A few years ago it was in the news for allegedly having Chinese backdoors implanted in the motherboards (this tanked the stock) and then investigated for accounting anomalies (which further tanked the stock) and suspended from the stock exchange for accounting reasons (which stopped institutional buyers from buying). That’s when I bought I just wish I’d held on. It would have made me more than a million. It still pains me to think of that one which got away.

I was in a fortunate position as I had both the technical knowledge to know that the spy story was BS (though even false stories can kill a company) and the accounting issue was not so serious. The great thing was that the suspension from the stock exchange forced many insitutions to sell and stopped them from buying (due to their investment/compliance rules). This is a clear case where the individual investor has an advantage over the institutional investors.

The charts never tell the whole story, could be a top or could be a nice dip.

Then I check some statistics in yahoo finance. Kind of expensive, like all techs, but nice growth. Burns a lot of cash, but debt is still not a big problem.

Then I tend to check the balance sheet. They have almost 1.4 billion in goodwill, meaning they bought other companies and have to downwrite the difference in the foreseeable future, 1.4 billion less earnings (that are already spent). Now I would trace back the company or companies they bought. I would check if the growth is bought or “natural” and if it may continue or not.

And one last thing: the motley fool is pushing it, which normally I don’t like.

Thank you. Are these charts from your system? I don’t like the hype around SoFi either. I’m a bit puzzled about pricings in high priced markets, years ago I bought some (way more stable!) stuff which was high priced, and now are on the moon… But I am a beginner, but dividend investing in my current life stage is not as attractive as buying my ETF combo and on the side I do stock picking.

What I did so far (basics):

website, services, get to know to the company

last earning call webcast+transcript

competitors, market overview

Trustpilot, Glassdoor, complaints, Reddit (both company users and stock people), Youtube (filtering out hype influencers)

Management LinkedIn profiles

Torturing chatgpt with tons of questions

SA analyst concerns

Someone today recommended me to have a deep look to P/B ratios on the market, so homework for today, but anything else I might have missed? My general strategy is to look deep into growth-value / high momentum individual companies which I would buy and hold for 5 or more years. But since this is a bank my general EVA/Economic Value approach does not work here.

I just got a message that the chart images in my last post have been downloaded, so they probably are no longer self adjusting. Makes sense, saves bandwidth…

A few words to my methods of analyzing (which I hardly ever use, as my trading is completely mechanic):

The stock market is probably the biggest casino in the world. Where there is that much money there is a lot of cheating. Everybody cheats, really everybody. “A company report is a lie that contains exactly as much truth to be still legal.”, I think that were words of Peter Lynch the legendary fund manager.

That said, there are numbers that are easily forged and others that are not. Earnings are really easy to forge. I used to say that the planned retirement of a CFO has more weight on the earnings than the companies business. Rules allow too much interpretation, like depreciation and some other. Cash flow and sales are harder to change, so I tend to use those.

A easy way to cheat are takeovers. We have a lot of examples from the past, like wirecard. If a small company has more goodwill in the balance sheet than equity that means that all the stockholders money went to the last owner of the bought company. That may have been a very good opportunity or simply a (half-legal) way to steal the money of the stockholders. Every such transaction has to be controlled. Those birds got away too long with this kind of cheating.

In this decade a new scheme has come up: SPAC (Special Purpose Acquisition Companies). Those are companies with absolutely no business that are listed at a stock market. They merge with non-listed companies to avoid all the controls a real IPO includes. Most of the capital invested in SPAC goes right back to the ex owners and the SPAC handling banks via options. After 2-3 years 98% of those companies lose money, some of them a lot. I use a SPAC filter and do not touch with gloves any company that was listed this way.

Tradingview has nice charts too, you can select to include dividends and compare.

The book value and therefore the P/B ratio is hardly ever correct. Too much interpretation. And it is not even on sector level but on individual company level. A low P/B ratio may mean the company is undervalued or the assets of the company are priced too high in the balance sheet.

An example: McDonalds still has a negative book value. The real estate is valued way too low in the balance sheet, I suppose for tax purposes.

The Swiss biotech company Idorsia is facing a deepening financial crisis and has asked creditors for another extension on repaying a convertible bond due on January 17, 2025. Even if creditors agree, the company’s liquidity will only last until the end of March. Idorsia has been reducing costs and cutting staff, with employee numbers expected to drop from 1,300 two years ago to 450 by the second quarter of 2025.

To improve cash flow, Idorsia has sold inventory of its sleep medication Quviq to Japan’s Nxera Pharma and secured $30 million in financing from an Asian investor, linked to future revenues from its drug Vamorolone for Duchenne muscular dystrophy.

