I’m trying to talk myself into retiring early. There are a few things holding me back:

A lot of “what if” doubts creeping into my mind (running out of money, stock market crash, etc.)

Reluctance to leave ‘money on the table’ in terms of salary during my prime earning years. and also smaller things like 1000 per month of childcare/family credits that is ‘free money’.

Guilt that I am being unproductive/lazy if I stop working

I think #1, I can rationalize and try to ‘trust the numbers’. #2 I’m struggling with combined with #1/#3 since the voices in my head will say “why not just keep working? it’s a lot of money to give up and you’ll be safer (#1) and what are you going to do anyway with your free time (#3)?”

I did think about it. I would prefer to make a clean cut that then allows me to move my pillar 2 into a VB account with finpension/VIAC and earn more than the 1-2%.

Retire early and you can get your pension into VB account that earns more money

You need to take a break and reset

You don’t need the money for anything. You have a basic lifestyle and any additional money will just be ‘psychological padding’ to help alleviate concerns over risk #1. You currently have enough buffer to sustain a 30% one-time drop in net worth in year 1 of retirement and still have enough to die with zero.

The problem is I don’t know anyone who retired with a modest/comfortable amount of funds. Friends I have who retired early all retired with $20m+ so not really a comparable lifestyle.

You may also have heart attack, stroke or develop terminal illness and become unable to earn and/or regret spending your last years at work, despite that you wouldn’t have had to.

Isn’t enough …enough? Having nominal work may let you keep eligibility for such benefits.

Thanks for starting this thread. I am in a similar situation and have OMY syndrome.

My job will end within 2 years so now my future is crystallizing. I don’t intend to go through the rigmarole of a search for a full time job in the same line of work.

My biggest uncertainty is 3) the change in lifestyle and impact on the family. In writing this I realised my thinking is not as clear as I thought. I need to go through it in more detail with my wife. I hope I can share something helpful, if I survive the discussion !

On your other points

You are planning a 3% Withdrawal Rate? Put the data into portfolio visualizer. You’ll be fine

I know that sooner or later we all have to stop and let go but I don’t underestimate the mind-set change that is going to be required

Squirreling away my savings and growing them has given me a sense of achievement

Dipping below the start point if there is a downturn is going to be tough. No more career progression or savings growth…

As others have already suggested: start out by working part time?

See for yourself how it feels to have (more) time for yourself (and others of your choice*). Experience the now even more existential excitement when the markets tank (or soar) and observe how you react to your nest egg shrinking (or bloating). Watch yourself first hand dealing with fluctuating cash amounts flowing out of your accounts every month and cash flowing in (hopefully) steadily (through part time income, also dividends or coupons, preferrably, or chipping off small parts of your nest egg, if you need to).

If the emotions you’ll go through aren’t your cup of tea switch back to working a bit more?

Took me a couple of years to adjust. First overshooting towards overly frugal mode despite part time money as well as portfolio cash flow still coming in steadily. Now (very) slowly realizing that my money will outlive me easily at the current pace of spending.

As for #2: the term summarizing this condition best is OMY.**

#3:

I’ve evolved towards looking at this as follows: You become the capital allocator of your own resources (time, skills) versus being a tool/resource available for a certain price for the “unproductive/lazy” capital allocators who use your resources for allocating their capital (and making gains off you).

If you’re still in doubt, consider doing volunteer work, work below your market value for a non-profit. If you have someone helping you with cleaning your house, pay them something extra. Pay them a bonus at the end of the year.

Your options are limitless …

* Like me taking time explaining to you, fellow stranger on the Internet, how to deal with a somewhat existential question in a few short paragraphs …

** As I learned from @FatFire IIRC this condition goes by the name of OMY: One More Year.

By suffering from this syndrome you can extend not leaving ‘money on the table’ until you have to pass it on to your heirs (well, you personally won’t have to, someone will take care of it because you’ll be … ahem … absent forever?).

Is this something that you decided or something that was decided for you? In some ways, I would like to be made redundant so that the decision is made for me.

I used to be a member of FatFIRE and shook my head at those people with $20m stock portfolio, $10m real estate portfolio, with annual spend of $200k asking (genuinely) if it was safe to retire.

Now I feel I’m entering that kind of silliness myself (but with a much smaller portfolio!).

I’ve modelled out the numbers and in 4 years, I should be able to retire. I could even survive a one-off 30% hit to the stock portfolio (real estate will tide me over). But I’m still a little nervous as:

There could be mistakes in my model (I found many big mistakes in the last few months)

There are unknown assumptions on returns, inflation, maintenance costs, etc. (now I think about it, I should really get critical illness/disability cover).

The model doesn’t even have a withdrawal rate until age 57 (7 years into retirement) when inflation grows expenses more than income. Before then, income exceeds expenditure. Heck even afterwards, when expenditure exceeds income, the pot is still growing as the capital gains are more than the annual deficit! [I just checked, under model assumptions, at 90, my NW would be approx 2x my NW at 50]

So on an intellectual level, I ‘know’ it should be OK. But as I’m a belt and braces kind of guy, I can’t shake the feeling that I might have neglected something. But I try to talk myself around in that the bigger downside is not running out of money by getting my calculations wrong, but working too long and missing out on having the freedom to do my own things.

I would definitely try that if it weren’t for the fact that:

I want to put my pension into a VB account to have better tax free returns

In reality, I’d have to work just as much compressed into fewer days

In some ways, I do think part time work would make sense to do a gentle transition. The problem is having small kids now, I’ve had no life: it’s just been work and kids for the last 6 years. So I fear it would be a shock to suddenly stop working - esp. as I lost touch with all my friends and networks. But I think I would be OK. I kinda think it would be better to go ‘cold turkey’ and get the shock over with and deal with it.

