I was reading a blog post from Mr.RIP about the swiss pension system and stumbled across this interesting snippet concerning pillar 3a:

Can anyone shed some more light on this? I have never heard about this before. does your tax bracket determine the amount that “makes sense” to contribute to 3a and get the max deduction (a break even for tax deduction if you wish).

how much is the reduced rate mentioned for the 768CHF @ 33.3 tax?

My situation is as follows: taxable income was 40’000 CHF last year (nettoeinkommen) and I was taxed 3500CHF resulting in a ~11.43% tax rate.

So following that would it only make sense for me to contribute so much into pillar 3a that would result in a 773.58CHF deduction from my taxes (6768*12.43%).

This would result in me only contributing ~5400chf to reach that deduction.

Tax is a continuous progression, so I don’t understand the argumentation about 6000 being more of an optimum than the maximum (6768).

But anyway for your very low tax rate (~11%), I would not bother with 3a. You gain little but lose flexibility in how to invest your money for many years and are charged higher fees (even with a Viac or similar).

Wait for a tax rate of >20% or even 30%. That’ll come soon enough when your income goes up

For example, I am able to deduct more than 30% of my 6768, but I live in tax hell.

For me this is jibberish. My simple rule is to contribute to third pillar to the maximum legal amount if no better use of the cash is possible. If you contribute more than the maximum you have no deduction when you contribute but you get taxed when you take your money once you are over 60 and want to retire.

The only advantage I see about contributing more to the third pillar than the maximum is avoiding wealth tax but I guess this is not relevant for most people.

To be honest in your case with 11.43% tax rate I even find a third pillar marginally attractive, especially if you are young and the TER of your third pillar is higher than 1%.

Don’t bother with pillar 3a then. Better get a real job instead

When you withdraw there will be 5-6% tax (in ZH), so you’re gaining only 5% for the privilege of having your money locked up for many years in suboptimal funds.

Now, if you were paying 40+% marginal tax, then even if all the fund did was hold money in cash, you could still walk out with a respectable profit after a few years

I stated taxable income for a reason. I have a lot of deductions and work part time at the moment. My tax will very likely increase soon and fast.

So in nuggets 3rd pillar thread we discussed that using viac and getting market returns with their funds, paying their 0.53% fees is worth the tax deduction you get.

The questions comes down to if you think that can be achieved or not with the forced 37% swiss stock allocation.

Lets say I have no issues with 6768 being locked up p.a.

I was wondering if anyone could shed some light on the stuff mentioned by Mr.RIP, is this something worth considering?

I am looking at these 3 options:

no 3a

max out 3a (viac)

find “optimal” amount to contribute (5400-6000CHF, viac)

determine what level of tax savings you want - what’s the minimal percentage of your investment in exchange for which you’re willing to lock the money up in pillar 2/3 schemes

add approximate withdrawal taxes to it (e.g. 5% in ZH)

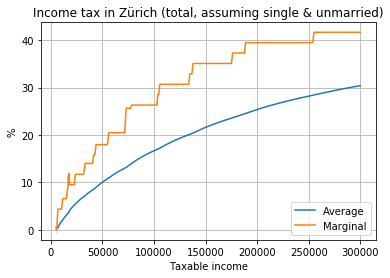

find where it crosses the marginal tax line on chart and invest until you taxable income is at this point or you hit 6768 CHF limit (note the above chart is for Stadt Zürich, YMMV, I could share a notebook that can make you that chart for other parameters in ZH if you want)

Two most likely solutions are invest none or invest all, just like with choosing health insurance deductible - due to the rather constrained decision choice the optimal solution would likely lie at the boundary of your decision space.

There’s more freedom with pillar 2 though, but there there’s the consideration that you’re better off splitting a big contribution over multiple years

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.