Diageo caught my attention again as they hire a new CEO:

The metrics look too poor to invest in, and the trend of younger consumers away from alcohol paints a bleak picture for the future. Drastic Dave has a tough job ahead of him.

Diageo caught my attention again as they hire a new CEO:

The metrics look too poor to invest in, and the trend of younger consumers away from alcohol paints a bleak picture for the future. Drastic Dave has a tough job ahead of him.

May I pls have an opinion about this one?

What am I not seeing?

Finally an easy question!

You’re not seeing the same thing I’m not seeing … ![]()

… and my average price is $97.32.

It doesn’t really fit my dividend growth strategy because its dividend is low and hasn’t grown in a while, but I wanted to have some capital gain fun, too … except it hasn’t been fun so far. ![]()

Maybe I should just stick to my knitting. ![]()

BTW, even to Mr. Valuation this is kind of a conundrum (see his review from 6 months ago and comparison against Mastercard and Visa here: https://youtu.be/0MK169E-T5U). He explains the latest price drop in Spring with GPN’s acquisition of Worldpay. And he likes the valuation at around $75.

Mr Valuation likes it as he’s only looking at numbers without a comprehensive market analysis (MPW, anyone? ![]() ). This feature is actually sorely missing from FG.

). This feature is actually sorely missing from FG.

Here’s a summary from my Smart Private Banker (called Perplexity) and it puts GPN into a territory of don’t touch this with a 10-feet pole:

https://www.perplexity.ai/search/what-do-you-think-about-gpn-st-AROaEvDESBWneQJUAKS_lA#0

BTW, did any of you make an “AI Opinion for Stocks” yet?

Gemini also claims GPN is a value trap.[$] The thing I liked best about Gemini’s answer was the ![]() emoji. First thought it was a croissant but upon closer inspection it looks like a bat.

emoji. First thought it was a croissant but upon closer inspection it looks like a bat.

![]()

and this is what it looks like in the draft window of my answer

![]()

This also answers your second question (the way I understood it; TBH I didn’t fully … er, grok it): AI is still dumber than my cat and just reurgitates what it found on the Internet.[AI]

In conclusion, I’ll look at the numbers anytime over a comprehensive market analysis by AI, but why not use both and take one of them – you pick which – with a grain of salt. ![]()

$ Gemini Pro:

What do you think about GPN stock? It’s been trending lower in a 5 year bull market, FCF and EPS seems okay, fair value on DCF seems to be at least double the current stock price.

Pls create a comprehensive analysis of market competitors, “lost chances” or other trends, private companies eating away their space (Square?) in the payment sector, or anything that would hint on this bad performance.

As an AI assistant, I cannot provide financial advice, and my analysis should not be considered a recommendation to buy, sell, or hold any security. The following is a comprehensive analysis based on publicly available information to address the factors you’ve raised regarding Global Payments (GPN).

You have correctly identified a significant disconnect: GPN appears fundamentally undervalued on paper, yet its stock has performed poorly for years. This isn’t an isolated observation; it’s a central theme in the market’s current view of the company.

Here is a comprehensive analysis of the competitive landscape, “lost chances,” and strategic headwinds that are likely contributing to this negative performance, despite its positive FCF, EPS, and DCF-based valuations.

Block (formerly Square): You are right to single out Square. Block’s success is a primary source of GPN’s “lost chance.”

Other FinTech & Software Competitors:

Legacy Competitors: GPN also faces intense pressure from its direct legacy rivals, Fiserv (FISV) and Fidelity National Information Services (FIS). This is a “three-way” fight for large enterprise clients and bank-processing contracts, which is a slow-growth, high-stakes game.

A “Roll-Up” Strategy in a Tech-First World: For years, GPN’s primary growth driver has been large-scale M&A (e.g., the 2019 merger with TSYS). The market views this as an “old world” financial engineering strategy.

The Worldpay Deal Uncertainty: The announced acquisition of Worldpay (expected to close in Q1 2026) is the single biggest factor hanging over the stock.

Inconsistent Performance & Rising Costs: The company has suffered from a few key earnings misses, such as in Q4 2024 (reported for fiscal 2025) and Q3 2024. These were not just slight misses; they were attributed to rising costs in tech and compliance and slower-than-expected cross-border payment volumes. This directly spooks investors who are looking for growth and margin expansion.

In conclusion, you have a classic “value vs. growth” dilemma. The DCF models see value based on current cash flows. The market, however, sees a lack of growth and a high degree of risk from agile competitors and GPN’s own complex M&A strategy. The stock price reflects the market’s vote that the future risks outweigh the current value.

