This to me sounds a lot more limited as to how much it can grow (esp. since I don’t think they’re really gaining that much traction and the field is fairly competitive with e.g. tiktok, yt, it seems like each generation tends to find a different product to spend their time in).

Most other big AI companies are selling shovels, the headroom here is really big. It’s basically a new area of growth for hyperscalers (where the growth potential was already fairly big).

Alphabet and Meta showed with their quarterly results this week that the most important thing to investors is making a return on AI spending. Both increased their already vast capital-spending plans. Both spent most of their time with Wall Street analysts talking about AI and new products.

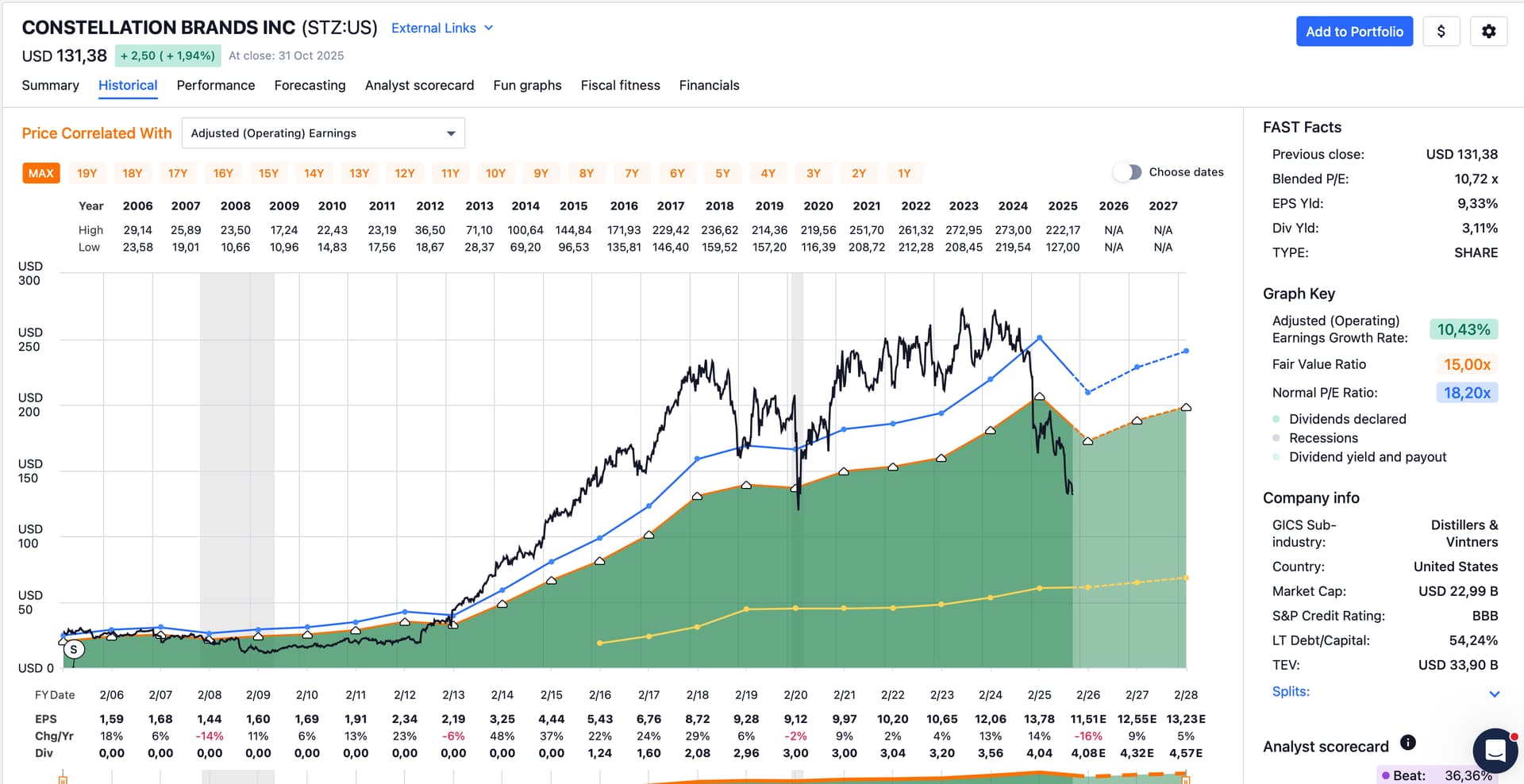

Upon their earnings call a couple of days ago Mr Market had a fit. If they returned to their normal multiple of 13xP/E I’ll be celebrating. In the mean time, I’ll wipe away my tears with the dividends received.

