Came across this article this morning (it’s from about a year ago). Wasn’t quite sure where to post it. Since a couple of sentences resonated with me as a stock picker, I thought I’d post it here:

Measuring the Moat by Michael J. Mauboussin and Dan Callahan (both of Morgan Stanley).

69 pages plus 7 pages for the appendix.

IMO not suitable for a Chat-GPT 10 points summary because of its depth and breath, but of course everyone can run it through their favorite LLM. Maybe turn to their own conclusion (less than a page) on page 65 if you want a summary.

I personally truly enjoyed reading through the full content which is presented in a clear and concise manner, without academic lingo and with a ton of data distilled into succinct sentences and graphs.

Excerpts I liked (not my summary of the paper, really only just what I enjoyed myself):

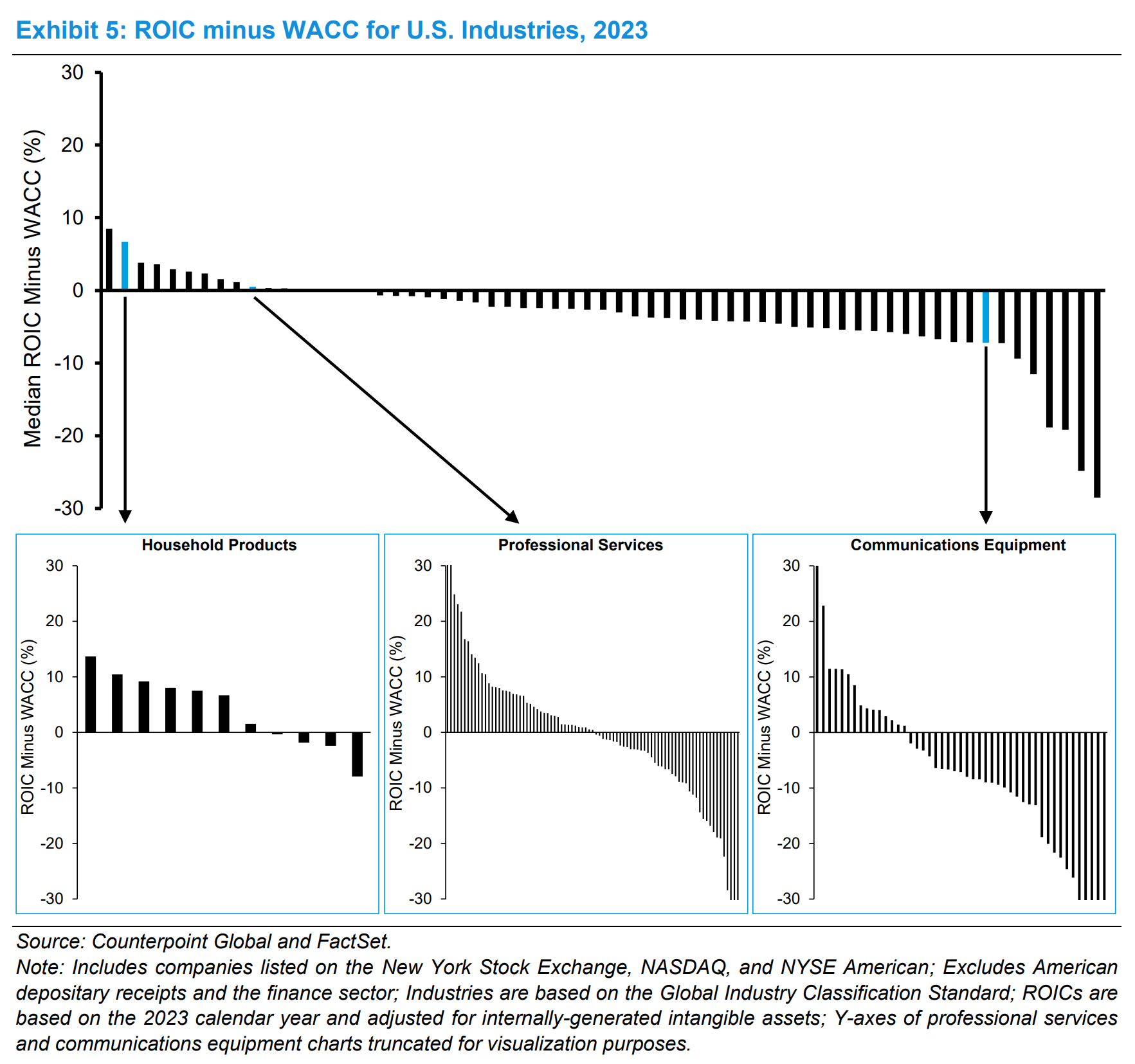

Industries that create value in the aggregate nonetheless have companies that have neutral and negative spreads [Goofy: spreads between positive and negative numbers for ROIC[1] minus WACC[1]]. And industries that destroy value in the aggregate still have companies that create value. This analysis tells us that industry alone does not seal a company’s fate for value creation.