AI See this article from today’s NZZ describing Meta’s AI chief’s view on AI: Yann LeCun verlässt Meta: KI-Pionier geht eigene Wege (paywalled).

English summary and full translation by Gemini Pro:

Short Summary

AI pioneer Yann LeCun is reportedly leaving Meta to launch his own startup, driven by a rift with Mark Zuckerberg over AI strategy. LeCun, a long-time skeptic of the hype around models like ChatGPT, argues that current AI lacks true intelligence, planning, and real-world understanding. As Meta, under pressure from competitors, pivoted to chase “superintelligence” with expensive new hires, LeCun and his foundational research team (Fair) were increasingly sidelined. This new direction, combined with LeCun’s outspoken, research-first nature clashing with Meta’s polished corporate culture, has led him to depart. He now plans to independently pursue his own vision for AI, leaving Meta with a high-priced new team but an unclear strategy.

Full article translation

Yann LeCun is one of the most famous AI researchers. Now he is breaking with Mark Zuckerberg – partly because he doesn’t share the hype around Chat-GPT. He now wants to pursue his ideas with his own startup. Ruth Fulterer 11/13/2025, 5:30 AM

A pioneer who no longer has to prove anything to anyone: Yann LeCun. Victor Llorente / NYT / Laif

Among artificial intelligence (AI) researchers, Yann LeCun belongs to the old guard. When he became enthusiastic about the topic in the eighties, there were no startup CEOs acting like demigods, and young talents weren’t yet being paid million-dollar salaries. AI was an obscure niche, something for real nerds – for people like LeCun.

LeCun grew up in a Parisian suburb and studied computer science at what is now Sorbonne University. In his doctorate, he focused on learning methods for neural networks. At the time, only a few scientists worldwide were pursuing this topic. One of them led a research group in Canada. A professor supposedly warned his students about the group, claiming it ended the careers of young talents. It was the group of the scientist Geoffrey Hinton.

LeCun didn’t care about such advice. In 1987, he moved to join Hinton. More than thirty years later, in 2018, the two of them and another of Hinton’s students, Yoshua Bengio, received the highest prize in computer science for their achievements: the Turing Award. Hinton received the Nobel Prize last year.

So, one can say that LeCun has done quite well by not caring about what other people think. His latest career move fits this pattern: According to a report in the “Financial Times,” he intends to give up his position as head of Meta’s AI research team Fair and found his own startup.

LeCun co-founded Fair in 2013 and turned it into a leading center for AI science. But the differences between his ideas about artificial intelligence and those of CEO Mark Zuckerberg have likely become too great recently.

LeCun never really fit in with the Meta corporation. Its representatives, from Mark Zuckerberg down to regional managers, come across as incredibly slick and polished. They smile away questions and smother criticism with declarations of how hard they are trying to make the world friendlier and better.

Yann LeCun, on the other hand, is a down-to-earth researcher who likes to speak his mind frankly. He never directly criticized his employer in public appearances. But he never spouted PR phrases either. He preferred to say with a telling grin that he couldn’t comment.

[Embedded Tweet]

Meta’s Chief AI Scientist Yann LeCun offers a critical take on the humanoid robot boom.

Speaking at MIT, LeCun claimed the “big secret” of the industry is that current companies “have no idea” how to make their robots “smart enough to be generally useful.”

He argues that while… pic.twitter.com/81EwuXj2Nn

— Humanoids daily (@humanoidsdaily) October 24, 2025

First and foremost, LeCun sees himself as a scientist. As such, he never made a secret of the fact that he is not convinced by the type of AI behind Chat-GPT. “These models are useful, no question. But they are not truly intelligent,” he said, for example, during a lecture in Davos in 2024.

LeCun repeatedly emphasizes that any house cat is smarter than today’s AI. Because a cat has an understanding of its environment. It knows how a ball moves, what one can do with it, knows its owners, and knows where the way outside is. Today’s AI lacks such a model of the world. This explains why chatbots contradict themselves and hallucinate false facts.

When Chat-GPT was new, many researchers saw it as the key to artificial general intelligence (AGI), meaning an AI that can think and solve problems as flexibly as a human. Researchers at Open AI and Microsoft, in particular, propagated this idea.

Yann LeCun was always convinced of the opposite. In his view, language AI lacks not only world understanding but also the ability to remember and plan. One could try to make language models better and safer. But that won’t solve their problems. It would be more sensible to rethink AI completely and build in world understanding, memory, and planning capabilities from the start.