Founded in 2017 by Martine and Jean-Paul Clozel after selling Actelion to Johnson & Johnson, Idorsia once had ambitious goals. However, competition from cheaper generic sleep aids has limited Quviq’s sales to CHF 55 million, far short of the billion-franc target. Another potential blockbuster, Aprocitentan for hypertension, is approved but not yet marketed, and the company has not secured a licensing partner despite ongoing negotiations.

Idorsia’s stock has plummeted to under CHF 0.80, and its market value is now around CHF 140 million. Analysts are increasingly critical, describing the company as a “bubble of promises” amid deteriorating investor sentiment in the biotech sector. The broader market for biotech mergers and acquisitions also weakened significantly in 2024.

At least Bank in Zürich survived. Kind of, at least. It first merged with with SKA (Schweizerische Kreditanstalt) in 1905, which was – by then as Credit Suisse – in turn acquired by UBS as recently as a couple of years ago.

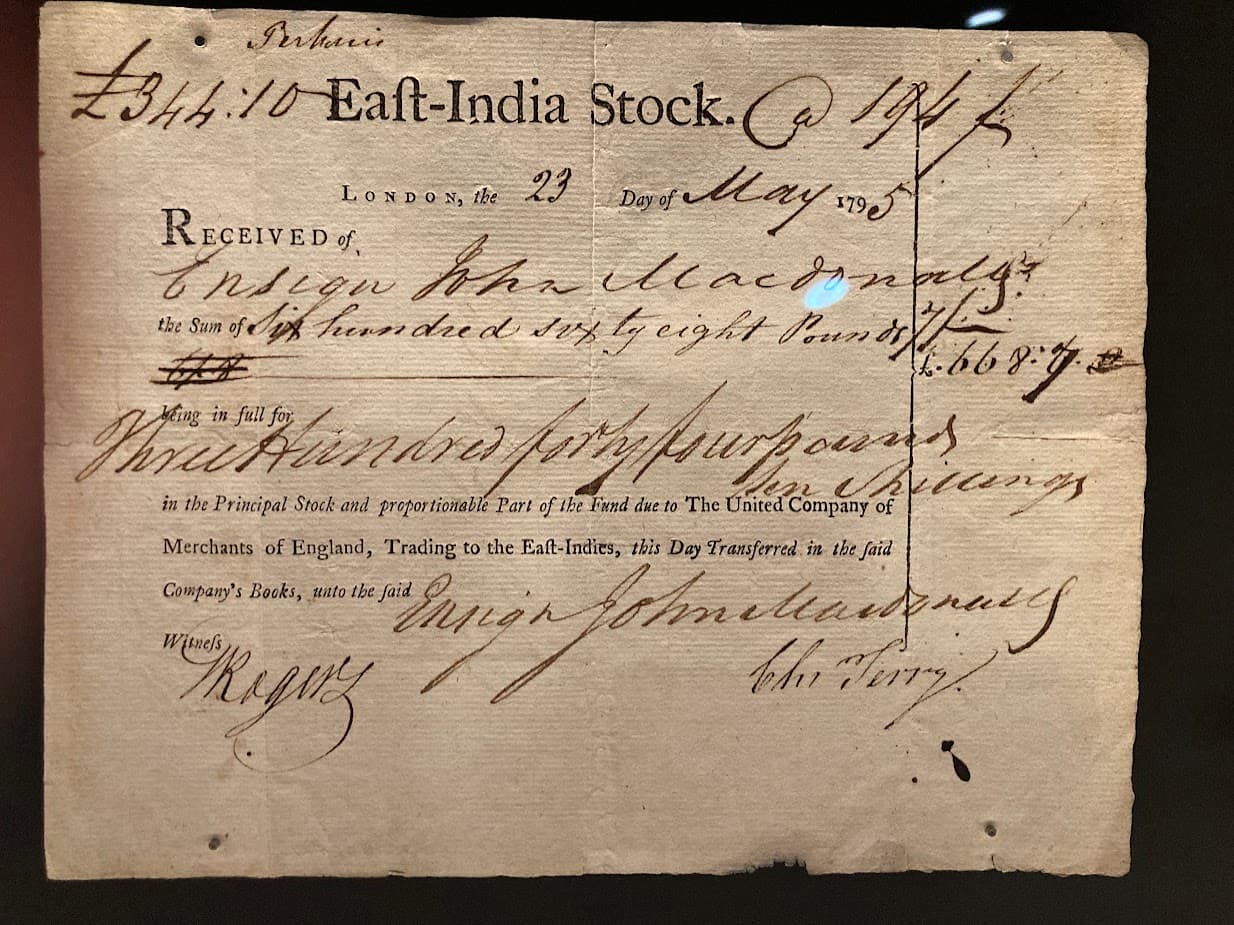

All pics are from this afternoon's visit to the Swiss Finance Musuem (https://www.finanzmuseum.ch/en/home.html), conveniently located in the basement of SIX Swiss Exchange in Zurich.