The longer I’ve been playing this game the more I’m convinced that sector or industry diversification (across my stock picked portfolio) does not matter nearly as much as (carefully selected) company diversification.

I’m not ignoring sectors (or industries) completely, but I pay less attention to it and don’t use it as a hard and fast rule for selecting or discriminating companies.

The analysis presented above puts some data behind my hunch.[2]

Peter Lynch, who delivered outstanding portfolio returns while running the Magellan Fund at Fidelity Investments, famously quipped, “When somebody says, ‘Any idiot could run this joint,’ that’s a plus as far as I’m concerned, because sooner or later any idiot probably is going to be running it.”

No comment from Goofy other than stating that this is usually attributed to Buffett but it seems to be Lynch who coined it.

Industry drilldown for the aviation industry:

A majority of the invested capital is in airlines and airports, both of which have negative economic profit. Some businesses, including fuel production and freight forwarders, do have positive economic profit, but their invested capital is relatively small. In the aggregate, the

economic profit for this collection of businesses was negative $69 billion in 2022.

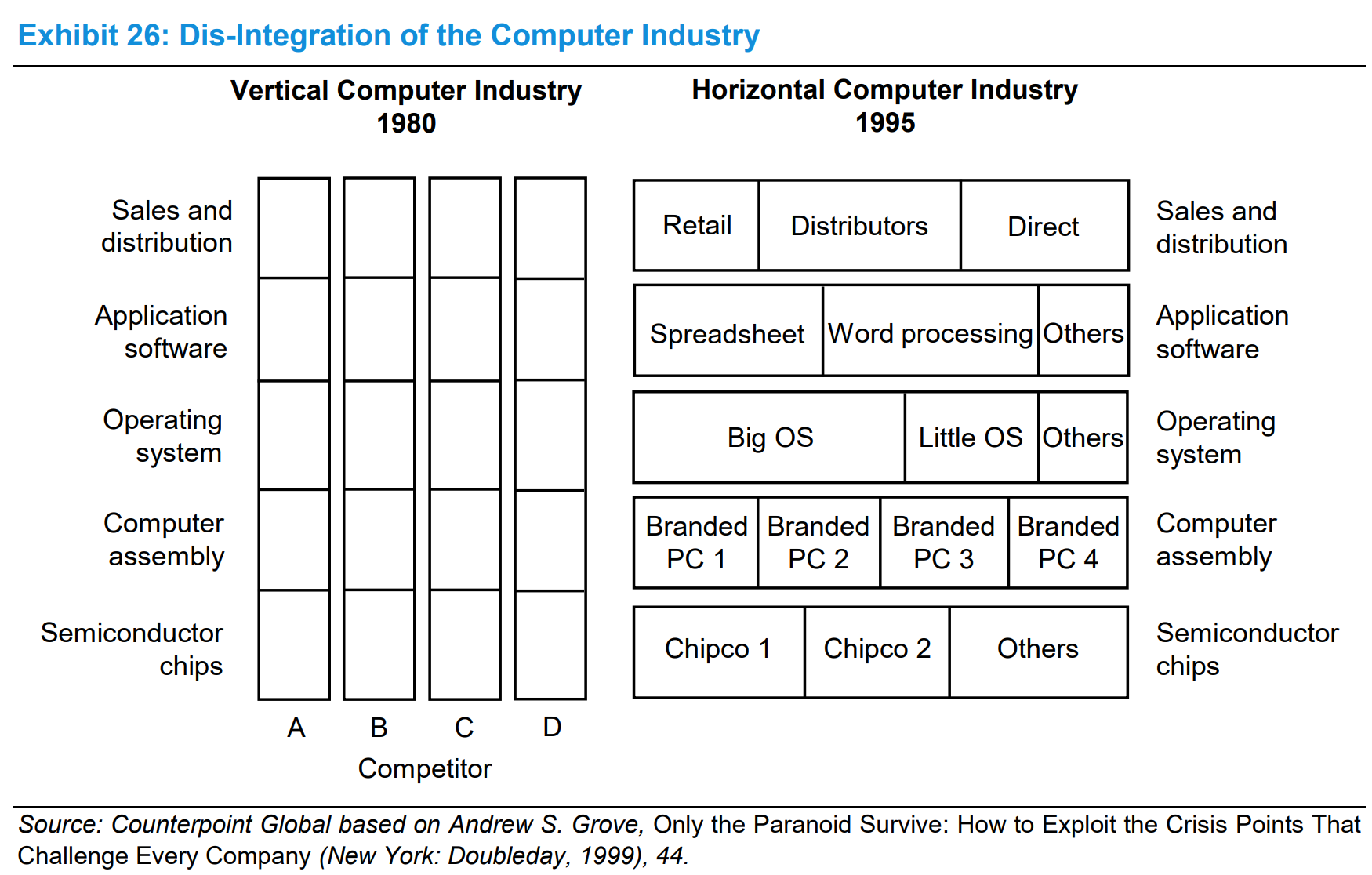

Vertical integration can be a substantial advantage as industries or products start out because coordination costs are high. Companies have to control all aspects of the supply chain so that the product will literally work. Exhibit 26 shows the evolution of the computer industry. In the early 1980s, the largest computer companies were vertically integrated because the engineers at the firms had to make sure their complex products did what they were supposed to do.

As an industry grows and matures, various components within the supply chain become modules, a standardized or independent part of a more complex product. The process of modularization allows an industry to flip from vertical to horizontal. So instead of each company doing each step within the value chain, new companies pop up to specialize in specific activities. This occurred in the computer industry by the mid-1990s. Modularization is a difficult engineering task, but it creates standardization and lower costs when done successfully.

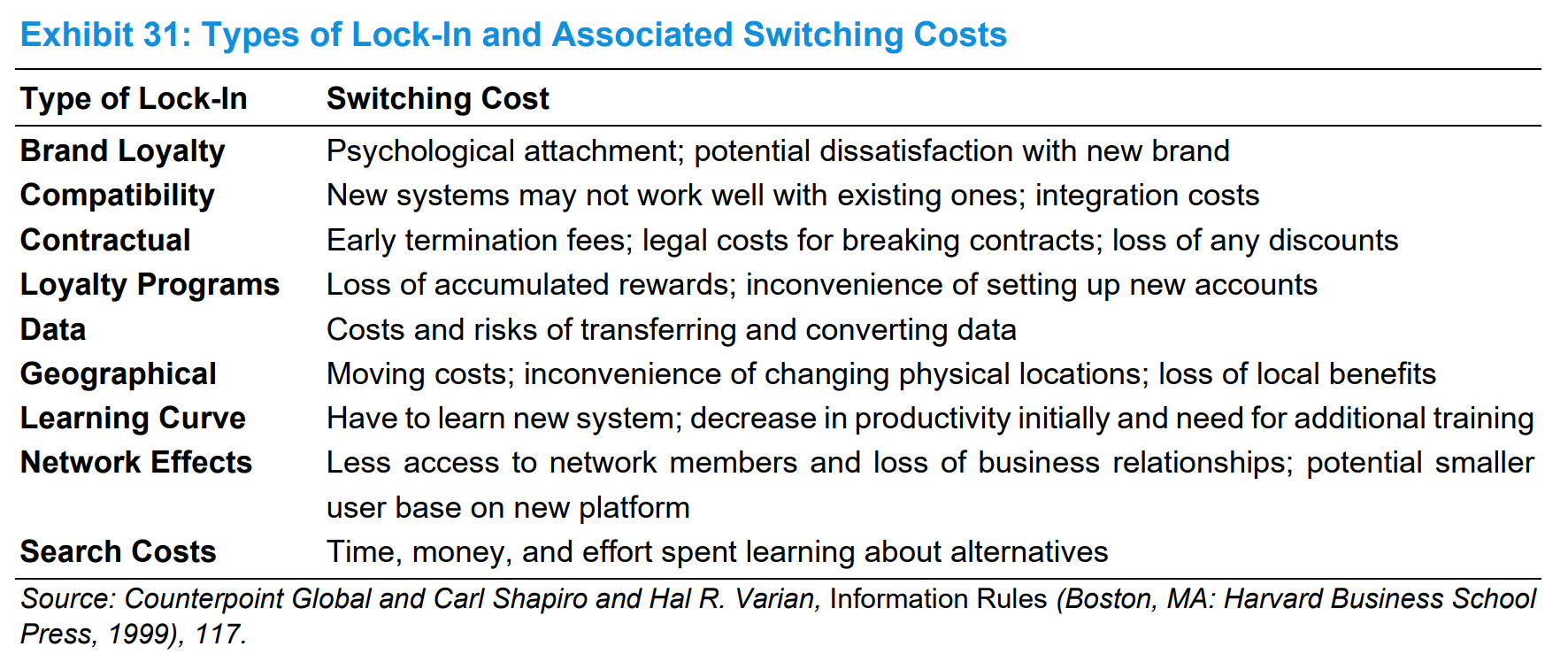

We have discussed switching costs as part of the assessment of supplier power, buyer power, and barriers to entry. Switching costs arise because a good or service creates customer lock-in, or dependence on a supplier.

