Are you sure? It looks like a life insurance to me, especially because you have the contract with AXA Life Ltd.

Did you cancel the contract now?

Are you sure? It looks like a life insurance to me, especially because you have the contract with AXA Life Ltd.

Did you cancel the contract now?

Well they told me to wait till September as they have new plan coming so I am waiting what they will say. So I couldn’t cancel.

And AXA told me it’s a saving plan and not a life insurance.

I hope they told you so in writing. Because then you can try to claim that you were falsely advised and request reversal of the contract without a penalty.

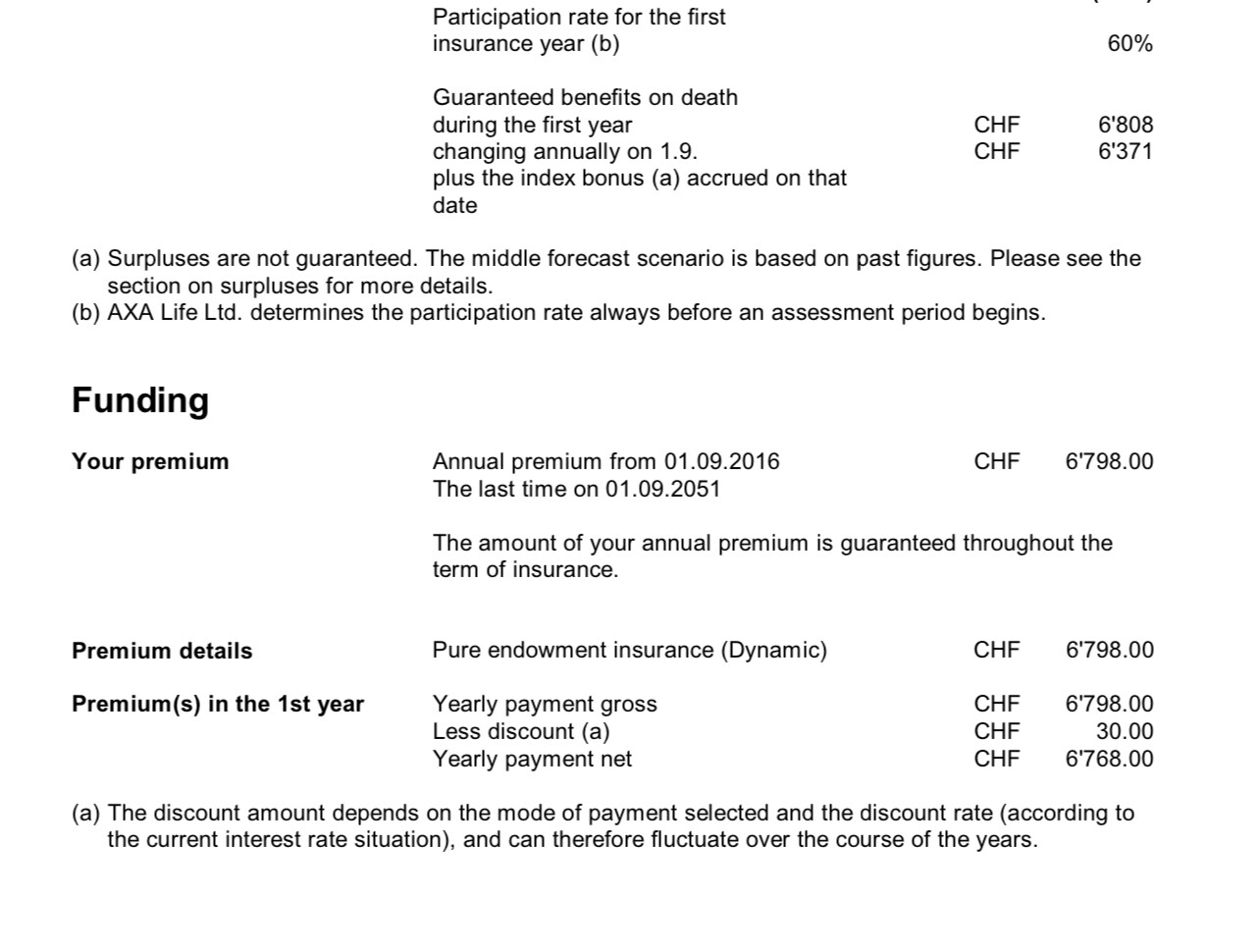

No they didn’t. ![]() They said look at your contract. I will get just nominal if I die now (honestly a part of me died there when I heard this, all that trust in that agent left me in tears). See the attached pik which he referred.

They said look at your contract. I will get just nominal if I die now (honestly a part of me died there when I heard this, all that trust in that agent left me in tears). See the attached pik which he referred.

What’s the name of the product exactly?

Yep, normally you should have filled out a protocol while he advised you. If it said somewhere you wanted a life insurance and not a savings plan, you could go for it.

Seems to be largely a savings plan with no or little life insurance component (unless you opt for one). So did my contact at AXA tell me. I’m still not 100% sure if you can choose no insurance component whatsoever - but then, even VIAC has got one built-in.

It certainly doesn’t seem that bad an investment.

Though still don’t quite get why one commit to a 35-year contract to invest largely in low-cost index-like funds (as in: reasonably low-cost but not as low-cost as others) at reduced early surrender values when you one do the same without such commitments.

Edited because of outdated information.

That’s not true. I work for an insurance company and we have 3a products not linked to any insurance at all.

Also look at the produxt that San Francisco linked above from an insurance company, it doesn’t have any insurance, it only has a secured part, the underlying is probably a structured product.

Are you sure about that? I used to have a 3a Start account through Swisslife, which is a (fee heavy) banking solution they offer by partnering with Lienhardt & Partner Privatbank Zürich AG.

An insurance can sell banking solutions and act as an intermediary, I’d expect some policies to look like that.

They (sometimes) are: Swiss Life Hypotheken: Vorteile, Laufzeiten, Zinsen | Swiss Life

Meant insurances, not mortgages.

Anyway, I edited my post.

A related topic: https://forum.mustachianpost.com/t/bad-investment-choices-let-others-learn-from-your-fails-mistakes/

Maybe it will take you @Mushyinvestor to read it through, but I think still worth it.

I hope you can somehow get out of your contract. ![]()

AXA pension 3a Protect Plan

I don’t know how should I do that as that guy just blamed the broker and said this protect plan is better for you as it has gurranteed 0.5% interest. But it’s not a life insurance.

I wrote to that broker but honestly he was screaming at me by saying that he showed me the contract and it’s my fault. Also he himself have the Swiss life 3a plan. In his opinion AXA didn’t perform well but atleast I got 0.5% interest.

This is a life insurance according to their own document → https://www.google.com/url?sa=t&source=web&rct=j&url=https://www.altersrente.ch/pdf/AXA_protect-plan2017_de.pdf&ved=2ahUKEwi67PflnqD4AhVNq6QKHQhCDlEQFnoECDcQAQ&usg=AOvVaw1KIiLWR2jNghqPLrFweECZ

On page two it states “Klassische Lebensversicherung”.

They can’t deny to cancel your contract, however you’ll probably lose a lot of money you put in already. However as stated by others and also in other threads in this forum, bite the bullet and move on to something like VIAC or FinPension. In the long-term you will profit and if you really need life insurance, it’s better to have a separate contract that only covers life insurance, not something linked to 3a pension.

Another thought. Imagine you take a mortgage and want to go for indirect amortization. But you can’t, because all your 3a contribution goes into this product.

As it was said by many others: cancel as soon as possible. If you cancel within 2 years, it also could be that the broker who have sold you this might lose his premium.