to overweight dividend paying companies.

All returns are equal in the sense that a company chooses how to return value to its shareholders, through dividends or alternatives.

I haven’t seen any full analysis on returns of dividend companies vs non dividend paying companies but I’d imagine this fluctuates by temporal trends more than anything and in the long run is irrelevant.

I would be very surprised if dividend paying companies have had higher absolute returns than non-dividend paying companies over the last decade. The large tech stocks which have led the market (Facebook, Amazon, Google) do not pay dividends and have contributed the most to recent stock market growth.

Though I fail to see the point regarding dividends and wealth tax? Whether it’s capital gains or dividend income that’s still on your accounts - it doesn’t make a difference with regards to wealth tax - or does it?

Except for the psychological pitfall of higher temptation for me to spend cash

If you’re employed, many 2a funds seems to have a very large portion of real estate in their portfolio, so there’s a good chance you’re already well covered.

Thanks a lot all who replied so far, it’s being a really nice discussion and definitely a lot of learning (at least for me as I have less experience than most of you). Here replies to some previous points:

I have read different things (in this forum and somewhere else) so, since I may have got it wrong, here is my understanding as I also wrote on one of my previous replies:

For funds registered at ICTax, The Swiss tax authorities will tax distributed dividends, but also the value appreciation part that is caused by accumulated dividends.

this means that whether that dividend sum is distributed to you or accumulated in the fund, will get taxed anyway and in the same way

In case the fund is not registered at ICTax, they don’t know which part of the value appreciation is caused by accumulated dividends and which by increase in value price (capital gain, which is not taxed), they will tax the whole appreciation.

TL;DR Given the above, Dist vs Acc it doesn’t matter from tax perspective. Did I get it wrong? (I fear the answer is yes, but better ask)

The ratio 25/10 is not that specific or scientific, but the choice of VOO+VB instead of VTI is because VTI has very small exposure to small-cap, 5.47% according to MorningStar. Probably my 25/10 does not reflect the marked distribution so probably should rethink this as well.

Well, QQQ is not full tech despite what many tend to believe. To be precise is “only” 56% Tech, but has also pharma/healthcare, consumer defensive, etc.

Agree, thanks a lot. I’ve realized EU weight is too big. And I had overlooked the overexposure to Australia and HK. I will look for one only European ETF and review the Asia (ex Japan) one.

This is the thought I’m having in the back of my mind too… I think I will probably keep a small amount to invest directly into stocks.

So I did read the first study that I came across, and lo and behold…:

“an emphasis on stocks with high dividend yields, and on those with a history of growing their dividends – have produced higher returns, with less volatility, than the global equity market, resulting in higher risk-adjusted returns”

(no, I didn’t miss the limitations and explanations they give)

I did work out the numbers for one or two I had from their annual reports (and the tax authorities’ guidance "Besteuerung kollektiver Kapitalanlagen und ihrer Anleger) for a couple of years, and declared them myself. Never was I questioned about them. But they probably just didn’t bother about me.

Otherwise, I concur with the assessment that all other things equal, it doesn’t matter if an equity ETF is distributing or accumulating.

Yes, your WEALTH is subject to wealth tax. But you were saying that dividends are subject to wealth tax. They aren’t. If you claim that dividends are subject to wealth tax, then capital gains are even more subject to wealth tax so even worse OMG more tax because of capital gains dividends are better?

Not more than capital gains of course but since they add to your wealth they are taxed the same. He just means they also have an extra tax on top of wealth tax.

As @Gesk mentioned in the post above, I am just trying to convey the additional tax drag on dividends. There is wealth tax on both capital gains and dividends.

Lets take an example:

CHF100k income in a high tax canton; so we’ll assume 35% marginal income tax rate

CHF1m portfolio and no other assets (house, cash, car); so we’ll assume 0.5% wealth tax

Now lets compare the two extremes of a portfolio:

Portfolio A: CHF1m in high dividend portfolio returning approx 6% in dividends a year and no capital appreciation

Portfolio B: CHF1m in a no dividend portfolio returning approx 6% in capital appreciation a year

Ignoring any income or wealth tax on our income and portfolio wealth, what is the additional tax burden we have from our 6% return?

Portfolio A (6% Dividends)

We get CHF60k in dividends paid to us

At the end of the year, we declare our wealth of CHF1.06m and income of CHF160k

Our additional tax burden on the CHF60k is:

Income Tax: 35% * CHF60k = CHF21k

Wealth Tax: 0.5% * CHF60k = CHF300

Total additional tax burden = CHF21,300 Net return from 6% portfolio appreciation = CHF38,700 Note: we may lose more to WHT if fund is not held in a swiss-tax friendly domicile so we could lose 0%-30% more here

Portfolio B (6% Capital Appreciation)

Our portfolio appreciates CHF60k from CHF1m valuation to CHF1.06m valuation

At the end of the year, we declare our wealth of CHF1.06m and income of CHF100k

Our additional tax burden on the CHF60k is:

Income Tax: 35% * CHF0 = 0

Wealth Tax: 0.5% * CHF60k = CHF300

Total additional tax burden = CHF300 Net return from 6% portfolio appreciation = CHF59,700

For all sakes and purposes whether a company returns value to a shareholder through capital appreciation (share buybacks or internal investments) or paying the shareholder directly (dividends) can be assumed to be equal.

However, as a smart Swiss investor you would avoid dividends as much as possible while maintaining ample diversification because we are exposed to this unequal tax drag.

I don’t recall OP mentioning he wanted to overweight small-caps in his portfolio. Exposure yes, overweight no.

And overweighting small-caps is generally a good strategy to achieve identical returns in the long run but expose yourself to higher volatility with unequal weightings yes.

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.