Exhibit 31 shows various types of lock-in and the switching costs associated with each.

Earlier we defined switching costs as what buyers or users have to endure to move from one supplier to another. But that is incomplete. The total switching cost is the sum of the cost to the customer and to the new supplier.

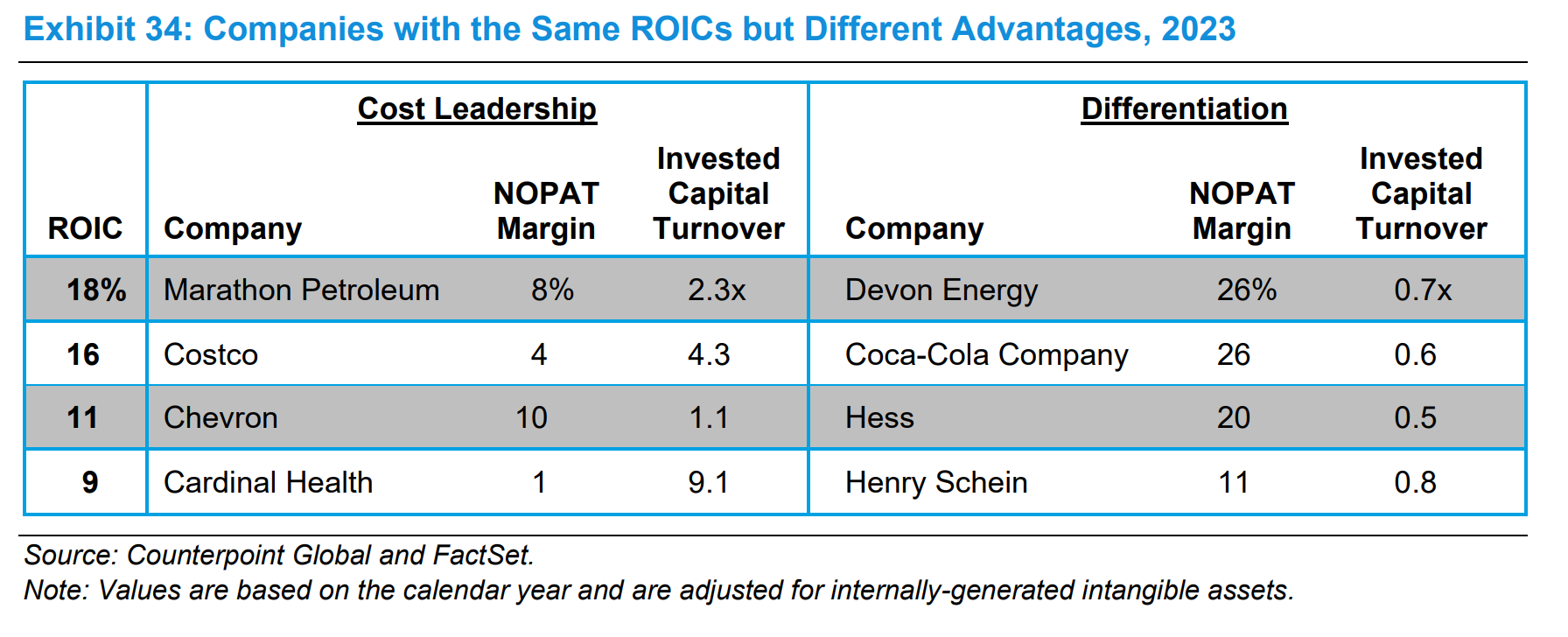

Exhibit 34 shows pairs of companies with equal ROICs in 2023 but different sources of competitive advantage.

The main message is companies can achieve the same level of ROIC using vastly different approaches.

(Goofy: invested capital turnover equals sales/invested capital).

