One of my favourite books, literally changed the way I see the world!

1 Like

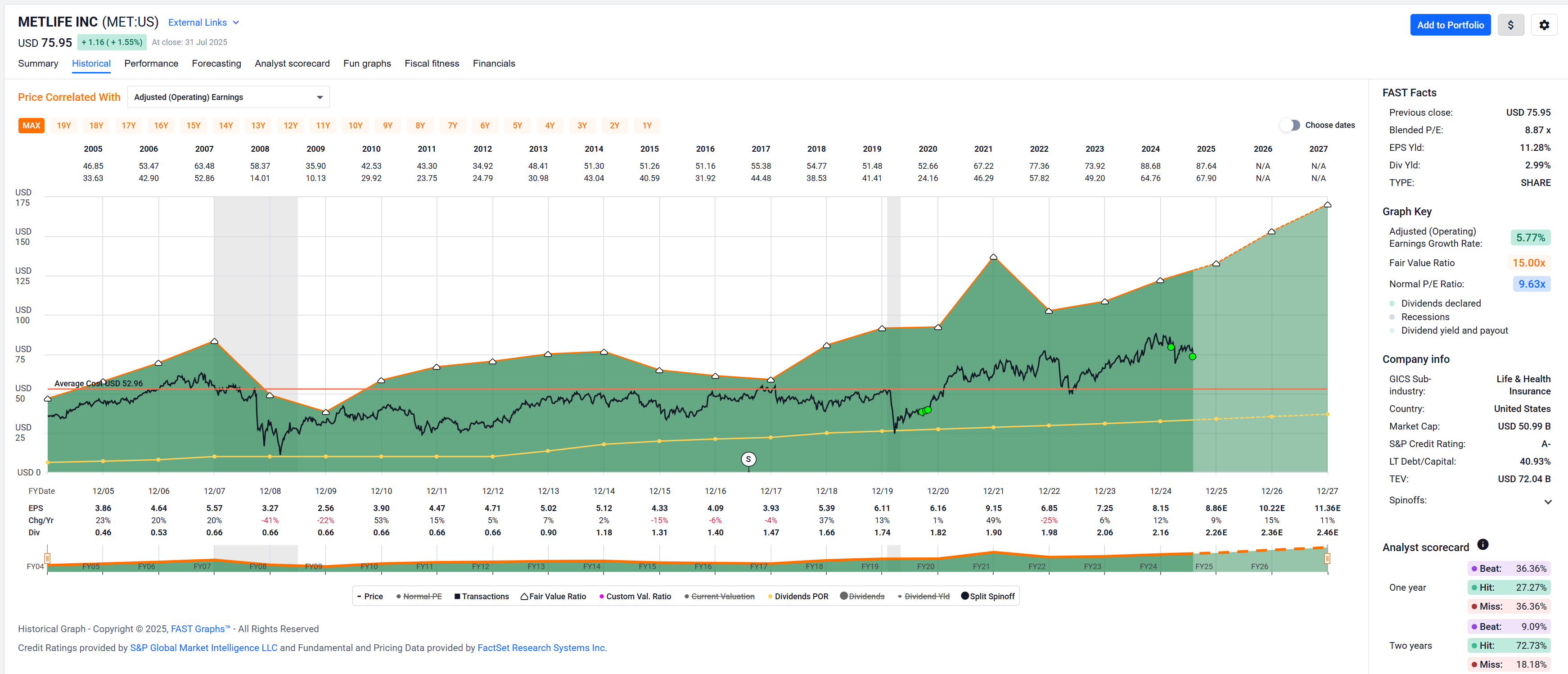

On my (buy/sell) candidates list[BS] MET lit up today (-3.25%) and I bought a few shares into the dip as the company pays an above 3% dividend now while fundamentals mostly continue to look solid.

Free cash flow is a different picture (and is projected to not even cover the dividend in the next few years), but operating cash flow is still fine.

Their S&P credit rating of A- and long term debt / equity at a manageable 40% makes me think they’ll continue to pay their dividend and even raise it further given their history of 12 years of raising it.[D]

Reminds me of Pepsi: couple of capital heavy investments planned in the next couple of years, but IMO not a fundamentally deteriorating business.

BS The BS list – pun intended – is a roughly weekly updated list of companies worth buying given the FASTgraphs fundamentals (or selling, same criterion).

D They didn’t even cut their dividend during the Great Financial Crisis (like most financial institutions) but instead held it steady until 2012 after which they started raising it again.