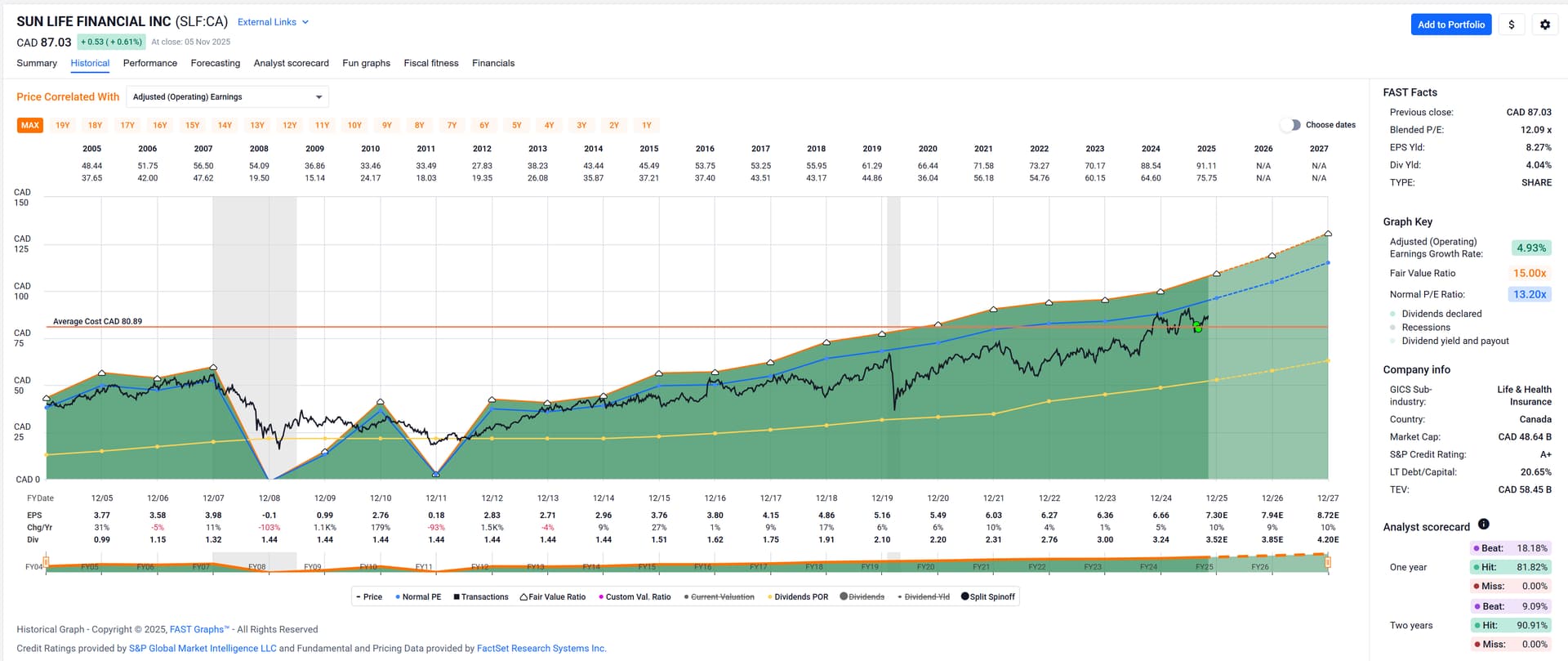

Was considering selling a put on Sun Life, too (it dropped over 5% at market open upon Q3 earnings results), but the options weren’t really liquid (big spreads for the strikes I was interested in).

Interesting. I was considering this too when starting, but the tests showed bad results. Big positions in falling knives. How do you resize?

The market dividend concept works better for me. And market dividends are free of tax. I use a fix position size of 4% initial and sell down to 5% once the position reaches 6%. There are some exceptions for bear markets. Works very nice for me, this year over 10% carry premium and I think Cummins pays the next one. That will catapult me to over 11% cash flow this year and, what is best, a performance over 14%. Tax already deducted of course.