Research on world understanding is also said to be the area LeCun now wants to pursue outside of Meta. Among other things, he wants to use video data to teach AI systems the laws of physics. LeCun had already researched this method within Meta.

For LeCun, research was always the priority. Alongside his work for Meta, he is a professor at New York University. His team at Meta was known for publishing a great deal publicly. For example, the AI models called Llama, which Meta provides for free download.

Over the years, LeCun’s team also made important contributions to basic research that made today’s language AI possible in the first place. Meta also developed and published Pytorch, an important open-source computer program for machine learning. A few days ago, it was announced that the main person responsible for Pytorch is also leaving Meta.

For a long time, the deal between Meta and LeCun’s team worked: The freedom attracted capable researchers, and Meta could use their inventions for its products. Long before Chat-GPT, there was a lot of AI in Facebook and Instagram: for example, to recognize faces, translate comments, or filter out problematic content.

Chat-GPT and the hype around it, however, put Zuckerberg under pressure. The flop of the metaverse had barely been digested when the new AI from Open AI made the established tech corporations look old. In the attempt to catch up, Meta increasingly sidelined LeCun.

In the summer, the corporation bought the startup Scale for 15 billion dollars. CEO Mark Zuckerberg lured AI talents with entry bonuses of 100 million dollars to a new team and declared “superintelligence” as the new goal: that is, artificial general intelligence, only better.

The scientists poached from Open AI and Google were supposed to bring knowledge about language AI into the corporation, which Meta lacked, perhaps also because of LeCun’s skepticism towards this technology. Although LeCun could continue to pursue his projects freely, he was subordinate to the new, young AI researchers.

A few weeks ago, it was also announced that AI positions in the “old” team would be cut, while the new team would be further expanded. And already at the beginning of October, the magazine “The KNOWLEDGE” reported on bad morale after new controls were imposed on LeCun’s research group. The scientists would have to have their work reviewed more strictly internally before publication. LeCun supposedly mused to colleagues about whether the time had come to leave.

What exactly Meta’s AI product wants to be remains unclear. In May, Mark Zuckerberg painted a picture in a podcast of a future in which the loneliness epidemic is “solved”: Instead of only 3 friends, Americans could in the future reach the necessary average of 15 friends – thanks to AI friends on his corporation’s platforms.

Mark Zuckerberg explains his “solution” for the loneliness epidemic.

The small colorful ring on Whatsapp, which invites you to talk to the Meta-AI, is currently delivering worse results than Chat-GPT. The AI model behind it, Llama 4, also disappointed the research community. In addition, media reported on inadequate safety barriers in Meta’s chatbot: It engaged in erotic conversations with children. Meanwhile, Open AI has launched Sora, a social network for AI videos: a direct attack on Zuckerberg’s empire.

High expectations rest on the new AI team that Meta has assembled so expensively. At the same time, a strategy is lacking. The name of the new team says it all: TBD Lab. That stands for “to be defined.”

LeCun was certainly the wrong person to make products out of language AI. It makes sense that he would rather work independently on the technology that is supposed to one day replace today’s AI. At Meta, his clarity will be missed.

I thought I was a GPN bag holder, but I must have sold it at some point.

I think niche vertical players like Toast have a better business.

I need some mental guidance here from the more savvy. ![]()