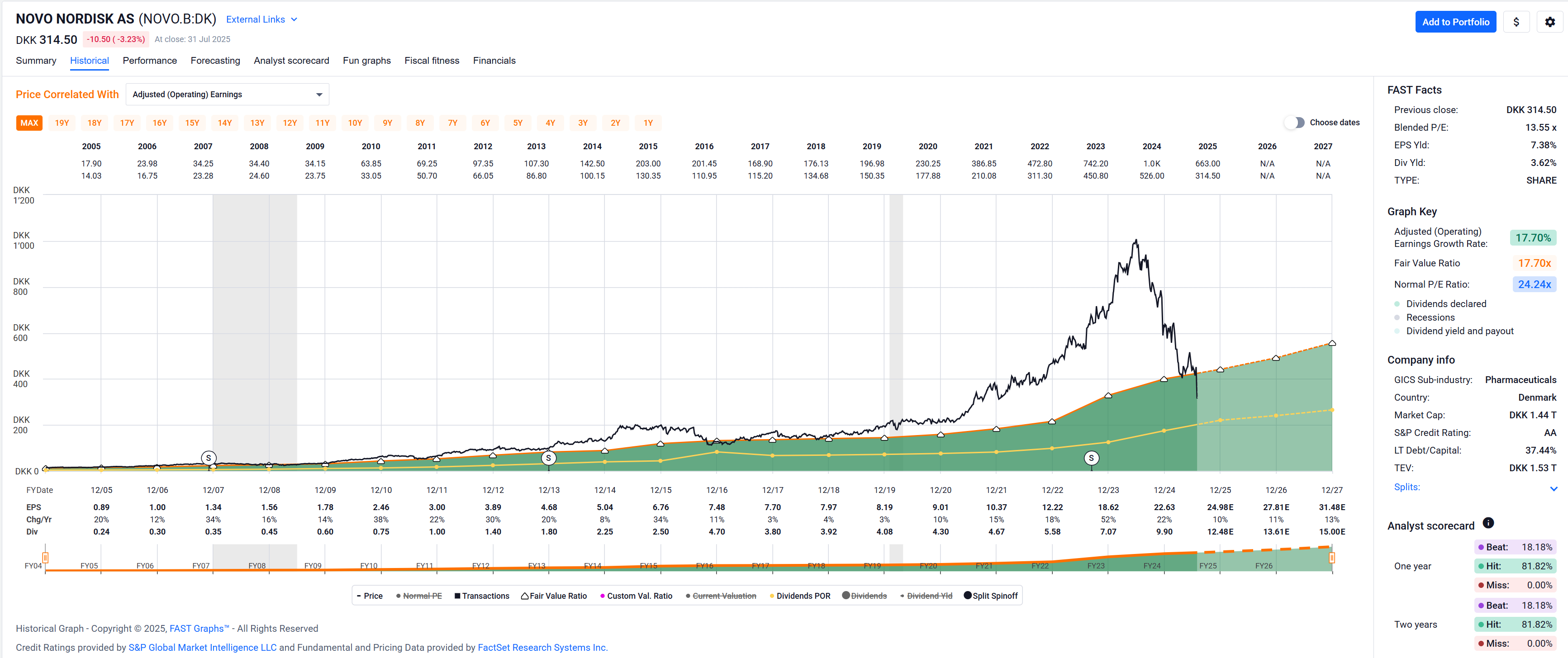

How is Novo Nordisk Fast Graphs looking like? Forward P/E looks interesting

Adjusted Operating Earnings:

(Goofy thinks: Slighty undervalued given their growth over the past 20 years)

Zooming in …

(Goofy thinks: Well, only really slightly undervalued given their growth over the past 7 years plus projected growth in the next couple of years)

Operating Cash Flow:

(Goofy thinks: Well, only really slightly undervalued given their growth over the past 7 years plus projected growth in the next couple of years. Dividend seems to covered well, payout ratio seems ok, perhaps on the higher end than what I would like to see for a dividend growth company)

Free Cash Flow:

(Goofy thinks: Well, a little more iffy … seems they’ll be paying out their entire free cash flow as a dividend this year. At least the projections going forward by the analysts seem to paint a rosier picture).