Now FI looks a lot like wirecard to me. Buying up some shops, probably backdoor in eastern countries to reach 46 billion of goodwill looks like somebody did shovel away a lot of cash.

I currently typically mostly have “non full” positions (probably 8 or 9 out of 10).

When positions become full (i.e. “organically” grow above their target (dividend) percentage) I let them run as long as the fundamentals continue to make sense.[$] I don’t think I’ve sold posititions because their dividend yield exceeded my target “max 2%” of dividends in total.

I might sell partial positions because they seem overvalued (recently AVGO, LMT, IRM, SO, etc).

I have sold entire positions because they cut or eliminated their dividend (MMM, WBA, etc).

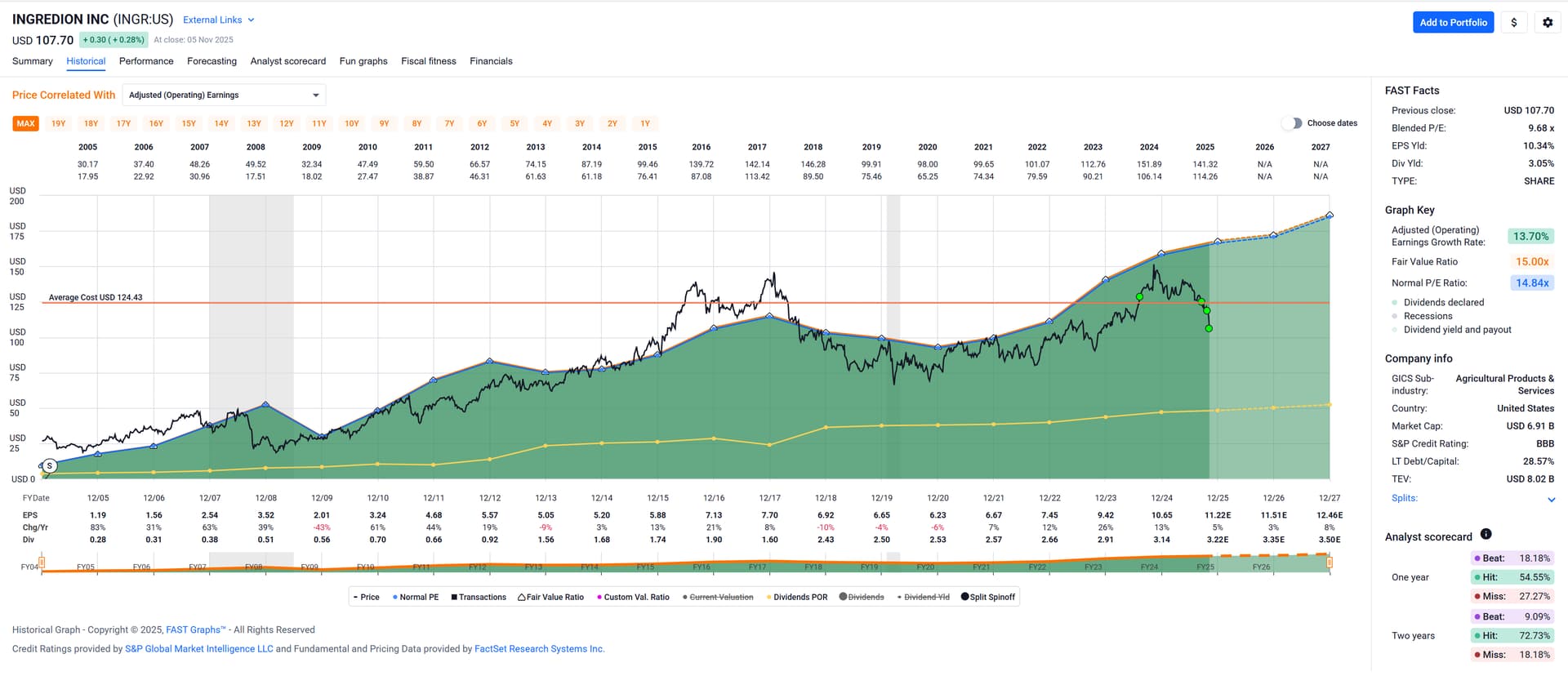