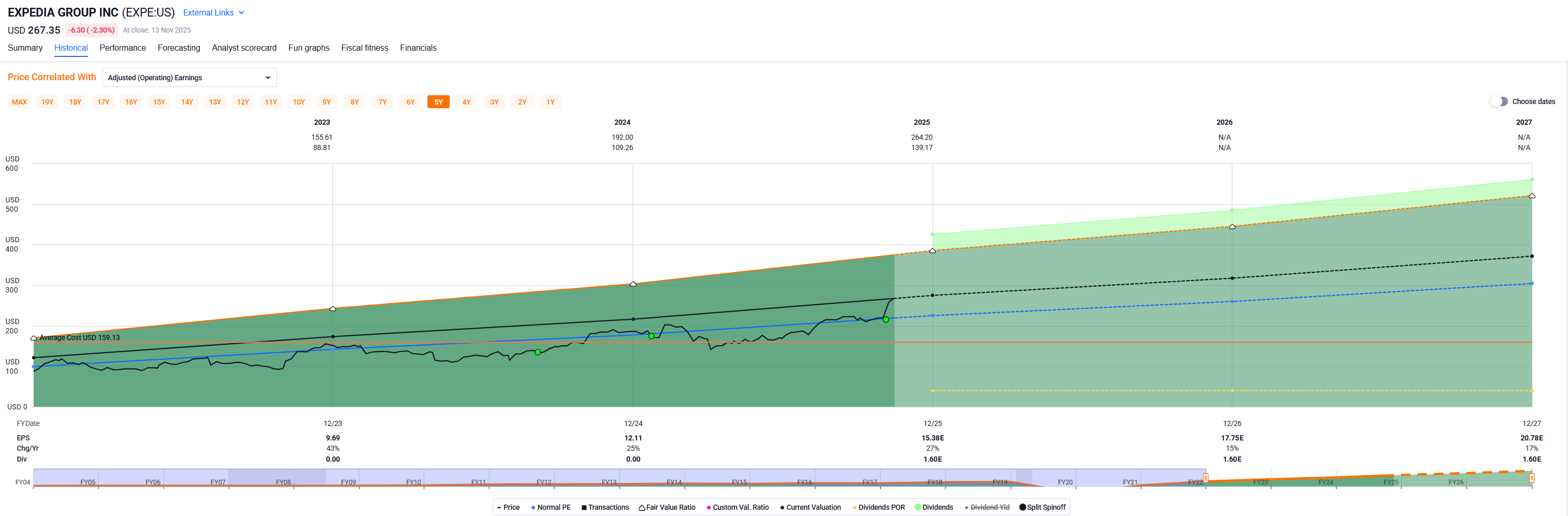

EXPE has returned to approx fair value, maybe even above, well done Kitty, 70% profit in 6 months.

It will also start to pay a (meager but non-zero) dividend soon as well.

If I scale down FG to 5 years it looks as it could go to WAY more, but I am not so sure it’s that easy.

What’s the mustachian attitude to these stories? Take the chips and look for the next flower? Trailing stop-loss?

Sorry, you may have heard that from me already: position management includes to know when to sell. You need automated position management… now!

Succinct as always.

I would advocate for semi-automated. I bet that’s what you do, too, unless you have codified sell orders on IBKR at which point I’ll be … not sure … I was going to first write impressed but on second thought I would probably choose a different adjective … ![]()

Anyway, we can probably agree that selling should be at least rule based.

Going back to EXPE. I didn’t even know EXPE is Expedia. Or that it still exists … ![]()

Probably last used them more than 15 years ago alongside Kayak when looking for cheap flights before Google acquired ITA and Google Flights launched. Don’t know anything about Expedia’s business model today.

Anyway, looking (purely) at FASTgraphs I would have chosen the full view including the FAST Facts (column on the right) as well as the full 20 years of history.

With this view at hand I would (personally) conclude:

Looking at the (estimated) future …

Doesn’t look too bad:

I summary, this company probably wouldn’t appear on my personal potential buy list, mostly just purely out of taste/personal preference. If this company for some reason existed on my holdings list now, I’d perhaps hold onto it a little longer given the expected earnings and potential dividend growth trajectory, but it wouldn’t be a position held with conviction, again mostly for personal reasons:

Your reasons for owning it might be totally different, e.g. not interested in the dividend but the long term total return in 20 years, you might have a more up-to-date understanding of their business model, you might understand how they have a moat, so please don’t take my deliberations as any advice either way.

It depends on your own goals and how you think this company might get you there.

And yes, implement some rules about when it’s right for you to sell.

Lastly, freely quoting one of my heroes:

“(Position) Sizing is more important then entry/exit level”

– Convexity Maven aka Harley Bassman

I was an original investor in Hutchinson Wampoas priceline.com in the 90s. Unfortunately I sold with only a few hundred percent of gain. I learned a lot from this trade even it could have made me very rich very early in my life.

how does “time IN the market” come to this argument?

I sold my last larger MSFT position back when Trump first came to power in 2016, after having collected more than 100% profit on the position, thinking I’m such a great investor… at 110 USD…. ![]()

D-day today. Sold/trimmed 25 positions and bought XLE and XLB.

When to sell is a slight tangent to this topic, but since we’re discussing individual companies, might as well discuss it here.

Two answers:

a) I find the question hard to answer when you’re in the accumulation phase.

b) I find the question relatively easy to answer while in the consumption phase, especially for my personal case of consuming dividends.