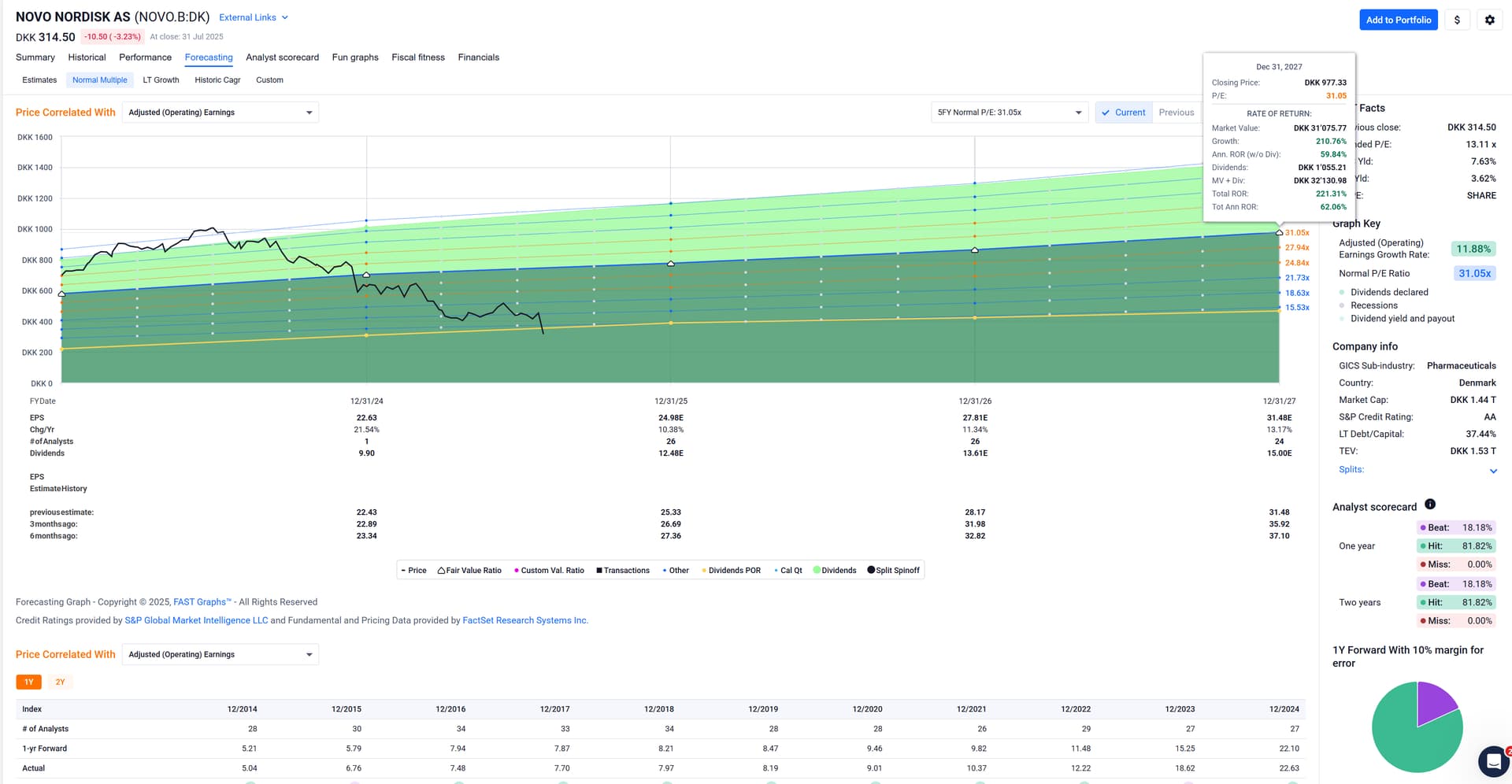

Forcasting:

(Goofy thinks: Hm. Earnings are expected to grow, but analysts’ expectations of earning in this and coming years have consistently be trending down. …)

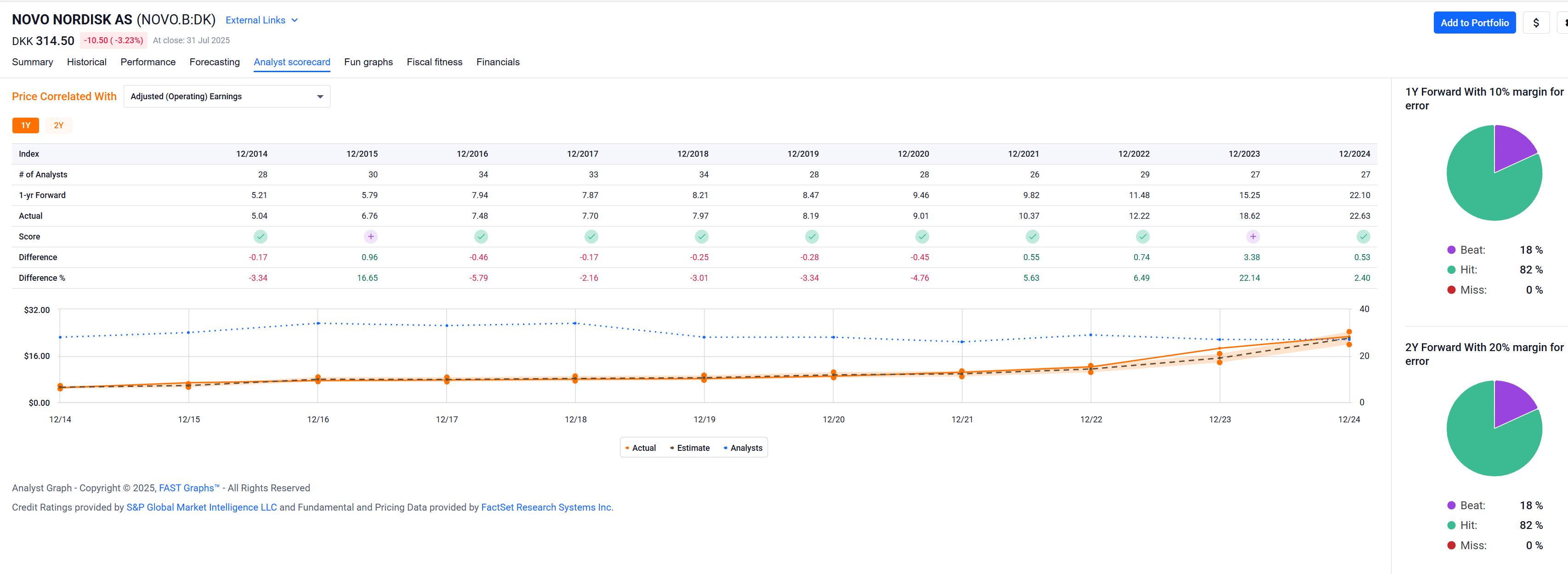

Analyst scorecard: seems fine.