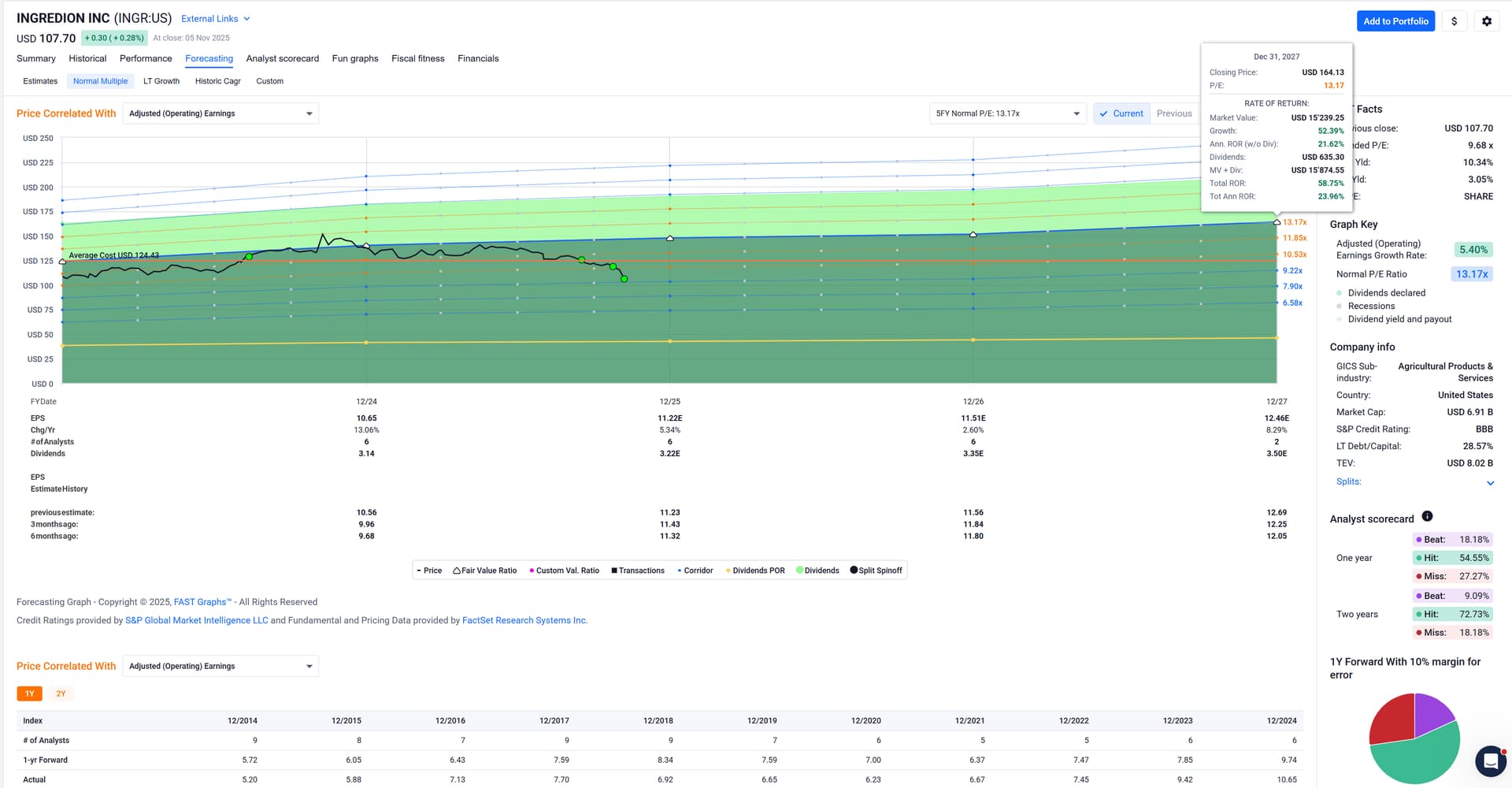

Positions not yet full I continue to fill as I see fit, depending on value, yield, etc. E.g. INGR today.

Edit:

Notably, Cummins has been on my sell candidate list because of its overvaluation, but I have resisted selling so far, even after it jumped about 7 or 8% today …

Same here, but my momentum filter says stop, don’t sell. I take the CMI market dividends but hold the rest of the position as long as it is in the better half of momentum in my dividend strategy. It is at position 3. Same for AVGO which is at position 1. Interesting enough position 2 is occupied by IBM which is still on buy. But I buy only if the position is lower than 4% of total value. Buy low sell high.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.