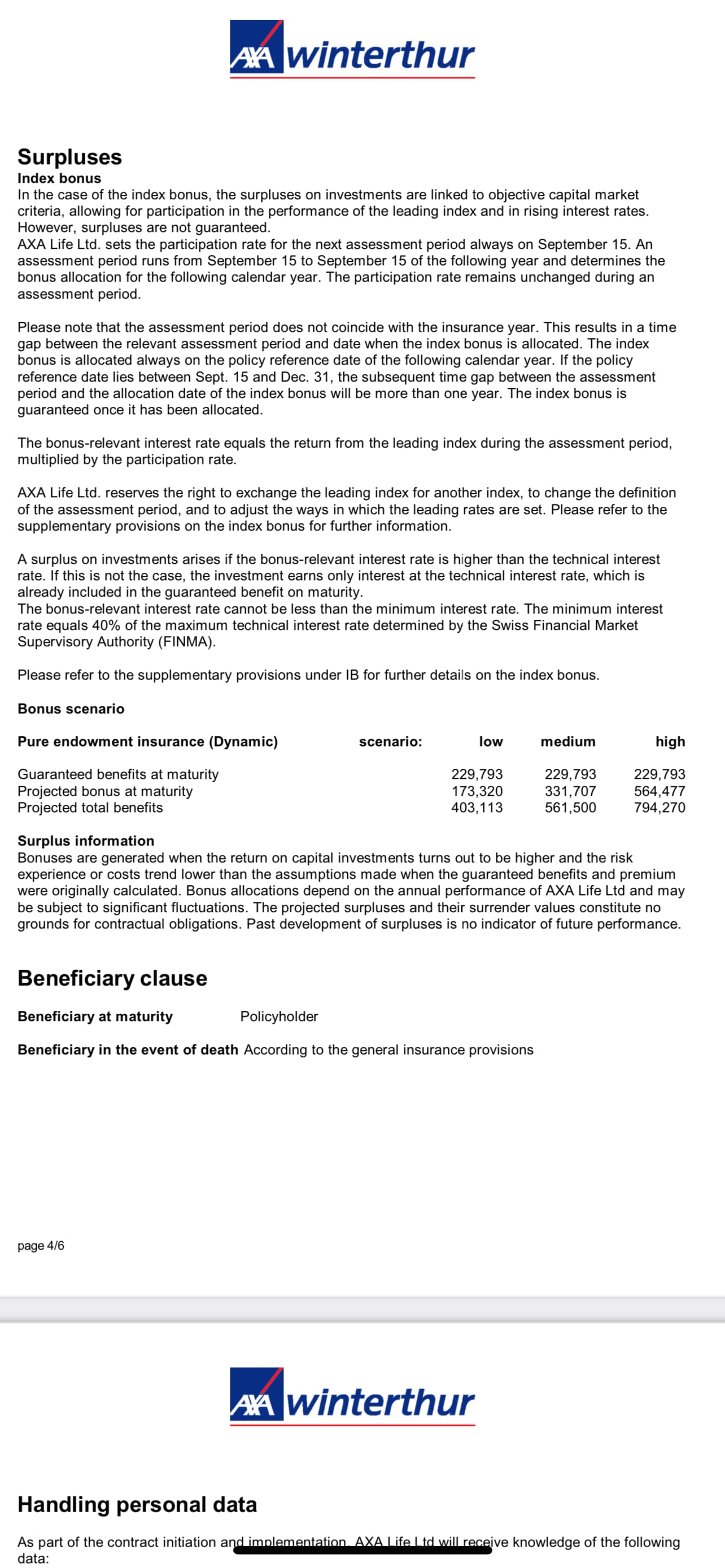

I asked this before as well but I think I understood now more clearly about my 3a with AXA with life insurance. I took this from a broker and he never explained what we will get at the end. My assumption was that I am putting 3a amount in the AXA and which is taxable and I will get projected benefit as you can see in the picture below but now I know that after paying for 6 years full amount I will get 23000 surrender value so I am

Loosing almost 22000chf.

I am actually panicking. Please don’t judge me. I am equally guilty in trusting someone and not checking the numbers as I thought my partner will do that. Turns out we both didn’t understand what broker was hiding.

Okay so my questions and suggestions I am seeking on are for below:

Should I continue as I get this 0.5% bonus?

Should I ask to pay minimum and continue with this protect dynamic plan?

If I continue what would be my loss apart from this 22000chf ? And if I stopped what would be my benefit?