It is a separation linked to restructuring. I am confident I could avoid it by finding another role in the company if I wanted to but it doesn’t make sense.

My role and hours have decreased to ~50% whilst I stay on 100% pay so it is giving me a soft landing. I am very lucky and happy.

It is the push my wife and I needed. It removes a barrier, by not having to telling her I want to hand in my resignation letter

My wife is quite supportive of me quitting so I don’t have an issue there. I just need to prepare myself for it. I still have 4 more years to go so I have time to get ready.

Your excel model sounds complicated. Now I understand your other post about excel errors!

Here are the models I keep, in case it helps:

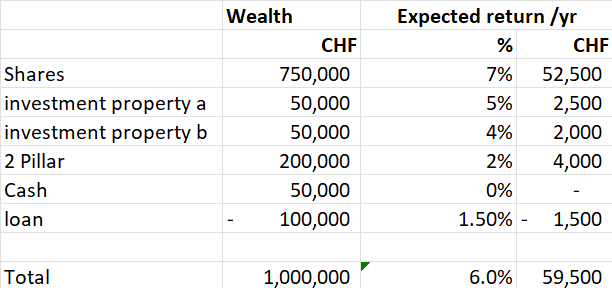

Bottom up expected return calculation

Objective: calculate the return I can realistically expect over the long term using reasonable return assumptions for each asset

I keep the model quite simple and I don’t make any distinction between dividends or capital growth

Withdrawal rate: Spending / net wealth

Objective: sense check that I am not out of line with Trinity study.

Portfolio Visualizer website: Monte-Carlo simulation

Objective: understand the probability of running out of money

I play around with “worst returns first” to test sequence of return risks

Yes. it is a monster. It started out as a single sheet with a row per year and maybe a dozen columns. Now there are >80 columns in the lead sheet and 8 sub-sheets.

It does a full year by year cashflow calculation including:

Year by year portofolio return (nominal)

Year by year expenses including inflation adjustment

AHV calculations

Applies tax rate to income (currently estimated based on broad deductibility categories - I plan to update it to make accurate canton/gemeinde/federal tax calculations)

Calculates wealth taxes

Allows for year by year split of investment income between capital and income (has a surprisingly big impact on tax)

Has 3a and Pillar 2 withdrawal phasing together with capital tax calculation (one mistake found was here as I forgot to include gemeinde factor and federal taxes in an earlier version!)

Maximum pension capacity and pension contribution phasing calculation to optimize taxes

Real estate uplift calculation for asset based AHV costs

Property schedules for mortgage payoff and rental income (detailed Eigenmietwert etc. calculations to be included in the tax calculation overhaul - currently estimated)

Pension income, child credits, RSU vesting schedule, tax approximation for federal and canton (under both child and no-children scenarios for when kids are older)

I know it is overkill, but it is meant to help calculate various payment plans (e.g. pension contributions, pension withdrawal schedule etc.) as well as providing some ‘psychological comfort’ that I’ve done my homework.

I use cfiresim to sense check. As well as sense checking against very simple retirement calculators.

Biggest unknowns are stock market returns and sequence of returns as well as inflation.

When forecasting “what my future is probably going to look like” and checking my asset allocation then yes I assume 7%.

On the other hand I believe I am quite safe in planning for the worst by by budgeting for a 3% withdrawal rate.

The reason I am quite confident in 7% long term is because I have a big conviction in Fundsmith which has returned 12.4% p.a. in CHF since inception in 2010. My second position is Smithson which should generate higher returns since it invests in smaller companies.

I try to plan in a balanced way. If your assumptions are too pessimistic you might make sub-optimal decisions. For example if I believed equities were only going to return 4% then I might invest in bonds instead, etc

I built something similar, mapping it all out from 2019 to 2054 … … copied the structure mostly from a corresponding calculation template by a professional wealth advisor that I consulted before considering leaving my former well paid job.

The sheet helped me towards having some confidence that I probably won’t run out of funds before I don’t need them anymore.

I still update that sheet once a year with actual figures based on my tax declaration.

BTW, in the first year or two I also uncovered several somewhat serious calculation errors in my sheet implementation. In the end, they didn’t matter.

Now that I’ve moved to part time work and after shifting my portfolio more or less from a total return strategy towards aiming for steady and growing income generation, I started a new much simpler spreadsheet that focuses on projected cash flow* per year that I can spend.

The past three or four years of observing the portfolio indeed realiably generating a growing cash flow have now given me (more) ease of mind and confidence that things will indeed pan out.**

Statistically, the total return approach has a higher chance of generating a higher return over a sufficient period of time. Since I don’t (want to) have a sufficient period of time, the steady and better predictable growing cash flow approach is preferrable to me as it let’s me SWAN.***

The growing income generation approach IMO also addresses better what you consider your biggest unknowns:

stock market returns: it’s nice to see my portfolio valuation going up, but even if it goes sideways or down, my cash flow goes up

inflation: this is me handwaving a bit, but being invested in companies (equity) addresses inflation to a certain extent (see e.g. the recent pricing power muscle flexing by consumer staples over the past year or two)

As always, YMMV.

The best approach is the one that allows you to stay the course, regardless of the weather.

* I.e. after taxes and other (mostly) fixed costs (like rent).

** My former job in information security has given me enough déformation professionelle that I am always paranoid about where things could still go wrong. This angst becomes smaller with every month of experience of that cash steadily flowing in.

I can relate to that and I see how difficult it might be to tackle this.

I don’t think I would have been able (psychologically) to take that step with small kids (although it actually makes most sense to spend more time with small kids!).

And equally, if I had moved to part time at my former company, I’d also have done the ~same amount of work … just for less pay.

I benefitted from my kiddo being much older and me moving to a different company for the part time work.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.