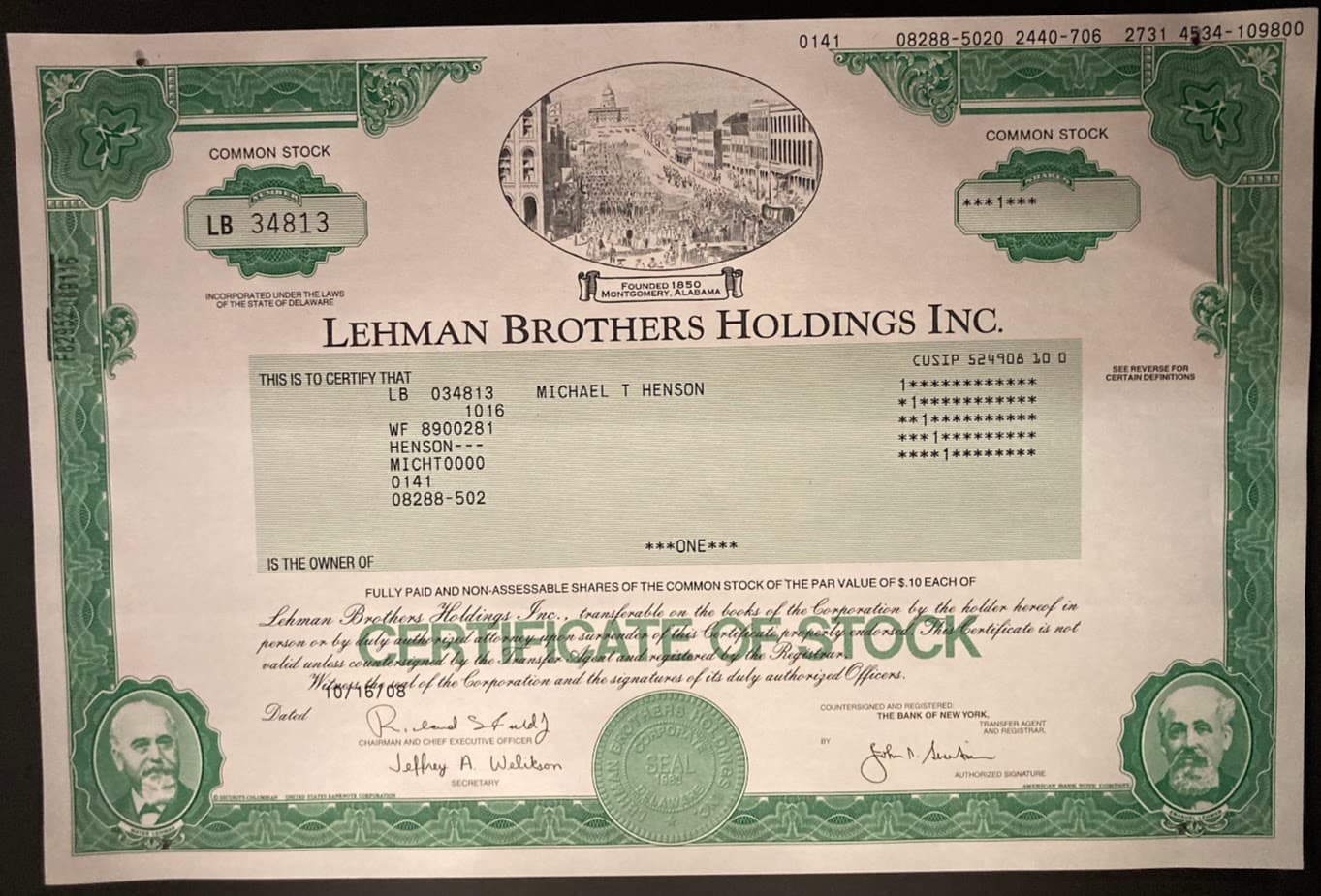

Over Christmas my mother told me my grandpa had some physical share certificates, somewhere. Doesn’t even know what they are, mentioned “some French railway”. I now want to see them, chances are they’re worth nothing more than the sentimental value.

Fun fact, I wanted to get one of my brothers a framed BRK.B physical share for his wedding last year, turns out it’s not THAT easy to get physical shares (I found this but was not convinced it’s not an expensive gimmick). In the end I just put some money in the IBAN he’d put in the invitation, so cold and soulless!

When I bought a Zurich Zoo share, I received a piece of paper that looked like a certificate. But I threw it away, I was only interested in the annual dividend (a free zoo ticket per year).

I keep wanting to buy one of these Swissair bonds (also to frame and hang at the wall of my “trading desk”), but found these worthless pieces of paper too expensive for CHF 5 when I last checked maybe about a year ago.

“In 2025, the Zurich Zoo in a joint venture with ETHZ leveraged its animal zoo population data to train the most successful stock picking AI model yet and the Zoo’s shares surged around 10’000 fold.