How a life insurance will benefit me?

Should I exit with the loss?

Is there a way I can ask AXA to cancel the contract? I actually change the contract from Broker to AXA just now. So my account is with AXA now. I don’t know how much this will help.

I am really looking forward for suggestions. . I am really tense and stress thinking about this as I was totally unaware of what’s happening…

it’s a hard earned money .

Is there any way exist I can get the whole 6 years amount?

We‘ve got several threads about these 3a life insurance products on the forum.

To make it short:

You‘re unlikely to get your full deposits back unless (you can prove that) you‘ve been misled by the insurance or broker.

If you‘ve got 20+ years until retirement, quitting the contract and accepting a loss will probably yield a higher return in the end, if you invest into low-cost index funds instead (do make sure to check which coverage you lose, get or need if you feel you need it).

Without knowing your particular plan/scheme, continuing it with minimum payments will also most probably not be worth it. Though that often seems what they‘re recommending instead of cancelling.

Personally, if I don‘t reasonably understand an investment product, I would get rid of it as a matter of principle. And precaution.

If the calculation of future projections isn‘t strictly regulated by law, I would be astonished if the „high“ wasn’t unrealistically high. Even the „medium“ return scenario may be very optimistic.

I am still digesting this as how my all degrees and experience was all in vain as I never tried to understood the numbers. Anyways .

AXA is telling me that to keep this as I am getting 0.5% interest and this interest can increase in future and if something happens to me than my kids or spouse can get the money.

Don’t know what should I do? I am in dilemna.

Just trying to understand if this is really a bad deal. What you all think?

May I ask you which low cost ETFs you are talking about? Do you have these from IBKR or banks?

As said many times: I was there too, degrees and all. Cancel it and never look back. I did a few years ago and it cost me ca. 15k. I have made it back already on performance by investing my 3a in passive funds through VIAC.

There is no silly post. You were brave enough to create this post and ask someone for another opinion. You should be proud of yourself! Finding out that you didn’t understand the contract can be a hard pill to swallow, but it’s good that you did. From here on, it can only get better

I don’t really see those numbers in the picture, only the end amount. Anyway, if you paid 6 years full amount (for simplicity we take CHF 6’883.- per year, it was lower before 2020) that would be CHF 41’298.-

If your surrender value is CHF 23’000.-, you “only” loose CHF 18’298.- Where did you get the 22k from?

Most probably (we’re talking 99.99%) not. If you check the original contract, there will be a page about surrender values in case of early cancellation. Unless the amounts on this page are very different, I don’t see any option to get back more money. You’ll definitely not get back all of the money.

It is a bad deal. Think about it: if you cancel now, you’ll loose several thousands. How can that NOT be a bad deal?

You can do yourself a favor and just run the numbers. I used this compound calculator, but you can use any compound calculator. Base assumptions:

20 years until retirement (I don’t know your age, adjust as you wish)

CHF 6’883 annual contribution = CHF 573.5833 per month (for simplicity, I used 573)

0.5% with AXA vs 5% for global stock market funds

AXA: contributions = CHF 137’660, end amount = CHF 151’857, total gain of CHF 14’197

Stock market: contributions = 137’600, end amount = 245’624, total gain of CHF 108’204

If you have more years until retirement, the gap is even bigger.

Others already recommended finpension, VIAC and Frankly

Even though I believe it would probably be preferable to cancel (if you’ve got 20+ years of investments ahead), I agree with @ProvidentRetriever not to rush it.

0.5% interest is good in the short run.

Or if you’ve got obligations to pay.

Over the long run though, it’s a a very meagre return.

Well that’s a very goood suggestion and thank you for being so kind on my questions.

Means a lot .

Any recommendations for any financial advisor to consult?

Also I was 26 when I started with this contract. I have quite some years left till my retirement. I agree with you about investing in other places.

That guy will contact me with proposal next week. Let’s see what will I do. But I think I will cancel it but loosing this much money and also penalty is making me more stressed as it is hard earned money .

For now I am not in that state of mind as I was when I agreed with this broker but now situation is different. I have woke up by reading posts here in MP group and I am thankful to you all.

I agree that I should think about future. Your analysis helped me to evaluate few things before I sat with AXA and make a decision.

Actually it’s not one contract… my spouse also signed one with another provider… and you would not believe this broker remove the disability from the contract. We get to know this from Swiss life… .