Pretty good return expectation if the company returns to the projected fair 15x multiple:

Flabbergasting return expectations if the company returns to its historic “normal” multiple:

With this 5 minute look Goofy is neither a buyer nor a seller, but thinks there’s equally beautiful brides / brooms out there that might be worth a closer look.

2 Likes

Finance stocks are difficult in that field. Their trading good is money, so investments are not always clearly investments in my sense. I usually try to filter out all business activity that is not like an investment into the business infrastructure.

MET looks still OK to me, even the free cashflow (the investmets) are difficult to identify. I think I did use only “other - net” of 173 millions as of last year.

I hold Metlife for many years, over a decade I think, loaded up a big chunk in 2020 at $27.20. Hope to be able to hold much longer…

How do you guys calculate the investment cash flow of finance stocks?

Anytime, buddy.

So, IIUC, with your idiosyncratic background (and the flying broom just now), you’re basically issuing a “strong buy” (“broom level” buy) on this one?

Did I get this right?

1 Like

Quite honestly … I was going to say “above my pay grade”, but that would really be a euphemism for saying “I don’t know at all”. So, I really don’t know.

Long term, I believe even financials (and their stock price) bend to earnings’ multiples and (operating and free) cash flow, so while short term things might look like voodoo for some financials, longer term, I feel you can evaluate them like other companies.

Do you have (very) differing thoughts on this?

Yes, I do. Normally free cash flow equals operating cash flow minus investment cash flow. Now if money is the trading good in my humble opinion one cannot call it investment; it is normal business. Therefor I do not count the financial “investments” in the investing cash flow. Probably a too simple view, but I could not find anything better.

They buy a new office complex: investment. They buy computers: investment. They buy bonds: no investment, it is their business.

My view is very simplistic but served me OK until now.

1 Like

Of course, who doesn’t want a flying broom?!

What about idiosyncratic background ![]() ?

?

None, of course, that I would know of. But since you’re asking why you might have one, this proves that you actually have one … ![]()

1 Like

This trade didn’t go too well…

2 Likes

I guess with the wheel strategy you wouldn’t consider buying it back before expiry, either?

The stock dropped so quicky that buying back the put was no longer a viable option. Now I’ll have to wait for the stock to recover…

