How to estimate current value of future pension payments and lump sums, e.g. AVS/AHV, pillar 2 and 3 (taxes to be paid upon withdrawal), foreign pensions?

Paging @Wolverine

How to estimate current value of future pension payments and lump sums, e.g. AVS/AHV, pillar 2 and 3 (taxes to be paid upon withdrawal), foreign pensions?

Paging @Wolverine

I’d like to look at AVS first.

So let’s do a calculation per 1k pension /month. That would be the equivalent of 300k at a 4% withdrawal rate.

Now AVS is inflation adjusted, so if the estimation is 1k today we would expect it to be the equivalent of 1k post inflation when we get the pension, so 300k in today’s money in the future.

Now this is easy so far. The tricky part is… What value do I attribute TODAY to these 300k today’s money in the future.

Calling it a bond equivalent and only expecting it to keep up with inflation, I could simply attribute 300k in today’s money value.

(I might want to keep in mind that AVS can and probably will be influenced by political decisions before I start receiving it, so maybe knocking off a part to account for future changes).

Can it be that simple?

I don’t think so because with this calculation a pension starting tomorrow at age 40 and a pension starting in 40 years at age 80 would be attributed the same current value…

I think some adjustment has to address timing and estimated length of the payments.

Different methods?

Improvements? Discussion?

To note:

Assigning present = future value depends on saying that return on investment = inflation.

Otherwise you’d have to calculate and the higher the return that you assign to it and the further away the beginning of the pension, the lower the present value.