A mere CHF 200 share from 2024 is now worth CHF 2’000’000 and there’s supposedly shareholders going through their trash bins to resurrect such orginal CHF 200 shares.

As a side effect, the single entry ticket purchases also ballooned for the Zoo as potential vistors were no longer interested in buying a CHF 2 million share to get a free single once-per-year Zoo entry and instead opted to buy the normal Zoo ticket.”

Interesting. Do you have a method to decide when to sell/buy what?

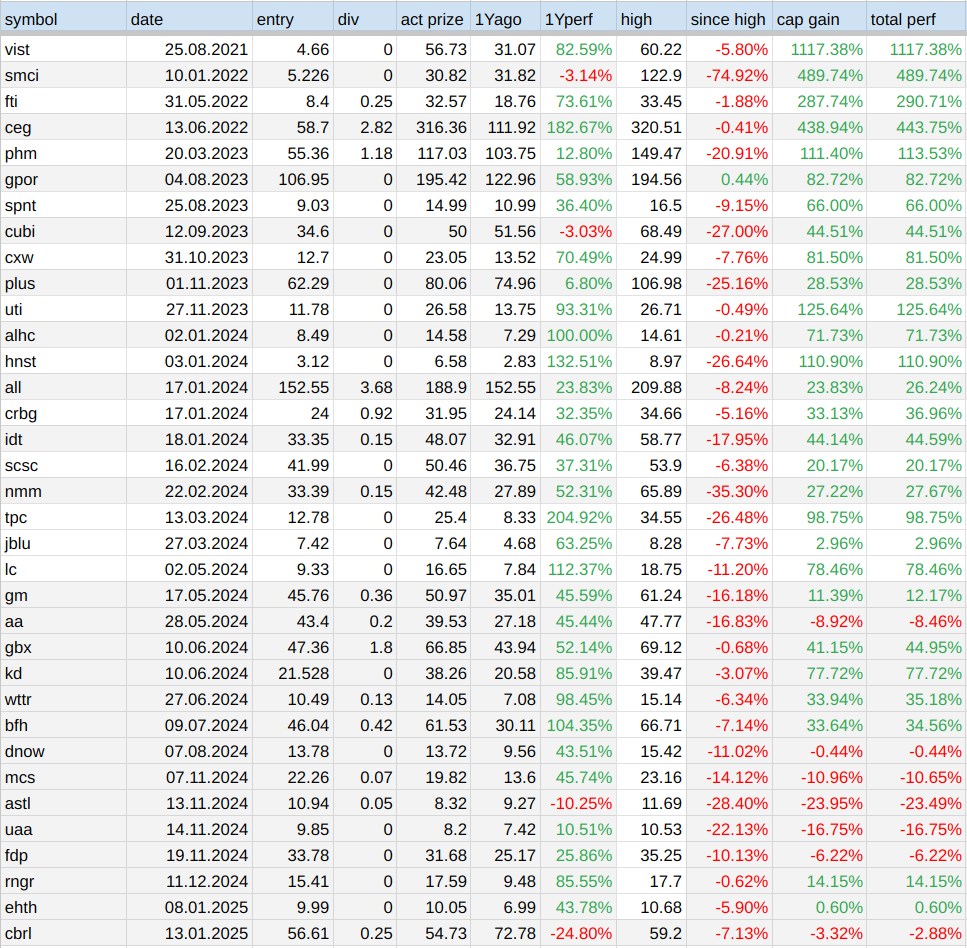

My energy stocks in the growth/momentum strategy at the moment: VIST, GPOR, FTI, WTTR and RNGR. Always hold a few, some since many years. Best performer is Vista Oil & Gas, +1117% since buy at 08/25/2021. Mexico and Argentina, thanks Mr. Milei.

This is a “push” strategy, meaning I only sell when I want to buy something new. All mechanical.

Here is a table of all my holdings in this strategy with some statistics:

I usually sell just before the stock goes on massive rally. And buy just before a big crash.

But seriously, I look at what I want to buy or sell and then sell or buy something else to balance it.

I love that one from Will Rogers:

Personally I hold as long as possible… but not longer. As a rule of thumb, the longer I can hold the more money I make. One has to pick up a lot of stones to find a diamond, but you can only lose 100% (which I never did) and gain many 100% (which I did quiet a few times).

My “luck” changed a lot when I decided to switch to mechanical investment. Even knowing the fact that my caveman-brain plays a lot of tricks on me I still fall for those tricks. Only strong rules did help.

Mit dem Lesen und der Teilnahme an diesem Forum bestätigst du, dass du die Forum-Richtlinien gelesen hast und damit einverstanden bist sowie den Haftungsausschluss auf http://www.mustachianpost.com/de/ akzeptierst.