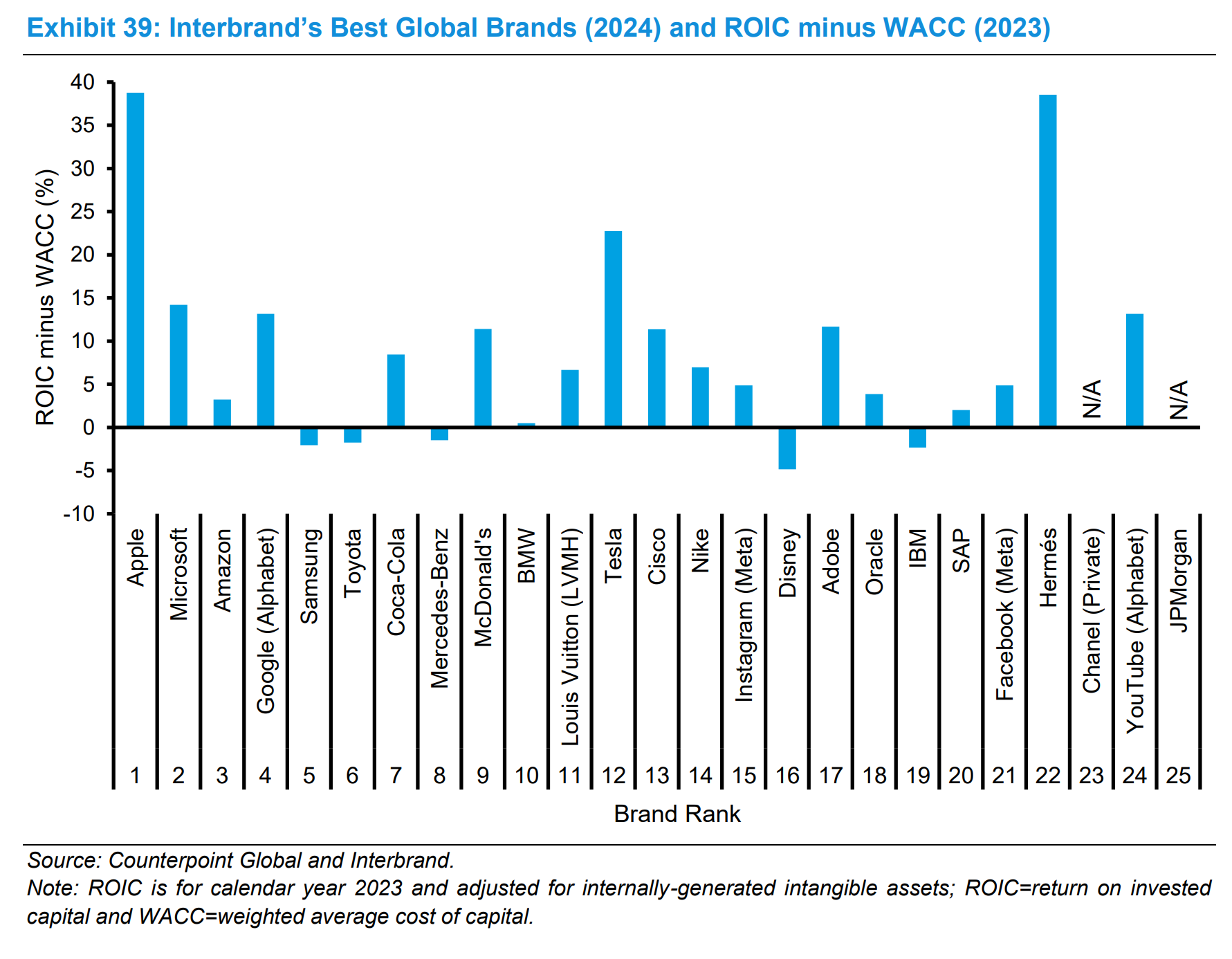

Exhibit 39 shows Interbrand’s best 25 global brands in 2024 and the ROIC, adjusted for intangible investment, for each company in 2023. The correlation between brand ranking and ROIC is weak. The sign of competitive advantage is an attractive ROIC, and the companies that own these brands do not reliably indicate that.

Hope you’ve enjoyed this quick’n’dirty Saturday Night Fever update!

1 ROIC is defined as net operating profit after taxes (NOPAT) divided by invested capital.

WACC: weighted average cost of capital.

2 I’m also fairly convinced that the sector and industry classification (by GICS) is fairly … inaccurate is probably the polite word?

E.g. Google is classified as a Communication Services company. Goofy’s former insider view: this company is mostly Tech …

Amazon is classified as a Consumer Cyclical … I’d label it as a mix between Consumer Staple and Tech.