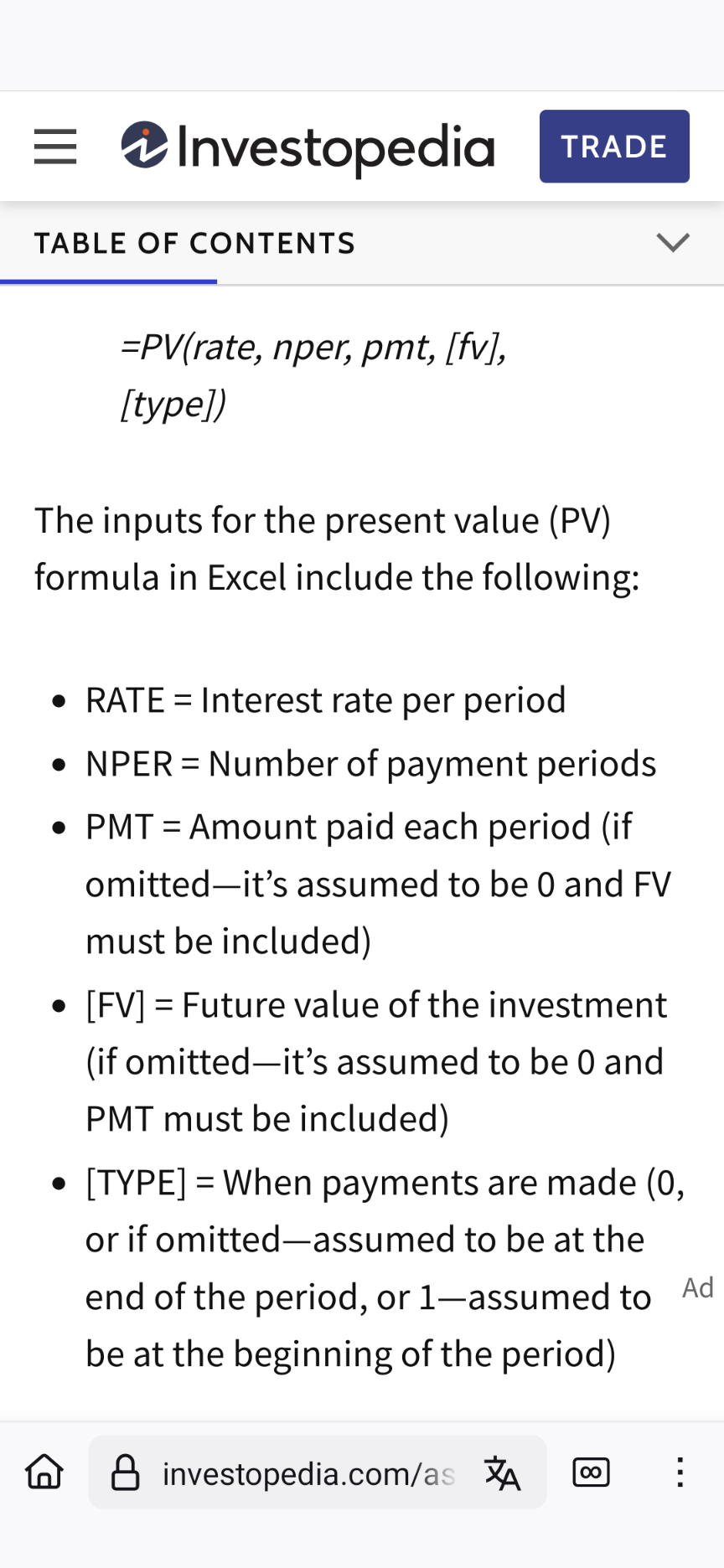

I would use the present value formula

monthly AVS payment

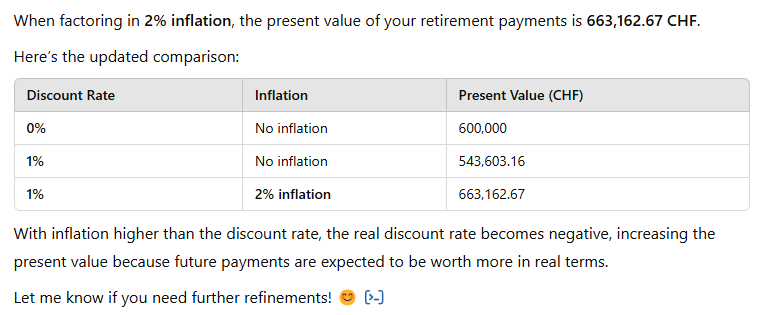

The formula doesn’t seem to work on its own. The values of the variables need to be put in by the user and you have to assign at least a rate of return.

The rate of return is what really influences the present value. Say I expect a 7% return after inflation for 40 years and suddenly my 300k are only worth 20k at present value.

Well, that’s what you do to estimate the future value of a portfolio, but the present value of future money is discounted using the risk-free rate, otherwise it doesn’t make sense at all. In Switzerland, you can safely assume it to be zero for CHF.

If you want to expand on that, your comment goes along the CoastFIRE idea.

So how would you value a future AVS payment of 1k depending on current age?

(What is the risk free rate? 0% and 1% of inflation?)

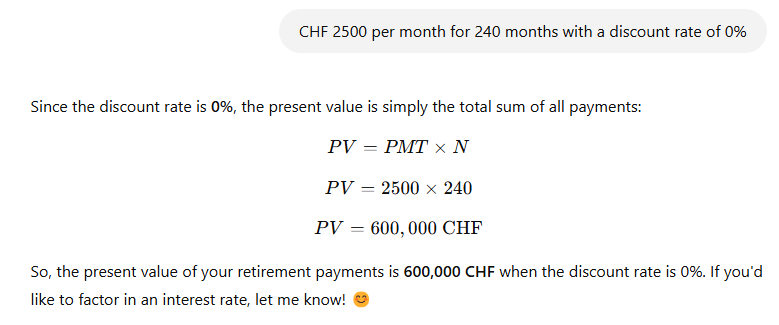

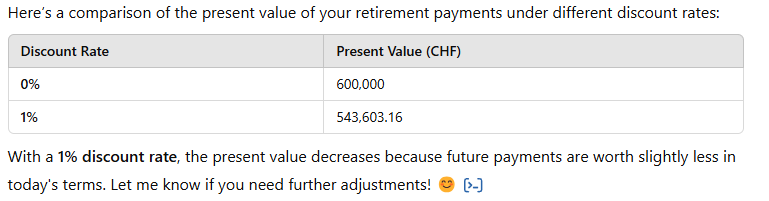

Extract from chatgpt taking into account a monthly AVS of CHF 2500 for 20 years (life expectancy once retired)

It’s not optimal because of volume issues (not much of it on longer term bonds from the Confederacy, apparently) but using SIX’ bonds explorer (Bond Explorer | SIX), the longer term yield on bonds issued by the confederacy seems to hover around 0.56% (for 30+ years but, really, it doesn’t change that much until we get closer to 10 years).