1 Like

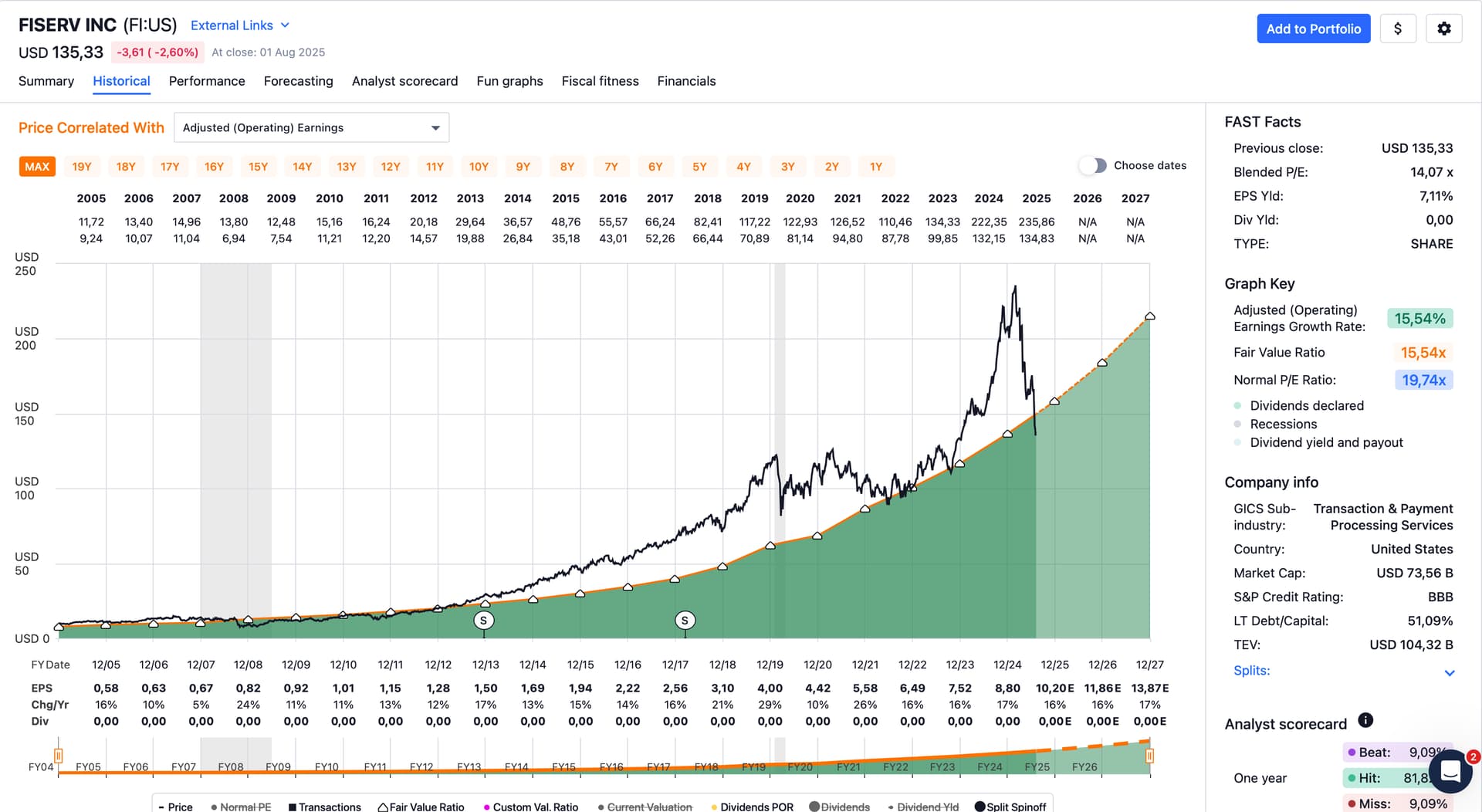

Came across Fiserv (FI) today.

This is a company I’ll likely add to my son’s portfolio next week. No dividend (great if your time horizon is long), nice growth expected, acceptable level of debt, historical earnings look almost perfect.

If you’d like to see Chuck Carnevale discuss the company, check out https://youtu.be/WZRQvOIhh54?si=ijhKHrngB7qe88nH&t=1212

FI:

There is no dividend, but they bought 5.8 billion in own stock, financed partially with new debt. I don’t like that, especially because it is to cover employees options I suppose.

The main difference to dividends: management does not profit from dividends. That is almost the whole operating cash flow and results in a negative FCF to treasury stock payout ratio. Does not seem very sustainable to me… at that point I already stop analyzing.

2 Likes

Shhhhh stock buybacks and dividends are the same thing minus taxes!!!1

1 Like

That’s what makes a market! ![]()

According to Gemini, the stock-based comp was $399 million in 2024 and $239 million in 2025 so far. Their buybacks were $5.5 billion in 2024 and $4.4 billion in 2025 so far. Seems (to me) stock-based comp wasn’t a major part for the additional debt taken on ($1.37 billion in 2024 and $4.4 billion in 2025 so far).

I actually like that they seemingly do more buybacks when their stock price has come down to more reasonable levels … as I likewise dislike that they did large buybacks in 2024 when their stockprice was still way above (my) fair value.