First off, your feelings and emotions are valid. It is a significant amount of money and you probably need time to trust a new plan to provide for and protect your family. As others have stated, your intent is good and the lesson comes early enough. It hurts right now but it could have costed way more if it had happened further down the line.

Then, the harsh truth: that money is already lost. What matters is what you and your partner do moving forward. Your family is alive and well, you have income coming in and are set for saving a bunch more in more efficient vehicles going forward. It will take some time to realize, which is fully normal, but you are probably in a good position.

After having reassessed the needs of my family for additional risk coverage (death and/or disability), I would also give some thoughts at some 3b policies: I haven’t checked of late but have heard it’s possible to cover both partners with only one policy, which could be a better option than two separate contracts, or not.

I’d steel myself and fish around for:

a risk only insurance policy (be very clear and very firm with whatever agent/broker you’re talking with that risk is all you want to cover and you absolutely don’t need nor want a savings/investment/mixed solution), provided you conclude that you still need one.

an investment solution for your 3a retirement savings (VIAC, Frankly and Finpension have already been named, you can have more than one account and use more than one of them if you want - as stated already too, be sure that you understand the risks involved with investing in equities and to choose an allocation that you are comfortable with, or use a low equity solution like VIAC’s 3a Account Plus (5% equities, 95% cash) or a simple bank savings account if you are not at ease at all with the concept of your investments loosing even the tiniest amount of value.

You are doing good, the path will become clearer with time and research. Keep going.

Hi All, coming back to this AXA 3a topic… I just started dealing with all the financial stuff, like investing, budgeting, buying my first ETFs and checking out my situation regarding insurances etc. and I am a complete newbie in these topics and I would need your advice.

I started a 3a plan with AXA in 2020, it’s called smart flex… Actually I wasn’t aware that it is some kind of life insurance… call me ignorant, but back then I had less clue than I have now… But the conditions sound good to me, so that’s why I am reaching out to you and get your opinion if it is really a bad deal and if I should try to get out of this as I am only paying since 2020.

I pay the full possible amount each year and this is split 10% in a traditional savings account with 0.5% interest and 90% into a global fund (AXA (CH) Strategy Fund Global Equity CHF, CH0457194931). They claim Investment costs of approx. 0.50% on the fact sheet.

I just changed recently to 10 / 90 split, before it was 50/50. So currently, my balance is around 15.000 CHF, they currently project an amount of CHF 463’011 by 2050, based on fund performance.

Current surrender value / Liquidation value: CHF 9,639.

So not sure what the difference would be if I would move to another fund-based 3a like VIAC? I do plan to open another 3a account (or more) at some point going forward to save taxes in the future when I receive the money…

Looking forward to hearing your thoughts on this as I didn’t read about this fund-based 3a AXA thing from anybody else here…

Right, so the surrender value would be applicable if I would end the contract before the official termination in 2050, correct? So if I would continue this contract as planned, I would receive the full projected amount and as the money is invested in a global fund with a certain performance higher than an usual interest rate, the “only” risk for me would be to terminate the contract before, e.g. if I would leave the country, or would need money to buy a house, etc…

Do you still consider this as a reason to terminate now and loose some money, but also getting rid of the contract? My financial situation is quite good, so of course it is not nice loosing 6k, but also I can survive that if it is really worth getting out of this.

Thr problem is, longer you wait, more you lose in opportunity cost - what would you earn with your money if you would have invested it with a good 3a provider. However most complaints are about 3a life insurance, maybe for once you indeed just have a shitty investment fund?

In addition to the point made by nabalzbhf (CHF 9,639 != CHF 15’000), the fund hedges developed market equities in CHF, which, on the long term, should carry an aditionnal cost (drawing down the performance).

Other than that and if there are no other fees, it doesn’t look like the worst solution out there if you also need the life insurance component. The question would be: do you really?

What performance are they using for their projection?

By reading and partipating to this forum, you confirm you have read and agree with the disclaimer presented on http://www.mustachianpost.com/

En lisant et participant à ce forum, tu confirmes avoir lu et être d'accord avec l'avis de dégagement de responsabilité présenté sur http://www.mustachianpost.com/fr/

Durch das Lesen und die Teilnahme an diesem Forum bestätigst du, dass du den auf http://www.mustachianpost.com/de/ dargestellten Haftungsausschluss gelesen hast und damit einverstanden bist.

And if I stopped what would be my benefit?

And if I stopped what would be my benefit? . I am really tense and stress thinking about this as I was totally unaware of what’s happening…

. I am really tense and stress thinking about this as I was totally unaware of what’s happening…