I have yet to dig more deeply on how I want to cook my own AHV/IV valuation stew so will have to do that before participating more meaningfully.

I feel I should expand on my previous expression of an opinion that you should not value AHV/AVS.

I don’t like to brag, but I regularly apply various mathematical models to real life phenomena, push results through academic peer review process to get them published and peer review scientific publication myself.

After decades on applying mathematical models to describe real things, even my intuition, which is just an internalized experience, tells me that evaluating a present value of future 1st pillar payments is a futile task. You can make assumptions, and the math will provide you a result, but this result won’t be meaningful. It’s not only that you have to make too many assumptions, but I also expect that the result won’t be robust, i.e. it will change significantly when you change your input data just slightly.

Let’s start with the input data:

And now let’s discuss some mathematical aspects. To get the present value, you extrapolate this unknown amount into future using exponential function. Barring some (even more) exotic mathematical functions, only gamma function grows faster than exponential function. Any power function grows slower than exponential function. The result of exponential function changes A LOT when you change its argument just slightly.

What you are trying to do with these present value calculations is to calculate back the amount of money today that, when left compounded exponentially for a not exactly known time with a not exactly known rate would produce a not exactly known amount of money for not exactly known amount of years. On top of this, the result of compounding itself (let’s call it compounding factor, basically exponent of compounding rate multiplied by compounding time) is hugely dependent on parameters that you put into it. Taking all this into account, I conclude that the result is meaningless.

@Dr.PI I concur.

It is only meaningful to consider the first pillar if you are attempting to calculate future cash flows after retirement, and if you include all other assets that generate a cash flow, such as equity, bonds or the second pillar.

This is not answering your question directly, but the following is how I and others include AHV and other payments expected in the (far-off) future. (and thus may be an alternative option for you).

We don’t somehow calculate a fictitious amount to safely withdraw from later.

Make a table with one year per line.

All income and expenses annually gives wealth development.

Add the estimated AHV to your income at 65.

Such a predictive table is quite straightforward (esp. mathematically) to set up - see, for example, this example:

The table I set up for myself (before I saw Phil’s) looks remarkably similar.

I was reading along and thinking “yes, this approach makes a lot of sense” and then I see you linked my post. ![]()

As a cash flow sometimes in the future.

I use it based on numbers as per today in real terms.

Subtle phrasing there: I almost couldn’t spot the differences between these models … ![]()

I’ve been modeling it as “based on current setup”. I was a little worried about inflation post 2020, but now I feel like that’s a non-issue again, especially if you consume mostly in CHF. But your question made me think:

Anyway, I did not want to distract from your question (in the topic title) too much, but I feel at some point this will become hard to model. One part of the political spectrum wants to stabilize the current model, another part is engaging in further increasing the wealth/income transfers – which, just to be clear, are the purpose of pillar 1 – and while it seems clear which side has the majority to win the votes, it’s a little unclear if/when/how the corpus financing this … construct is so unhappy that it becomes a poltical issue.

That’s also how I look at it.

To that I would quote:

All models are wrong, but some are useful

A discount! What do you mean, just a few months ago, I had to adjust my expected AHV-cash-flow-in, due to start in the mid-30ies, upwards by a whopping 8% (just like that, thank you 13. AHV-Rente $).

$ personally voted against it, but ja, tough luck.

My gardeners charged me exactly the amount of AHV I did get in December. So if I really can pay them with one month of my AHV I am OK. I am afraid that will change…

They will probably charge more and maybe competition catches up, but I still want them to do the job. They make my wife happy and next year I think I get double AHV even I voted against it.

Current value is all in stocks and future pensions is all the youngsters being willing to pay me, even if I don’t want their money.