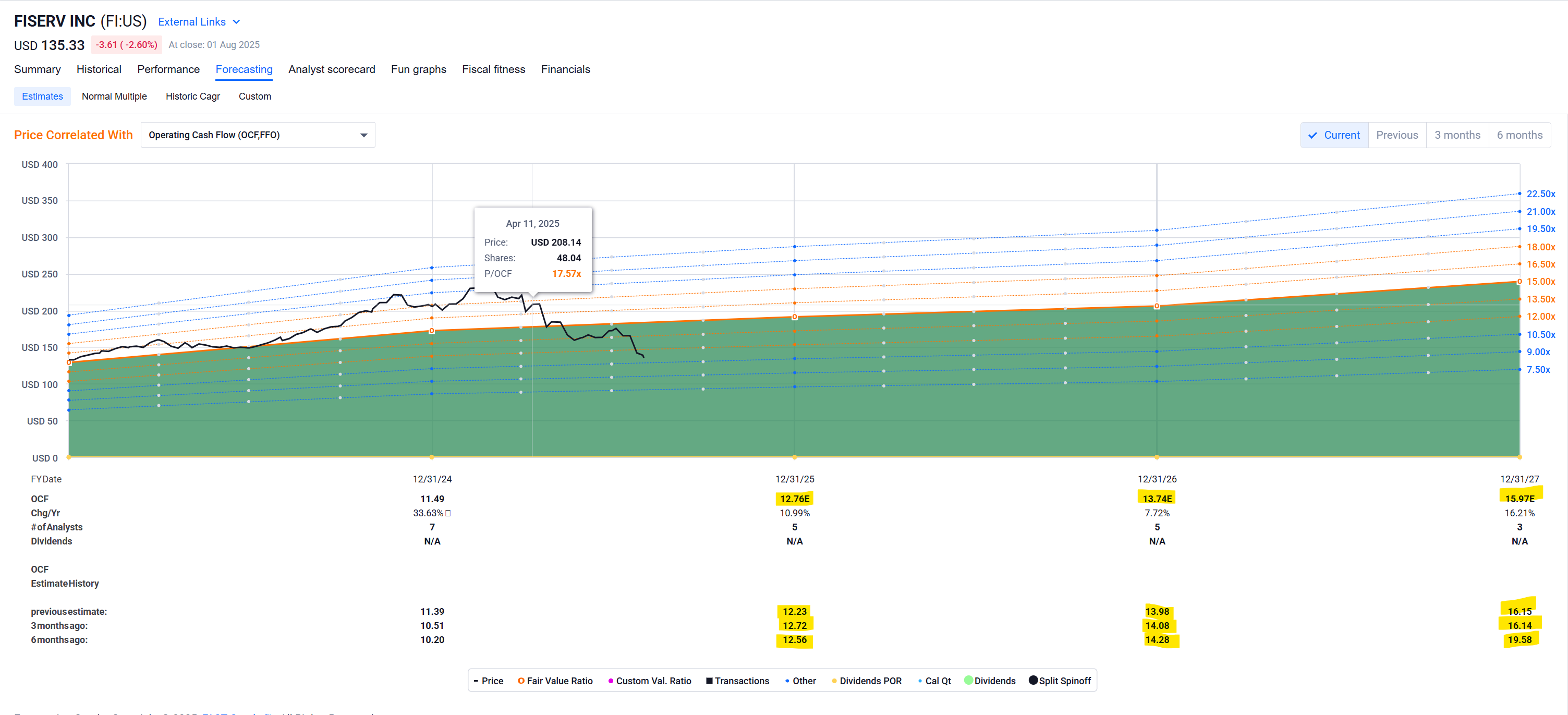

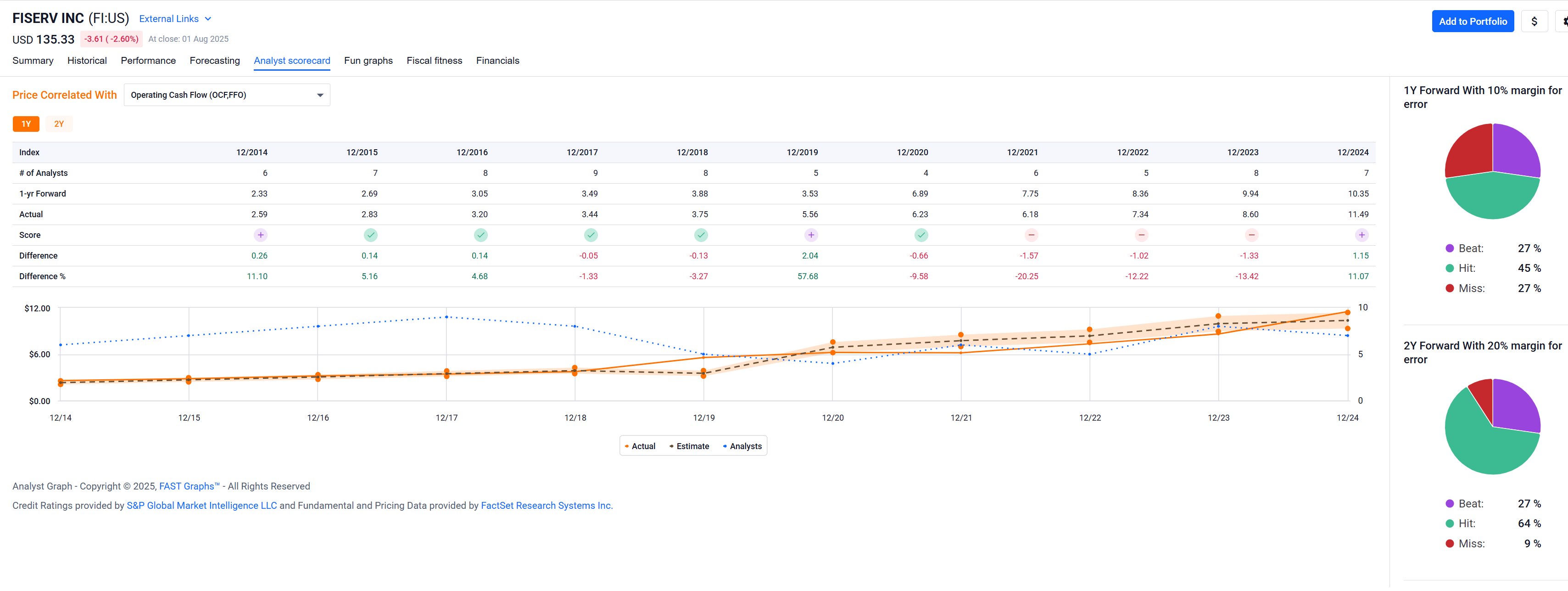

Here’s their OCF over time:

and the analyst[★] estimates going forward

(while analyst[★★] estimates have come down a bit, the growth still looks fine to me)