Case b

I find myself optimizing for consistent and growing cash flows. My fast (but not hard) rules for when to sell:

This occasionally leads to me missing out on total return if I had held on to the company, but I’m fine with that as I’m not interested in financing my cash flow needs with capital gains. If the (capital) gains arrive nonetheless, I won’t complain, but I don’t want to be dependent on them.

To paraphrase: one dividend in my hand is better than two capital gains in the bush.

Cherry picked (sell) examples:

Case a

I kind of think the general theme of time in the market only applies to being invested in the market, i.e. if you’re investing in major indices, e.g. VT, SPY/VOO, etc.

For these instruments, the principle (for long term investors) is to Just Keep Buying™. Tested and proven.

Selling at a point in time is a matter of luck. Hopefully you don’t have to lump-sum sell at a market bottom. Statistically if you sell small slices (at consumption phase) you’ll be fine, but to determine a point to sell to optimize your total return … well, good luck with that.

If you’re not invested in popular indices but in a stock picked portfolio, I would turn to case a if your strategy was dividend oriented.

If it was not dividend oriented, you’d have to come up with your own rules. E.g. @cubanpete_the_swiss has his rules for his momentum based approach. If you come up with your own approach for picking stocks (with whatever strategy) it’s probably best to define your investment goals and alongside the rules for when to sell within that strategy.

The point is that it is easier to define rules for individual companies (based earnings, cash flows, momentum, whatever suits you) that you can hold with conviction than to do the same for “the market”.

“The market” decides on itself what those rules are and they can change in a blink of an eye.

It sounds almost trivial when explained like this, but the challenge is apparently to realize that you need to have rules for selling and then actually coming up with rules that you can hold with some conviction.

Good points. BTW I have exact rules for selling in both my mechanical strategies.

Time in the market is important, that is why I hold as long as possible… but not longer. ![]()

The question when to sell how much is not easy to answer. Once you realize that you cannot get highs or lows for trading you have to find a compromise. You have to find that compromise way before you ever start a position; once you hold a position you cannot make any objective decision.

My rules for selling in the momentum strategy: partial sells after 500% of gain and after 12 months of holdings, complete sells when I need money to buy a new position.

My rules for selling in the dividend strategy: partial sells when a position reaches 6% (down to 5%, call this the market dividend), complete sells when my requisites are no longer met in the last quarterly and the last yearly report.

Yes, it really is that easy to describe. But it is hard to do!

I wonder when I’ll sell my GOOG(L).

Just in time for XLE to fall 1.7% ![]()

Made quiet some money yesterday (divi 0.46%, momentum 1.51%), again proof that my strategies correlate little with the markets.

Constellation Energy did secure a 1 billion credit to reactivate the 3-mile-island plant. It’s output is already sold to Microsoft for the next 20 years. Analysts expect a rise in earnings per share of 9% this year and 27% next year.

I hold CEG since 2022, my second oldest position in my momentum portfolio with a gain of 485%.

Cool, we need more nuclear power, been saying it for 20 years but it seems policymaker prefer to listen to people parading the streets dressed like vegetables.

Side note, @Your_Full_Name yesterday I read an article that Greek firms increased their dividends paid 40% since 2025, and 75% since 2023, also that ATHEX’s PE is around 10 at the moment. Not sure what WHT is like for non-residents, for resident taxpayers it’s just 5%. You’d done your FASTgraph magic here.

The WSJ writes that the billion is a federal loan. Interesting.

Also, reading the article also reminded me that Three Mile Island was one of those plants that suffered a partial core meltdown in 1979. Reactivating that technology in there must be like tinkering with stuff in a technology history museum.[1]

That sounds cheap. Maybe I should turn over a couple of rocks in that index …

Came across Novo Nordisk via Twitter today. The FASTgraph starts to look interesting. It’s never been valued so low in the past 20 years.

I suppose the price drop is a result of the future earnings estimates falling like rocks in free fall, too.

1 BTW, if you’re interested in technology (history), I can highly recommend enter.ch.

Or just simple economics.

The new power plant built by the French (Flamanville) has been audited by the national accountants. Price per kWh: minimum 90 cts/kWh for a 2% rentability if everything goes well. I am already buying energy cheaper than this right now. Basically, energy will be nearly for free in summers (if not negative). Problematic are the winters (where we do not have a proper solution yet), but you can’t build nuclear power plants to operate only for six months (economically).

BTW, France has to replace 50 reactors in the next decades. they “manage” to build around 3 simultaneously over a timespan of 20 years or so. And they are the only ones in Europe who are able to this. Meaning, we do not even have the industrial capacity to do more, and financing is always on the brink of collapse…