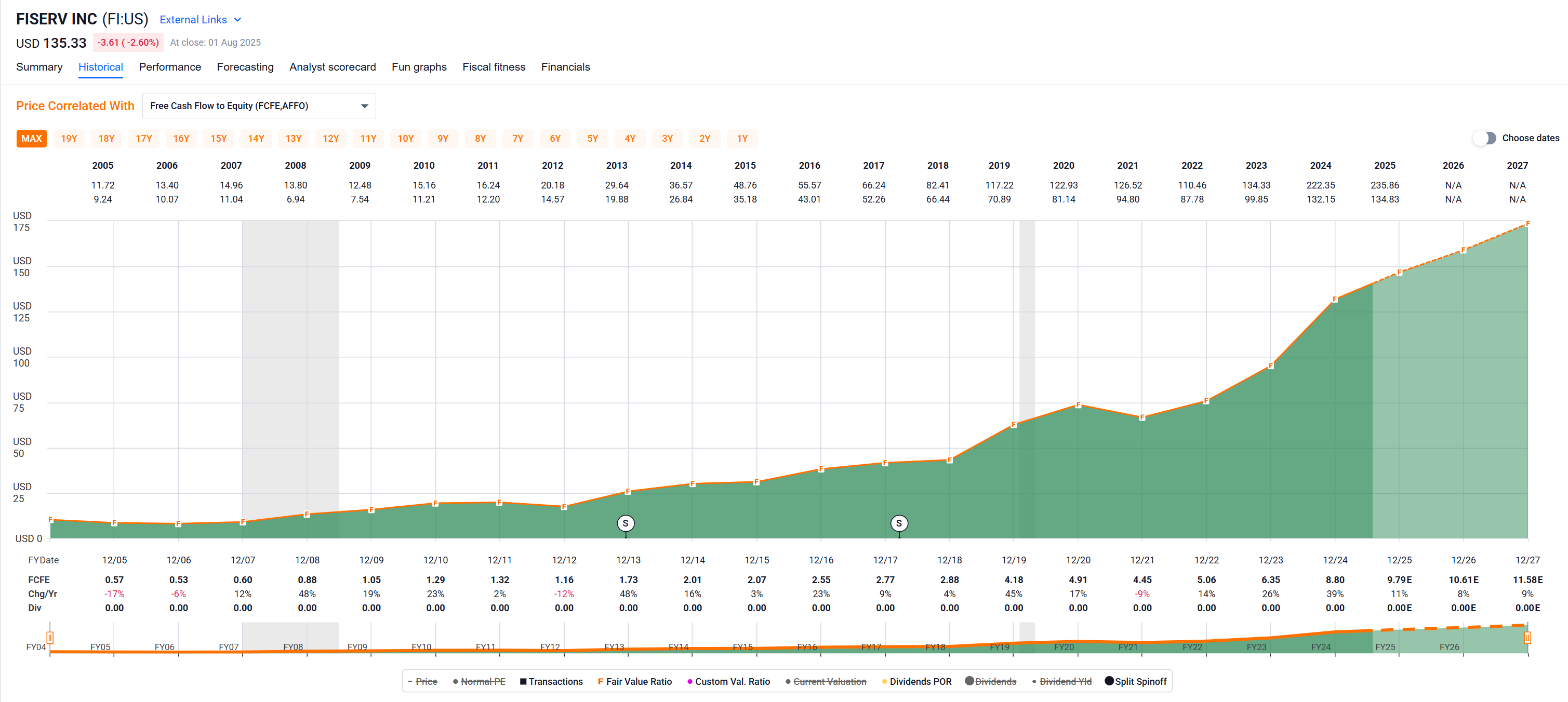

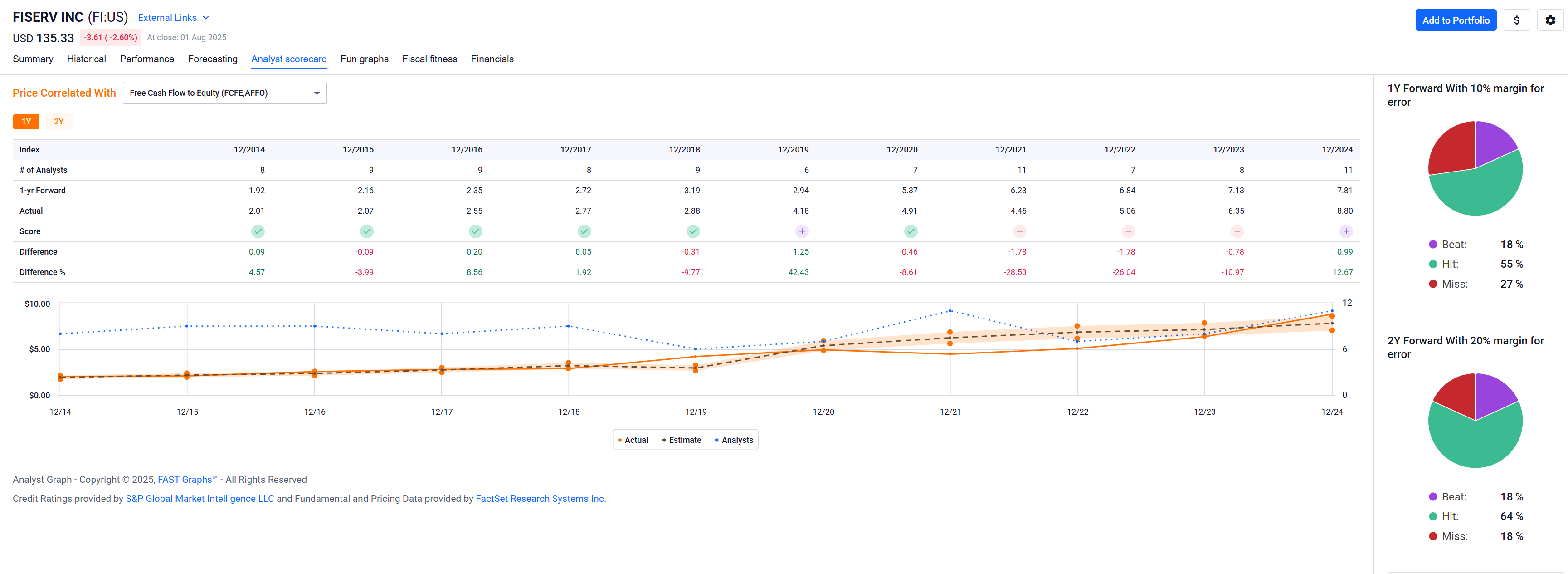

And here’s their FCF:

and analyst[★★★] estimates going forward

I guess I like looking at the balance sheet and cash flow statements (and 10-K and -Q filings) as well, but I like extending the snapshot view by how these things have evolved in the past and how they are expected to do in the future, and I draw a different conclusion. Also, it’s not my money, it OPM. ![]()

Also, I’ve probably never dug as deep for an investment in my son’s portfolio, where I do tranches of about $200 per position, i.e. I’ll probably initiate a single share/$130 position next week and might add to it when further cash arrives in his portfolio (via dividends). ![]()

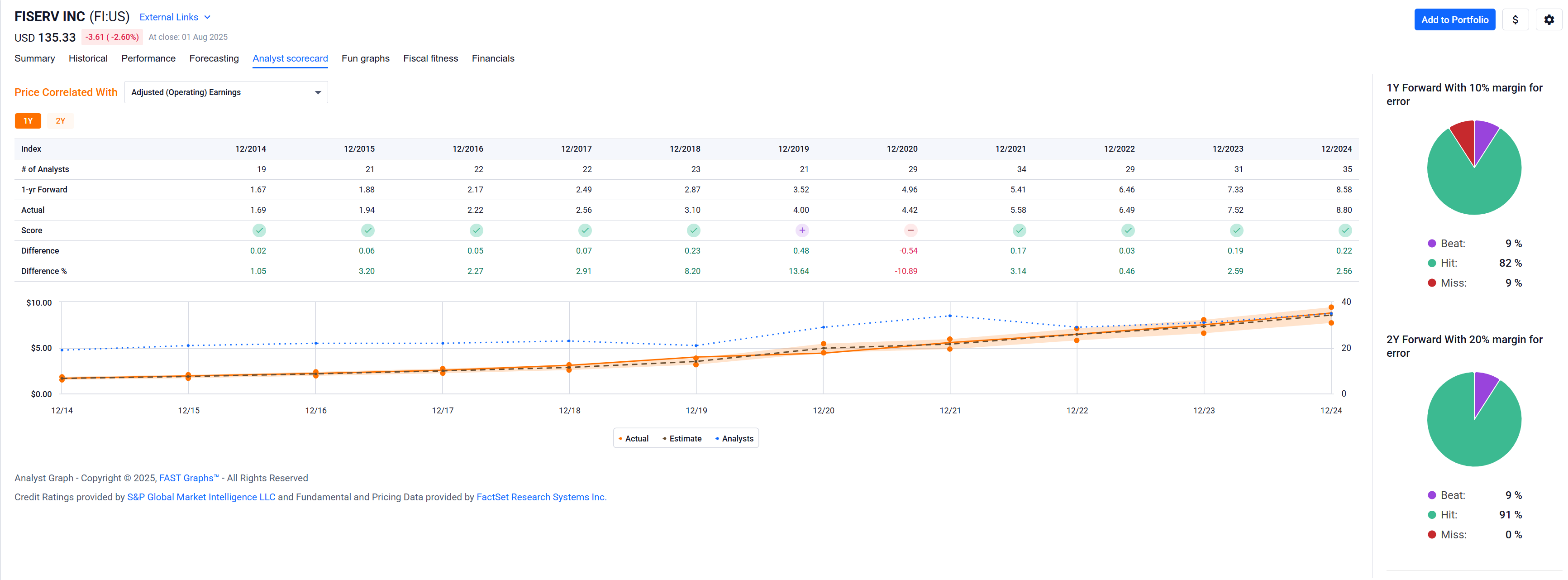

★ Analyst scorecard for earnings looks pretty good:

★★ Analyst scorecard for OCF is still fine:

★★★ Analyst scorecard for FCF is still acceptable:

Not exactly, at least from the viewpoint of management. Dividends are gone, lost forever. Stock buyback however lowers the number of shares in circulation and therefor the remaining shares and especially the options are worth more. That means it goes directly to the management options.

So with dividends we pay tax, with stock buyback we pay the management. If there are no management options stock buyback is better of course.

… and shareholders.

For companies – do these even exist? ![]() – that don’t do stock based comp, we pay only the shareholders with buybacks.

– that don’t do stock based comp, we pay only the shareholders with buybacks.

Add some lingo here about how to incentivize management with stock based comp to have the stock price do well given their vesting schedule.